Loans to Nonbanks Threaten Banking Crisis

Last week, the Federal Deposit Insurance Corp published the latest data on US banks for 2025. At first glance, the figures appear reassuring and solid. However, beneath the headline lies a growing peril that investors should carefully consider. According to the FDIC, domestic deposits rose for the sixth straight quarter in Q4 2025 by $318.3 billion, or 1.8%. Loan balances increased 2% in Q4, with nearly 6% growth year-over-year. Foreign deposits expanded by 11%, while subordinated debt and FHLB advances dropped roughly 14% as banks reduced excess capital and funding sources.

U.S. bank lending in 2025 showed strong momentum, with total loans and leases reaching $13.4 trillion by the end of the year—a sequential rise in Q4 and an annual growth rate of 5.9%, driven mostly by larger banks. Personal loans climbed to $2.2 trillion, and credit card debt expanded 5.5% year-over-year, though card utilization remains below 20% of available credit. Still, this seemingly stable outlook conceals an escalating vulnerability threatening banks and broader financial markets. What appears as a steady financial system is, in reality, masking a swiftly expanding risk that could emerge as a major stress point.

The segment growing the fastest among bank assets is lending to non-depository financial institutions (NDFIs), a part of the financial ecosystem that regulators find challenging to oversee, rising 7% quarter-over-quarter and surging 35% year-over-year to $1.4 trillion by the close of 2025. Signs of mounting credit distress among nonbank entities suggest banks will eventually pull back from providing loans to NDFIs. The critical factor is timing: banks’ tightening of credit comes too late for many private firms heavily dependent on this funding, which may already be headed toward failure. Such collapses will not remain contained within the shadow banking realm.

Instead, these problems will directly impact bank balance sheets.

The recent default involving UK mortgage lender Market Financial Solutions risks a collateral deficit of £930 million backing loans to Apollo, TPG, and other Wall Street-focused private credit sponsors. These players are deeply involved in lending to private credit and equity, as well as speculative ventures aligned with the ongoing “AI investment boom.”

“The collapse of MFS, which attracted backing from firms including Barclays Plc, Apollo Global Management Inc.’s Atlas SP Partners unit, Jefferies Financial Group and TPG, is the latest crisis to hit both banks and direct lenders, and puts a spotlight on asset-based financing,” Bloomberg reports. “Accusations of double pledging also emerged in the collapses last year of US auto parts supplier First Brands Group and sub-prime auto lender Tricolor Holdings.”

Similar allegations of double pledging collateral have arisen in failures like First Brands Group and Tricolor Holdings, highlighting the system’s fragility.

The fact that Apollo’s Atlas SP unit was blindsided by apparent collateral fraud at MFS is striking given their extensive history in this sector. As one of the major providers of secured financing to US nonbank mortgage companies, Atlas SP—once owned by Credit Suisse and advisor on many NDFI financing deals—now faces defaults on two “secured” warehouse facilities it backed. If the arrangers of these loans are surprised by the collateral issues, it raises serious concerns about how widespread the underlying risks truly are.

The 2023 failure of American Car Centers, another Atlas SP client, foreshadowed a wave of corporate bankruptcies that now threaten contagion within the US banking sector. Corporate filings in 2025 surged to a 15-year peak, exceeding 700 by November, a 14% jump from 2024. Many of those bankruptcies involved private equity-backed businesses.

Why is the rapid expansion of bank lending to NDFIs so alarming? Federal Reserve Chair Jerome Powell has acknowledged that while non-depository institutions serve an important role, their growth beyond traditional regulatory oversight introduces financial stability risks. This isn’t about mortgage firms with fully secured loans, but rather speculative credit and private equity ventures facing cash shortages.

The rise of private equity and credit is particularly troublesome for banks. Numerous lenders are quietly delaying recognition of early defaults via loan forbearance. When struggling private equity firms cannot meet obligations, they often attempt to buy time by repaying in “kind”—issuing additional equity, effectively creating more shares of already devalued capital. The term “principal on original principal” or “POOP” (h/t Victor Hong) describes this tactic, which private equity sponsors use to hide financial distress. Put simply: investors receive payment in more of the same flawed capital structure.

In 2024, Jerome Powell warned about the unchecked expansion of nonbank financial firms and the migration of financial activities outside the regulated banking system. He stressed the importance of regulators being “smart” about spotting emerging risks, emphasizing that lending by nonbanks could undermine economic stability. Yet, federal regulators have taken scant action to counter the surge in loans to NDFIs. Historically, when a bank asset category grows noticeably faster than the overall economy, it signals the buildup of systemic risk.

Seeing a bank asset class increase well beyond the pace of the general economy is a major warning signal. Even more concerning than the rapid growth in loans to NDFIs is the enormous volume of undrawn credit commitments to these lightly capitalized private equity and credit firms.

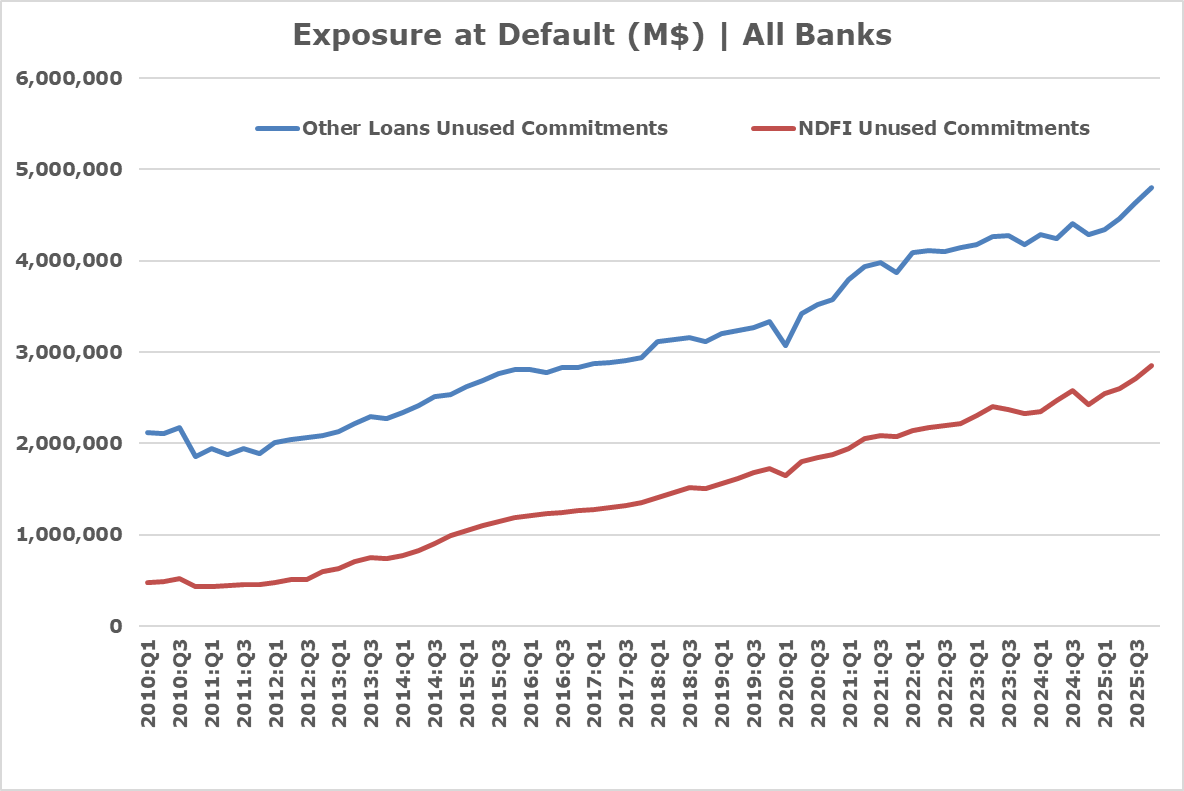

Although the FDIC does not fully itemize loan categories for NDFIs, inferred data suggest banks hold roughly $2.8 trillion in unused loan commitments to NDFIs, representing an exposure at default about 200% of current advances per Basel III definitions. This means a nonbank entity could draw on these credit lines and default immediately, inflicting substantial losses on the lending bank. For every dollar of the $1.4 trillion in outstanding loans to NDFIs today, there are two additional dollars in undrawn commitments—a total exposure near $2.8 trillion, as illustrated below.

To break it down:

- Banks currently have $1.4 trillion in loans outstanding to NDFIs

- They hold another $2.8 trillion in undrawn commitments

In other words, for every dollar lent, an additional two dollars may soon be drawn.

If a nonbank borrower pulls those funds and defaults immediately, losses land squarely on banks.

Total potential exposure could reach approximately $4.2 trillion.

Should stress spread across private credit markets, this figure turns critically significant, and rapidly.

Source: FDIC

The enormous volume of bank lending to NDFIs is a looming threat largely overlooked by federal regulators but increasingly noted by credit analysts. A clear indicator of rising credit difficulties among nonbanks is found in business development companies (BDCs), whose stock prices have dropped 18% over the past year, in stark contrast to a similar gain in the S&P 500. This divergence is no coincidence: BDC investors are signaling that risk within private credit markets is intensifying rapidly.

“UBS strategists say private credit could see default rates surge as high as 15% if artificial intelligence triggers an “aggressive” disruption among corporate borrowers,” the Swiss bank reports. “Direct lenders that financed software companies are exposed to AI’s impact, with some estimates suggesting 40% of all sponsor-backed loans are tied up in the software industry.” A 15% default rate is twice the highest bank loan delinquency recorded in 2008.

To put that into context, a 15% default level would nearly double the peak bank loan delinquency rates from the 2008 financial crisis.

Should even part of that scenario come to pass, the private credit sector and the banks funding it would face significant immediate repercussions.

The year 2025 was remarkable in many respects, including low credit losses and soaring asset prices. Quantitative easing has historically suppressed default costs by propping up asset values—until those valuations decline. Yet Wall Street continues to portray the rising delinquencies among private firms as a marginal issue.

“A review of the 3,649 middle market (MM) corporate credit assessments completed in 2025 shows mixed signals,” explains Kroll Bond Rating Agency. “Slowing growth is negatively impacting some companies’ credit quality, but overall, our portfolio remains stable. The growing divergence in performance is driven by challenged subsectors that we believe will contribute to the rising, yet contained, default rate in 2026.” In short, cracks are emerging, yet the market hopes the fallout remains limited.

In the 1920s, many believed asset values had reached a “permanently high plateau.” That faith did not hold up well, despite warnings about an impending crash. Sectors such as private equity, credit, and AI suggest rising credit costs ahead. For lenders, the immediate effect likely means increasing credit expenses, which compress earnings and depress stock prices. The sharp drops in bank shares during January and February illustrate this trend.

We anticipate bank equities will fall short of their strong 2025 gains and face several headwinds:

- Growth in credit expenses

- Heightened market volatility

- Increased operating costs

Lower funding costs will provide some margin support for banks.

Yet, the outsized exposure to nonbank financial institutions could become among the most influential financial stories of 2026.

If distress spreads through private credit markets, investors may soon realize that the shadow banking system is far less insulated from traditional banks than commonly assumed.

Editor’s Note: Investors seeking detailed insight into bank balance sheets and emerging credit challenges can follow Christopher Whalen’s ongoing analysis and commentary.

- Watch Chris on The Wrap with Julia La Roche, where he regularly covers banking, credit markets, and financial regulation. Also available on Apple Podcasts.

- Explore further private market risk insights here.

- Monitor performance via Whalen Global Advisors’ Top Bank Index, a proprietary benchmark tracking leading U.S. financial institutions.

Access to the index and comprehensive bank research is offered through Institutional Risk Analyst.

For investors navigating the shifting landscape of banking risks, independent research has never been more essential.