The Largest Oil Disruption, Ever…

On an ordinary day, global oil production and consumption sit at 103 million barrels.

Currently, due to Iran’s closure of the Strait of Hormuz and attacks on oil facilities, approximately 10 million barrels are offline and inaccessible.

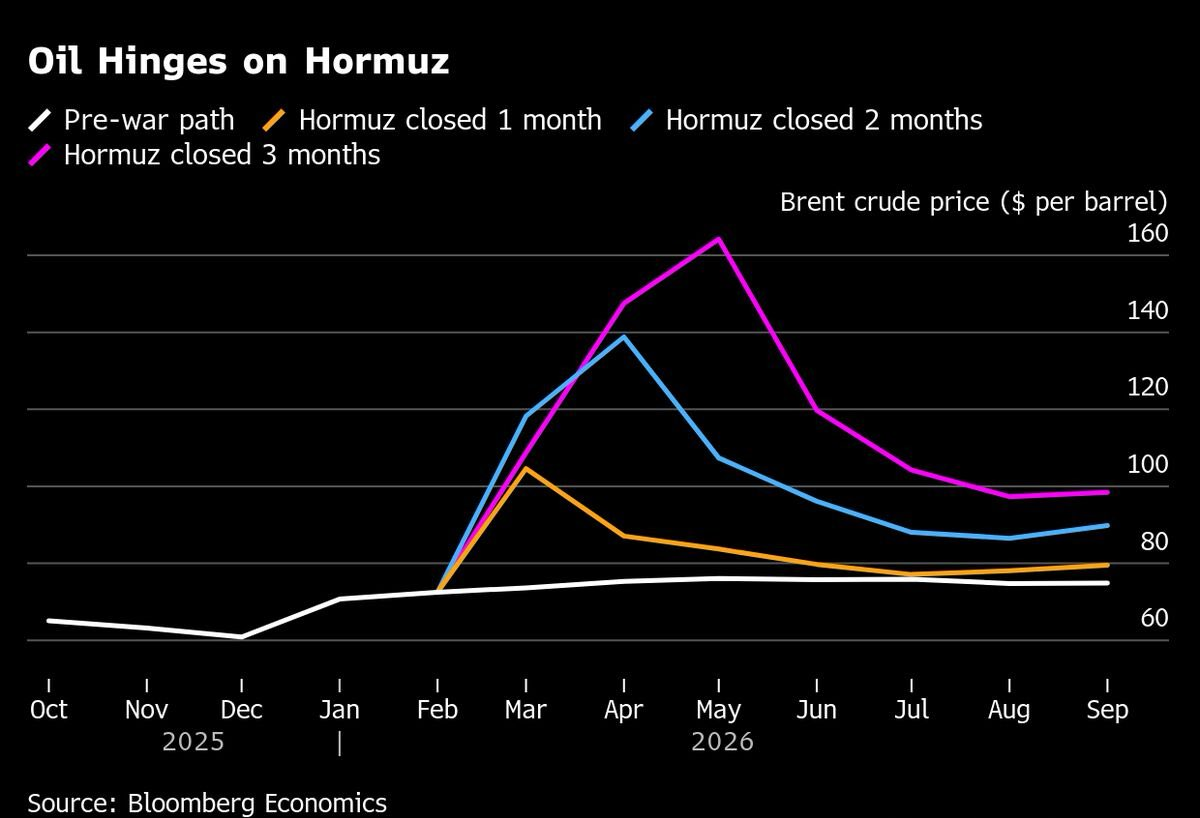

Bloomberg Economics has modeled situations where the Strait of Hormuz remains closed for one, two, or three months. Their experts predict oil prices could soar to $165 if the shutdown lasts three months—$100 more than pre-war levels.

We are only 13 days into the conflict, yet Brent crude has surpassed $100 per barrel. I believe Bloomberg’s forecasts may be somewhat optimistic.

In the Paradigm Press app today, Jim Rickards shared insights regarding Western allies releasing over 400 million barrels from their strategic reserves:

[Note from Adam: For real-time commentary from Jim and other Paradigm editors, just download our free app and visit the “daily feed” section.

The app works on both Apple and Android devices.

Get the app here.]

Weird Science (Economics)

Some might wonder why a “mere” 10% reduction in oil supply (10 million barrels) leads to a price surge exceeding 50%.

Oil demand is “inelastic,” meaning it remains strong regardless of price changes. People still commute, ships transport goods, power plants operate, and airplanes fly.

It takes substantial price hikes to prompt reductions in these activities.

This means even a slight supply drop can drastically affect prices. For instance, in 1973, a 3 million barrel-per-day decrease caused oil prices to quadruple from $3 to $12.

No Spare Capacity

Currently, more than just a 10% production decrease is disrupted due to turmoil in the Gulf. The region contained most of the world’s spare oil capacity, primarily in Saudi Arabia and the UAE—nations now cut off from their export routes.

Source: BBC

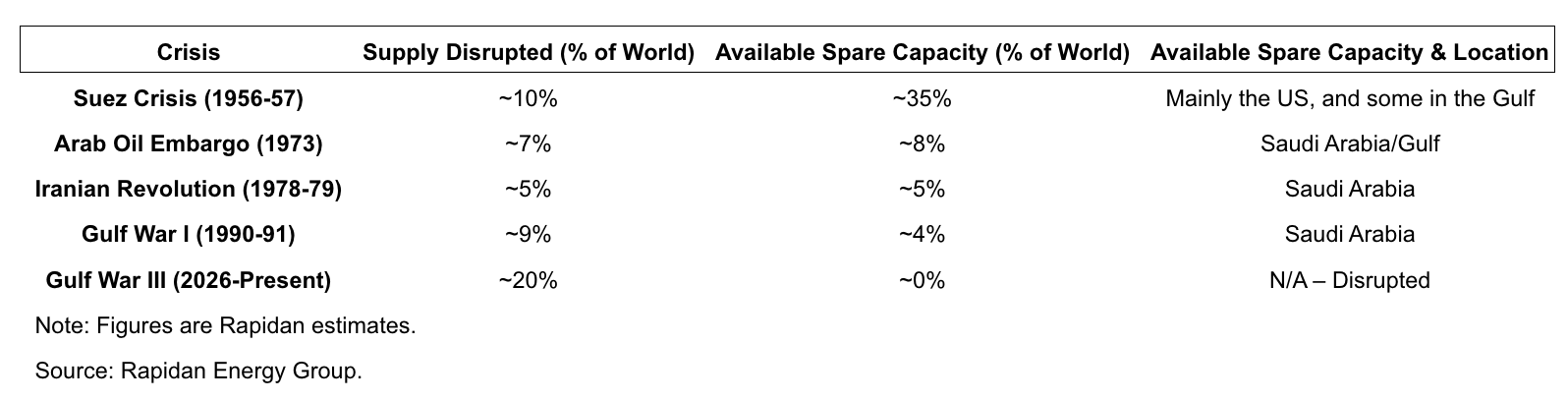

Dan Amoss, Senior Analyst at Strategic Intelligence, shared a table by Rapidan Energy Group illustrating supply disruptions during various conflicts. Their data estimates that today’s crisis has halted about 20% of supply altogether (including spare capacity previously available before this war).

According to Rapidan’s research, this event marks the largest oil supply disruption of modern times. An excerpt reads:

Rapidan Energy Group’s proprietary historical disruption dataset – covering every major supply event since 1950 – confirms that Gulf War III has exceeded any prior disruption by more than 2x.

During the Suez Crisis – the last time a disruption approached this scale – spare capacity stood at ~35% of global supply and was located largely in the US, where it was available to global markets. That cushion no longer exists.

Currently, there is virtually no spare capacity. Though strategic reserve releases help temporarily, their quantity is insufficient and expected to last only around 130 days.

Russia to the Rescue?

At the beginning of this conflict, Jim Rickards informed readers that, “The big winner will be Russia, which can make up for Persian Gulf shortfalls to some extent with its own exports.”

Russian oil, much of it previously restricted, is now easing supply pressures in the near term. President Trump has temporarily lifted import restrictions on Russian oil for India, allowing many Russian “shadow fleet” tankers to more easily deliver their cargo.

The financial press is beginning to highlight this trend. Today’s Financial Times observes: “Russia is earning as much as $150mn a day in extra budget revenues from its oil sales, making it the biggest winner from the conflict in the Middle East.”

Still, Russia’s capacity to offset the shortage is limited.

Typically, Russia could boost oil output quickly. However, Ukraine frequently targets their oil tanks and refineries with drone attacks, leading to damage like this:

Russian oil facility in Bryansk. Source: VOA

As a result, Russia’s ability to increase production dramatically is constrained due to ongoing conflict.

Knock-On Effects

I don’t want to sound overly pessimistic, but history shows that sharp spikes in oil prices often bring unpleasant consequences.

Our colleague Matt Badiali provided this graphic:

Rapid increases in oil prices frequently correlate with slowdowns or collapses in housing markets.

Off-Ramps?

Initially, I anticipated this conflict would last less than a month. However, both parties now seem entrenched.

Trump has delivered mixed messages. At a rally in Kentucky, he declared, “We’ve won… in the first hour it was over.”

Yet he also said, “We don’t want to leave early, do we? We got to finish the job.”

Conversely, Iran rejects Trump’s viewpoint. Its leadership vows to persist until the U.S. admits fault and pays reparations (which is unlikely).

Although Iran’s navy and capital have suffered heavy losses, they continue missile and drone attacks. In response, Israel, Bahrain, and the UAE have introduced strict censorship banning citizens from sharing war footage.

The only foreseeable exit I see is if President Trump declares victory without enforcing regime change—a stance likely acceptable to most Americans.

Hopefully, a resolution is reached soon. If the Strait of Hormuz remains blocked and oil infrastructure keeps burning, prices could skyrocket to $200 per barrel.

Such an increase would almost certainly trigger a global recession, stock market collapse, and a humanitarian disaster across many regions.

Let’s hope that outcome can be averted.