The Truth About Oil Markets

Happy St. Patrick’s Day, a day when everyone embraces a bit of Irish spirit.

Meanwhile, at the local gas station, the price for a gallon of regular gasoline has soared to $3.99, marking an increase of roughly 30% over the last three weeks since the good old days of… let me check… February. (Keep in mind, these are prices from Western Pennsylvania, where state fuel taxes also apply.)

Irish or not, higher fuel costs affect us all, prompting questions from readers like:

- What factors contribute to the price of gas at the pump?

- How long might these higher prices persist?

- What consequences will rising costs have on other parts of the economy?

- What strategies should investors consider?

There’s a lot to unpack, so let’s get started…

Oil’s Global Reach and Price Tag

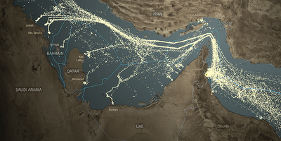

The recent surge in pump prices stems from the conflict with Iran, which resulted in the closure of the Strait of Hormuz, located at the southeastern end of the Persian (sometimes called the “Arabian”) Gulf.

Pre-war, typical tanker routes through Hormuz. Courtesy Reuters News.

Shutting down Hormuz halted the movement of thousands (indeed, a huge number) of tankers transporting crude oil, refined products, and various other commodities worldwide. With these ships idled, less oil and fuel products circulate internationally, pushing prices upward because oil functions as a globally traded asset.

Accounting for differences in chemical composition and physical attributes, oil prices depend on international supply and demand dynamics. However, it’s important to note there isn’t a single, universally fixed global price.

For instance, a significant portion of tankers passing through Hormuz are headed to the Indian subcontinent, Asia, and as far as Australia and New Zealand. These regions heavily rely on Middle Eastern oil. When Hormuz is sealed off, countries like India and China must bid higher for barrels, which impacts global pricing.

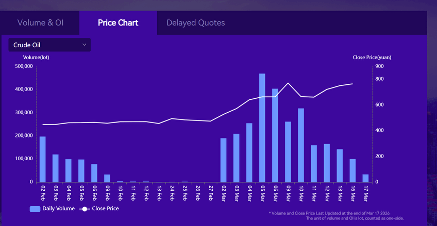

To demonstrate, here’s a pricing graph from China’s Shanghai Exchange:

Shanghai oil price on International Energy Exchange. Courtesy INE.cn/eng/.

As of Tuesday morning, March 17, a barrel of oil stood at 780 yuan, translating to around $114. But wait a second…

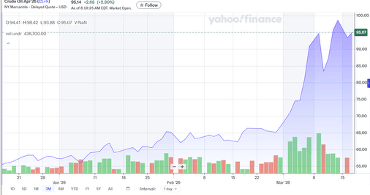

Meanwhile, on the New York Mercantile Exchange this same morning, an oil barrel traded near $95, as shown here:

NY Merc price of oil. Courtesy Yahoo Finance.

What explains the $19 gap—$114 in Shanghai versus $95 in New York?

One perspective is the distinction between purchasing “real” barrels and “paper” barrels. China must physically buy actual oil, given its heavy import dependence. Meanwhile, traders in the West—New York and London—often trade oil through futures contracts, buying and selling oil claims they expect to be fulfilled later.

To put it differently: Chinese refineries require guaranteed deliveries. Since China produces little domestic oil, its refiners are forced to import crude and cannot afford supply interruptions at their terminals. Therefore, Chinese companies push prices upward to ensure tankers stop at their ports rather than sail onward.

In essence, the genuine value of oil reflects what refiners pay now to get a tanker’s cargo offloaded—not the trading board prices for contracts. “Show me the money,” as the famous phrase goes.

This elevated Shanghai price can also be seen as a “scarcity premium” that Chinese refiners pay because, at present, they compete with other Asian and Australasian buyers for fewer oil shipments aboard a reduced number of tankers.

By contrast, the U.S. and broader Western Hemisphere still benefit, at least for now, from relatively abundant nearby resources—domestic production plus sturdy imports.

America the Fortunate

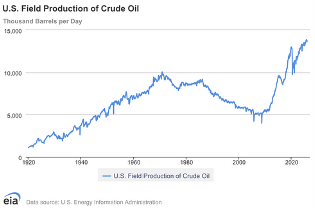

The United States is indeed fortunate to hold the position as the world’s top petroleum producer, generating approximately 13.8 million barrels per day—surpassing both Russia and Saudi Arabia (the latter is cutting output due to export hurdles).

Here’s an informative graph outlining U.S. production directly from the Department of Energy:

U.S. oil production since 1920. Courtesy Dept. of Energy/EIA.

The chart above exemplifies what Americans can describe as “energy security.” Since 1859 and Col. Drake’s discovery at Titusville, Pennsylvania, the U.S. has built an extensive, advanced oil and natural gas industry, spanning from exploration to extraction, transport, and refining. This is not the product of magic, but rather 167 years of sustained industrial development.

It’s important to understand, despite widespread belief, the U.S. does not produce all the oil it consumes. While pumping out about 13.8 million barrels daily, the nation’s usage hovers around 20 million barrels. The 6-million-barrel gap is filled primarily through imports from Canada (about 4 million barrels daily from Alberta) plus oil sourced from Mexico, Brazil, Nigeria, Angola, and most recently Venezuela.

Previously, a small portion of imports from Saudi Arabia was destined for a Saudi-owned refinery near Houston. That situation now remains uncertain.

Aside from imports, the U.S. is also an oil exporter. Some crude barrels leave the country, but a far greater volume is shipped out as refined products. For instance, most motor fuels and lubricants consumed in Central America come from U.S. refineries.

Additionally, gasoline and diesel trade between the U.S. and Europe is substantial, while Alaskan crude reaches markets in Japan, South Korea, and other Asian destinations.

The global oil market is quite fluid and complex, especially with the ongoing Hormuz closure, even as reports surface of tankers successfully navigating through with cargoes aboard.

Ultimately, every barrel will find a buyer at some price.

The Refinery Angle

Oil itself isn’t the product we directly consume. If you had a barrel of crude on your doorstep, you’d likely need a professional outfit to handle it.

Most consumers don’t use raw crude; instead, we rely on the finished products refined from it—such as gasoline, diesel, kerosene, jet fuel, lubricants, and other derivatives like tar and asphalt, which help make transportation smoother.

All these outputs come from processing crude through industrial facilities called “refineries.” You might have seen one while driving on highways—perhaps I-95 south of Philadelphia, “Refinery Row” in Houston, or near northern Long Beach in Southern California.

Valero refinery at Wilmington, California. Courtesy Valero Corp.

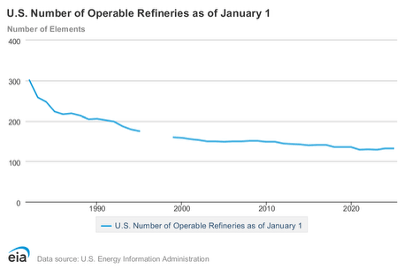

According to the EIA, as of January 1, 2026, the U.S. had 135 operational refineries—a significant drop from about 300 in the early 1980s. Here’s the data presented visually:

U.S. Refineries. Courtesy Dept. of Energy/EIA.

These refineries are spread throughout the country—from Alaska to Georgia and California to New Jersey—with a strong cluster along the Gulf Coast.

California is notable: the state went from 42 refineries in 1982 to just six now, contributing to the state’s ongoing fuel supply challenges. This fact also makes fuel a national security concern there, with prices among the highest nationwide, regardless of Hormuz.

These six refineries must produce different fuel blends to meet local sales needs and satisfy emissions regulations. Added taxes and legal complexities further raise operational expenses, complicating business efforts.

On a related note, someone recently suggested that if I cared about energy security, I should buy an electric vehicle. I was surprised to see “EV” and “energy security” mentioned together so casually.

Returning to refineries… having only 135 to serve 350 million people is not much. A simple calculation reveals roughly one refinery per 2.6 million residents, meaning any disruption at a refinery has the potential to significantly impact supply.

Currently, one challenge for U.S. refineries is the rising oil price. Even with abundant domestic and Canadian crude flows, global market prices influence local costs. So when crude prices climb from around $62 last month to roughly $95 now, that increase trickles down to refining costs.

About half of the price paid at the gas pump reflects the cost of crude oil entering the refinery. The balance accounts for refining, transportation, delivery to gas stations, and operating the pumps. Fuel taxes vary by state (California leads with the highest rates, closely followed by Illinois and Pennsylvania). Meanwhile, gas station operators earn only a few cents per gallon, so don’t fault them for higher prices.

Looking Ahead at Higher Fuel Prices

Regarding readers’ concerns about whether oil and gas prices will remain high: unfortunately, the answer is yes—likely for as long as Hormuz remains closed, and probably continuing long after any resolution of the conflict. Even if the war ended today, we would still experience its economic aftermath for months.

As Americans spend more at the pump, less money will be available for other purchases—whether it’s skipping a candy bar at the station, passing on a fast-food meal, saving on theater tickets, buying fewer groceries, or cutting back on shopping at stores like Walmart or Costco.

Your personal financial impact depends on your household income level. Here’s a chart for added perspective:

Consumer spending by income percentile. Courtesy Financial Times.

On the whole, rising fuel costs will noticeably strain the finances and lifestyle of many Americans. Roughly 60% of households live paycheck to paycheck, meaning funds diverted to gasoline or diesel leave less for basic expenses. So what goes to the pump comes out of other parts of the budget.

Sadly, despite political optimism about the economy, inflation-adjusted wages in much of working-class America have stagnated for over two decades. High-skill, well-paying tech jobs are dwindling due to AI, outsourcing, and imported labor; some work even shifts entirely overseas.

The bottom line: higher oil prices lift fuel costs, forcing consumers to spend more at gas stations but less elsewhere.

Looking ahead, inflation will rise, profits outside energy will fall, and broad market indexes may trend downward.

For investors, the recommendation is to favor energy firms with limited Middle Eastern exposure. U.S. refiners appear poised to benefit. Also, maintaining positions in gold and silver can serve as long-term hedges against inflation.

There’s plenty more to consider, but that covers the essentials for this St. Patrick’s Day. Let’s hope for some Irish luck amidst these challenges. Understanding the unfolding situation helps maintain composure as events develop.

Thank you for subscribing and reading. Best wishes…