Dieselflation Sparks Energy Emergencies

I hope you enjoyed your Easter break. Now we’re back to the usual rhythm, and oil along with refined fuel prices continue climbing relentlessly. There’s a lot to unpack as we strive to keep ahead of developments.

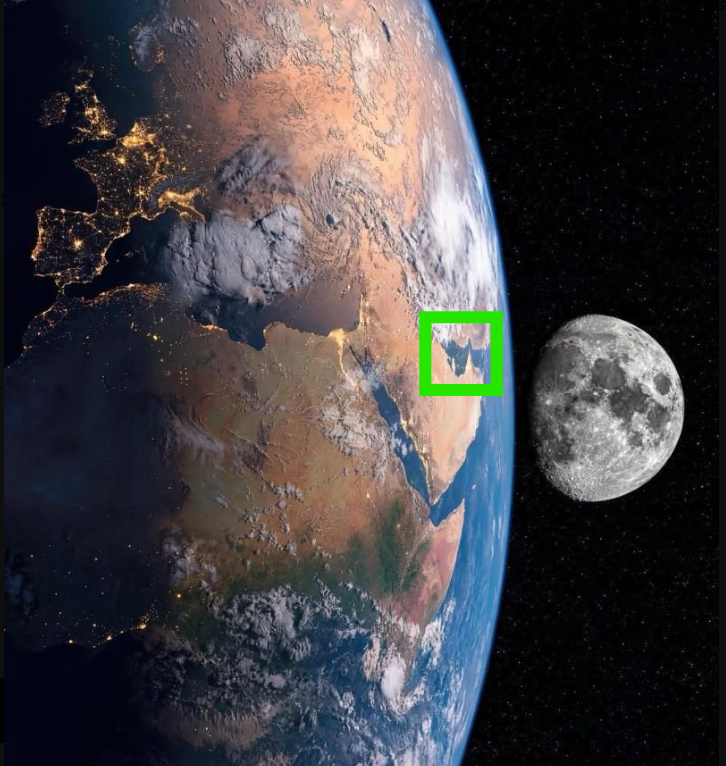

Before diving in, it’s interesting to note that among the eight billion people on Earth, only four spent these past days journeying to the Moon. A rather enviable feat.

North Africa, Europe, Eurasia and Persian Gulf (green box), plus Moon. Courtesy NASA.

I bring up the Moonshot because this striking image of Earth and the Moon together offers perspective, at least for me, to contextualize some of today’s challenges.

Moonshots While the World Keeps Spinning

At the heart of this picture is the brown Sahara Desert in North Africa, flanked to the east by the Red Sea and Arabian Plate. Above lies the Mediterranean Sea, with Europe outlined by scattered lights amid darkness. Further east and northeast stretches Eurasia. The editorially included green box highlights the Persian Gulf, also known as the “Arabian Gulf,” depending on perception.

Viewed from 250,000 miles away, despite weekend routines for most and the four astronauts in orbit, the Earth continued its steady rotation.

The ongoing Iran conflict still commands attention, including intense moments surrounding the rescue of American personnel behind enemy lines (a topic for another day). Meanwhile, closer to home, diesel prices climbed roughly 60 cents by last week’s end.

These matters—namely Iran and diesel—are intertwined and form today’s main focus. Simply put, the conflict has fueled oil cost surges, pushing up diesel and refined fuel prices, guaranteeing inflation ahead—what might be called “dieselflation.”

Let’s delve deeper into this situation…

Well-Traveled Barrels of Oil

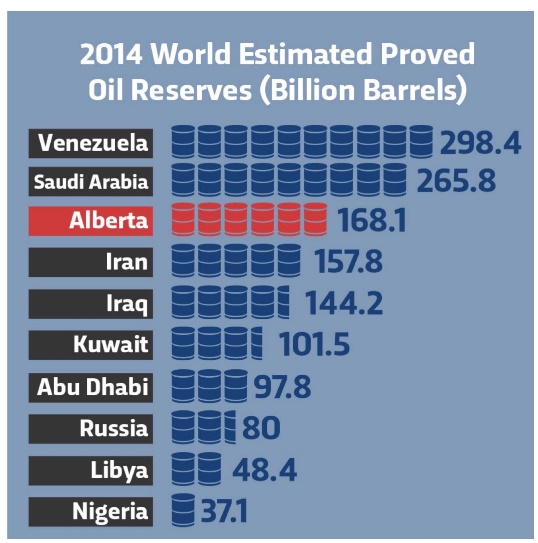

There’s a vast supply of oil worldwide, yet a significant concentration resides in the Middle East. This chart presents a ranking of nations by estimated oil reserves (in billions of barrels).

Estimated oil reserves by nation (and Alberta). Courtesy @RazorOil.

The list prominently features familiar Middle Eastern players: Saudi Arabia, Iran, Iraq, Kuwait, and Abu Dhabi, all major oil exporters. The graph excludes Qatar, which is highly significant in natural gas.

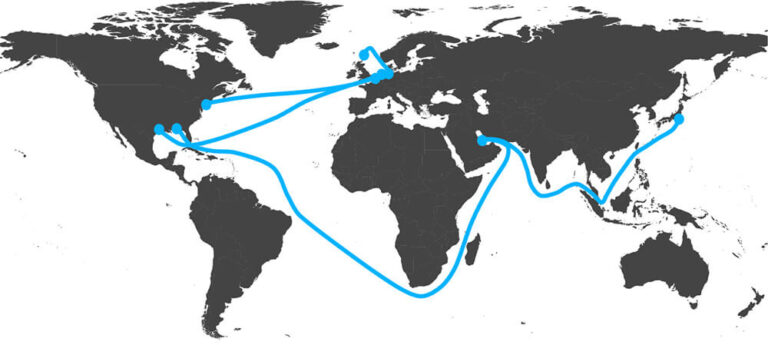

Oil, liquefied natural gas (LNG), and refined fuels move worldwide on tankers taking anywhere from 30 to 90 days, depending on the route, linking the Gulf to destinations across Europe, Africa, South Asia, East Asia, and the United States.

Notional – very cursory – chart of global tanker routes.

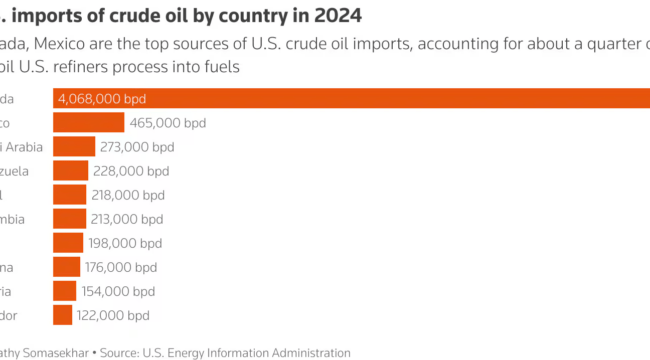

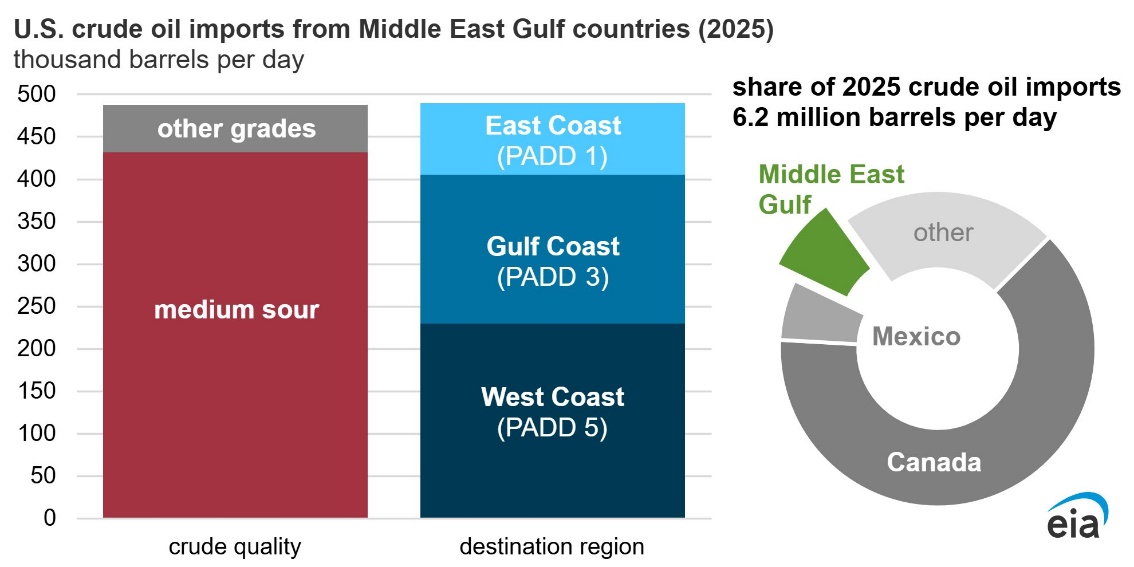

Contrary to popular belief, the U.S. did import oil from the Middle East. Last year, around 8% of the U.S.’s imports—nearly half a million barrels daily—originated from the Gulf. Here is a detailed breakdown:

U.S. oil imports, especially from Gulf nations., Courtesy Dept. of Energy/EIA.

Much of this imported Middle East oil is categorized as “medium sour,” rich in sulfur, which suits many American refineries adapted to process this type of crude. Keep this in mind as we explore more about American oil imports.

America’s Many Imported Barrels

Looking back at the graph showing U.S. oil sources, it is clear that the majority of imports—approximately four million barrels per day—come from Canada, specifically from Alberta’s oil fields (refer to the Alberta reserve graph above).

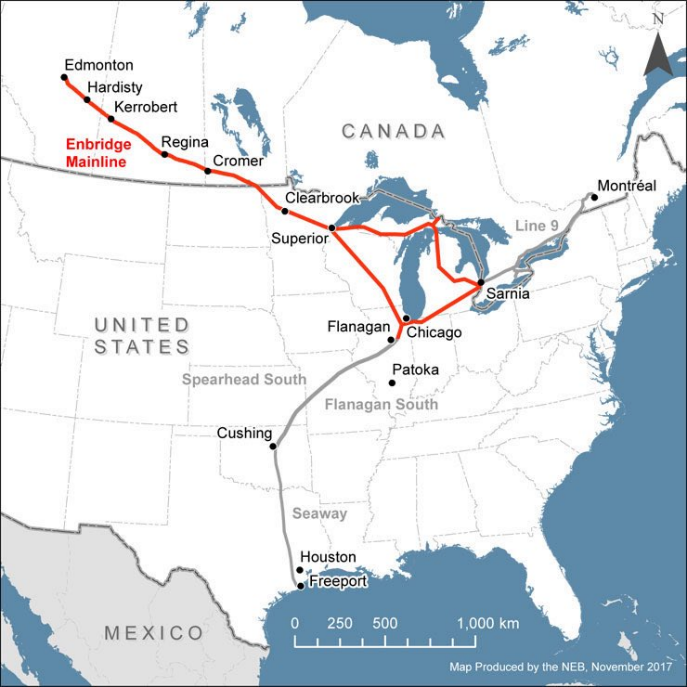

Here is a map illustrating a key pipeline system, the Enbridge Mainline from Alberta, which transports roughly three million barrels daily to the U.S. Midwest. (This system could have been even larger had President Biden not – stupidly! – halted the Keystone XL project in 2021.)

Enbridge Mainline, moves Alberta crude oil to U.S. Courtesy @RazorOil.

No pipeline in North America surpasses the Enbridge’s daily capacity of three million barrels, including the Alaska Pipeline. This underscores Canada’s vital role in supporting the U.S., particularly the Midwest and Gulf Coast refineries, with energy supplies.

By comparison, Alberta’s oil exports greatly outpace those of Venezuela, which produces under one million barrels per day. Venezuela’s heavy, tar-like crude faces added logistical challenges, requiring transport to its Caribbean coast before sea shipment to Houston. In terms of logistics alone, Canadian oil is a logistical advantage over other imports, including those from closer countries such as Venezuela.

Additionally, the EIA data shows U.S. Middle East oil imports are split nearly evenly between Gulf Coast refineries and the West Coast, mainly Southern California.

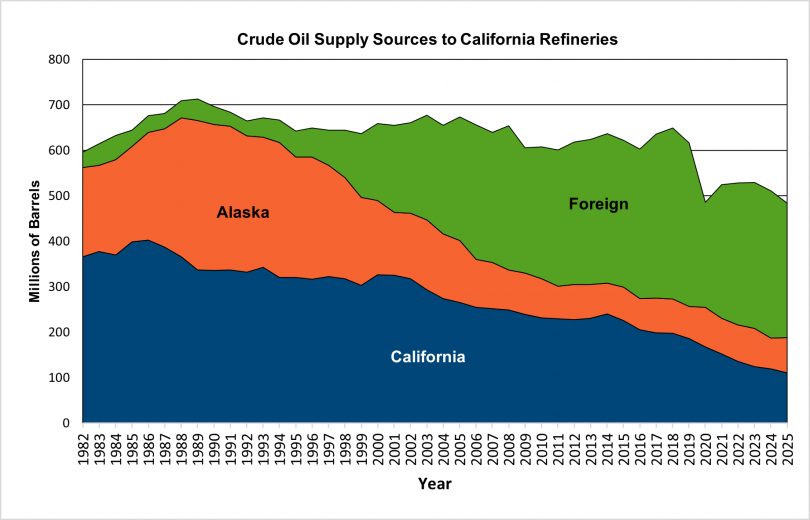

Gulf Coast imports largely involve Saudi crude flowing into a Saudi-owned refinery near Houston. The California imports, mostly from Saudi Arabia but not exclusively, emphasize a serious concern on the West Coast: a shortage of local and regional oil supplies for California’s six remaining refineries (down from over 40 previously), as illustrated here:

Oil supply to California refineries. Courtesy California Energy Commission.

So, what’s amiss here? Up until the early 2000s, California generated most of its oil, supplemented by Alaska’s production. Now, that’s no longer the case.

Over the last 25 years, oil exploration and extraction in California has been severely limited by taxes, litigation, and regulations, despite available hydrocarbon resources (a long and complex story). The same decline is true for refineries, many of which have shuttered during this period.

Meanwhile, California’s population grew steadily (until recent years when political issues caused some outmigration). Anyone visiting the state can attest to the increased number of vehicles, planes, trucks, and trains—all consuming fuel—in spite of aggressive “green” initiatives.

However, with fewer refineries operating and diminishing local or regional crude production, California fuel costs have soared to some of the highest nationwide. As reported recently, diesel prices are exceeding $8 per gallon there.

The key takeaway is that most of the U.S. maintains a reasonably stable supply of crude. Mid-continent and Gulf Coast refineries benefit from a mix of domestic, offshore, and Canadian oil imports.

Conversely, the West Coast faces a starkly different reality, impacting California and, by extension, states like Nevada and Arizona, which rely heavily on California refineries or imported refined fuels.

West Coast Will Soon Have BIG Problems

We’ve covered significant ground regarding the origins of oil and refining infrastructure.

A major conclusion: California is confronting serious challenges with both oil supply and refining capacity. Since much oil processed there comes from imports, global disruptions have severely affected this flow. Moreover, California depends heavily on imported refined fuels. The question is—from where?

Shockingly, until recently, a large portion of California’s diesel was refined in South Korea. In practice, crude might be shipped from Saudi Arabia to South Korea for refining, then shipped back across the Pacific to California. However, the Iran war is disrupting this cycle.

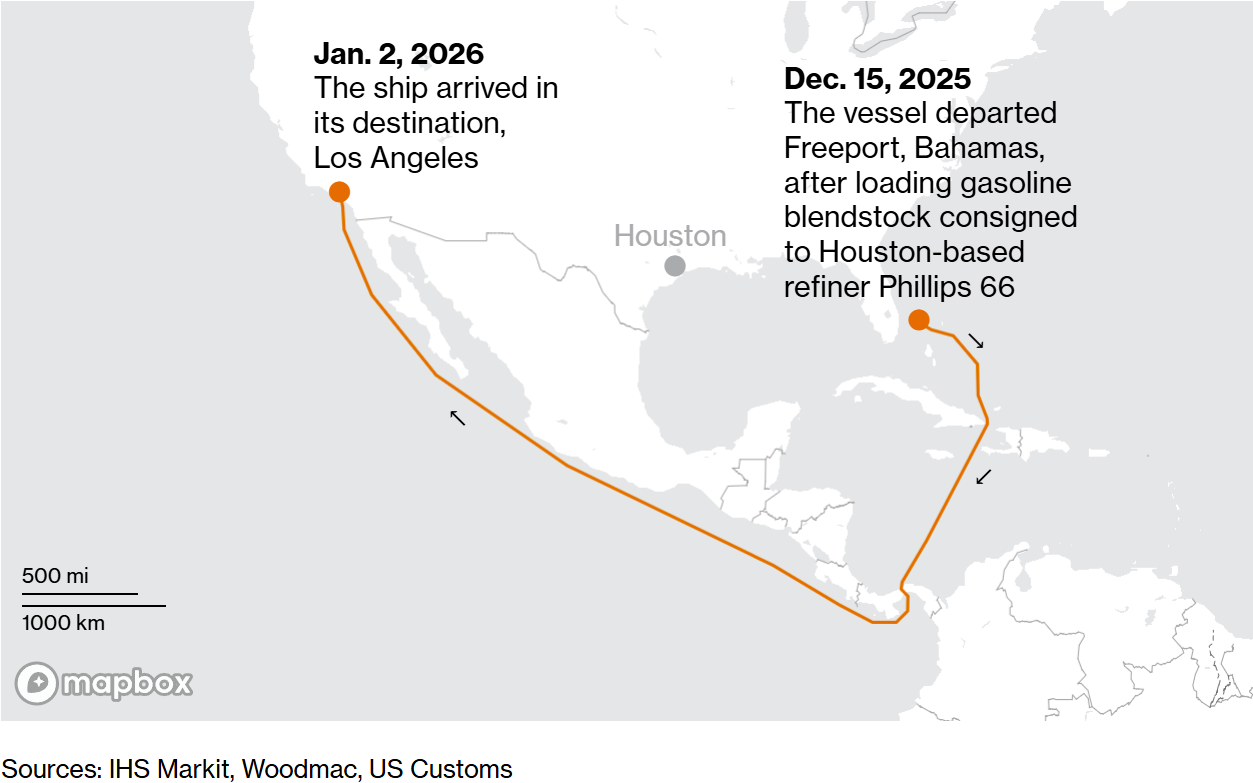

The U.S. Gulf Coast also supplies refined products to California, but these take a complicated detour through the Bahamas (due to the Jones Act) and transit the Panama Canal.

Recent refined product shipment from Houston to Bahamas to California. Courtesy Bloomberg News.

Put simply, California is geographically isolated, and its neighboring states Arizona and Nevada rely mainly on California’s fuel supplies. This spells trouble ahead with climbing gasoline and diesel prices across the West Coast and surrounding regions.

Fuel costs have already surged everywhere; for instance, Pennsylvania saw a 30-cent diesel increase just last week. But prices in California are significantly higher, and further spikes are expected.

Recall those 90-day tanker journeys from the Middle East. Many tankers delayed in early March due to the conflict and Persian Gulf blockade are now absent from unloading docks worldwide—from Pakistan to New Zealand and, crucially, California.

Without crude supplies, refineries globally face shortages of feedstock needed for refining. Therefore, within the next 15 to 45 days—roughly by late April or early May—refined fuel shortages will emerge in many regions, especially in the western United States.

Asia is already feeling the pinch:

- The Philippines declared a national emergency, with fuel reserves below five days.

- Pakistan imposed a four-day workweek to cope with the crisis.

- Bangladesh enforced curfews limiting fuel use past 6:00 pm.

- Thailand halted much of its fishing fleet for lack of diesel.

- China faces long lines at fuel stations and banned exports, including those to Australia and New Zealand, which lie at the far end of the global fuel supply chain.

Is this a bleak outlook? Yes, unfortunately. But it highlights a stark reality: energy supply disruptions will fuel inflation—“dieselflation,” as mentioned.

The takeaway for all nations: avoid simplistic, reactionary energy policies. Instead, focus on developing domestic oil resources, constructing your own refineries, and maintaining good relations with resource-rich regions like Alberta.

Looking ahead, the question arises: “What will the true price of oil be?”

There are speculative barrels traded on exchanges, but then there’s real crude—the physical product trapped by halted exports out of the Persian Gulf. Consequently, refineries globally must pay premium prices to secure crude.

Brent barrels, a key international benchmark, recently traded as high as $160 per barrel according to recent data. Reports tell of tankers altering destinations multiple times across Asia as refineries compete fiercely for limited supplies. The market is volatile indeed.

For those in the U.S., consider yourselves fortunate. At minimum, we maintain access to oil and fuel, unlike Australia with only two refineries and insufficient domestic oil to meet demand, or New Zealand which operates with zero refineries, importing all refined fuels and lubricants.

For investors, the simplest strategy is to focus on oil firms with minimal Middle East exposure, such as Petrobras (PBR), alongside U.S.-based producers. Also consider oil service companies like Schlumberger/SLB (SLB), Halliburton (HAL), or the OIH fund. (Note, these are not formal recommendations; no Reckoning portfolio is offered.)

That wraps up this update. Thank you for reading and being a subscriber.