SMRs and the Uranium Miner Opportunity

The major breakthrough in nuclear energy today is its shift in scale. Traditionally, nuclear plants were enormous installations.

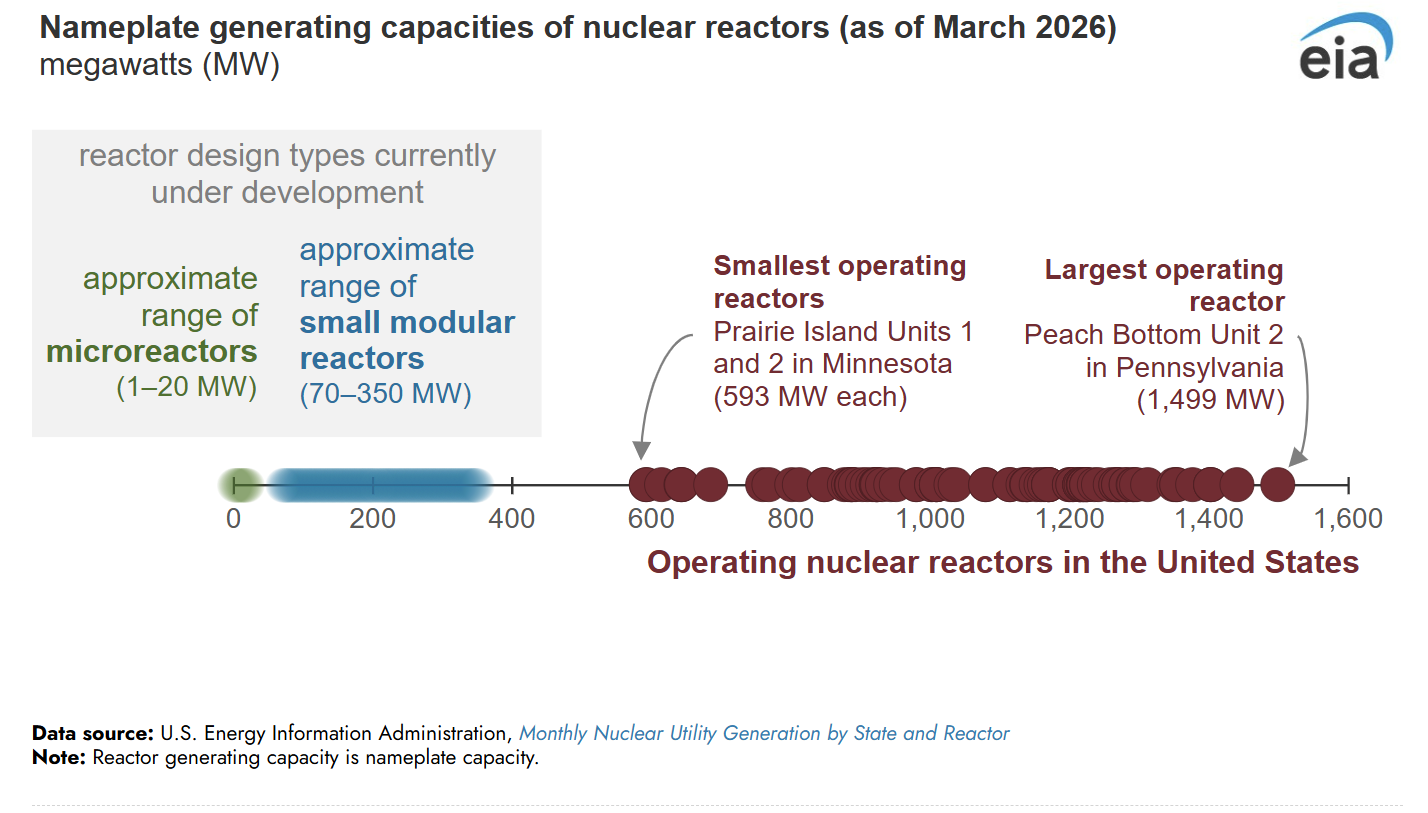

As illustrated in the chart below, existing nuclear facilities produce between 600 and 1,500 megawatts.

Such plants come with extremely high costs. The latest reactors completed—Georgia’s Vogtle Units 3 and 4—came with a price tag of around $15,000 per kW, equating to roughly $16 to $17 billion each. Moreover, these projects require extensive time for planning, permitting, and construction.

Building new nuclear sites in the U.S. is rare nowadays. Most operating nuclear plants were commissioned before 1990. Since 2000, only three new facilities have been constructed, including the Vogtle Units, while over 30 plants were decommissioned during that period.

Jacopo Buongiorno, professor of nuclear science and engineering and Director of the MIT Center for Advanced Nuclear Energy Systems, notes that cost overruns and construction delays largely caused nuclear power to lose ground to other energy sources.

This trend is shifting with the arrival of small modular reactors (SMRs).

In Oak Ridge, Tennessee, two new SMRs (Kairos Power Hermes 1 & 2) operate in a demonstration setup that will later connect to the power grid.

The military is also developing small reactors. The Air Force intends to build one at Eielson AirForce base in Alaska next year, while the Army’s Janus program aims to deploy multiple SMRs across various bases.

On the commercial front, NuScale Power (ticker: SMR) and the Tennessee Valley Authority plan to install SMRs at the Clinch River site. Similarly, Holtec International is developing two 300-megawatt SMRs at its Palisades location in Michigan, targeting operation by 2031.

There is considerable interest in utilizing SMRs for powering data centers. For example, X-Energy (ticker: XE), Energy Northwest, and Amazon (ticker: AMZN) are collaborating to construct a facility in Washington state with a capacity of up to 960 MW—making it a substantial energy project.

The U.S. government supports these innovations, which is a positive signal for companies involved. It is essential that the regulatory process is simplified to help projects stay on schedule.

Past decades have seen projects hampered by bureaucratic delays, though efforts during the Trump administration sought to improve permitting efficiency.

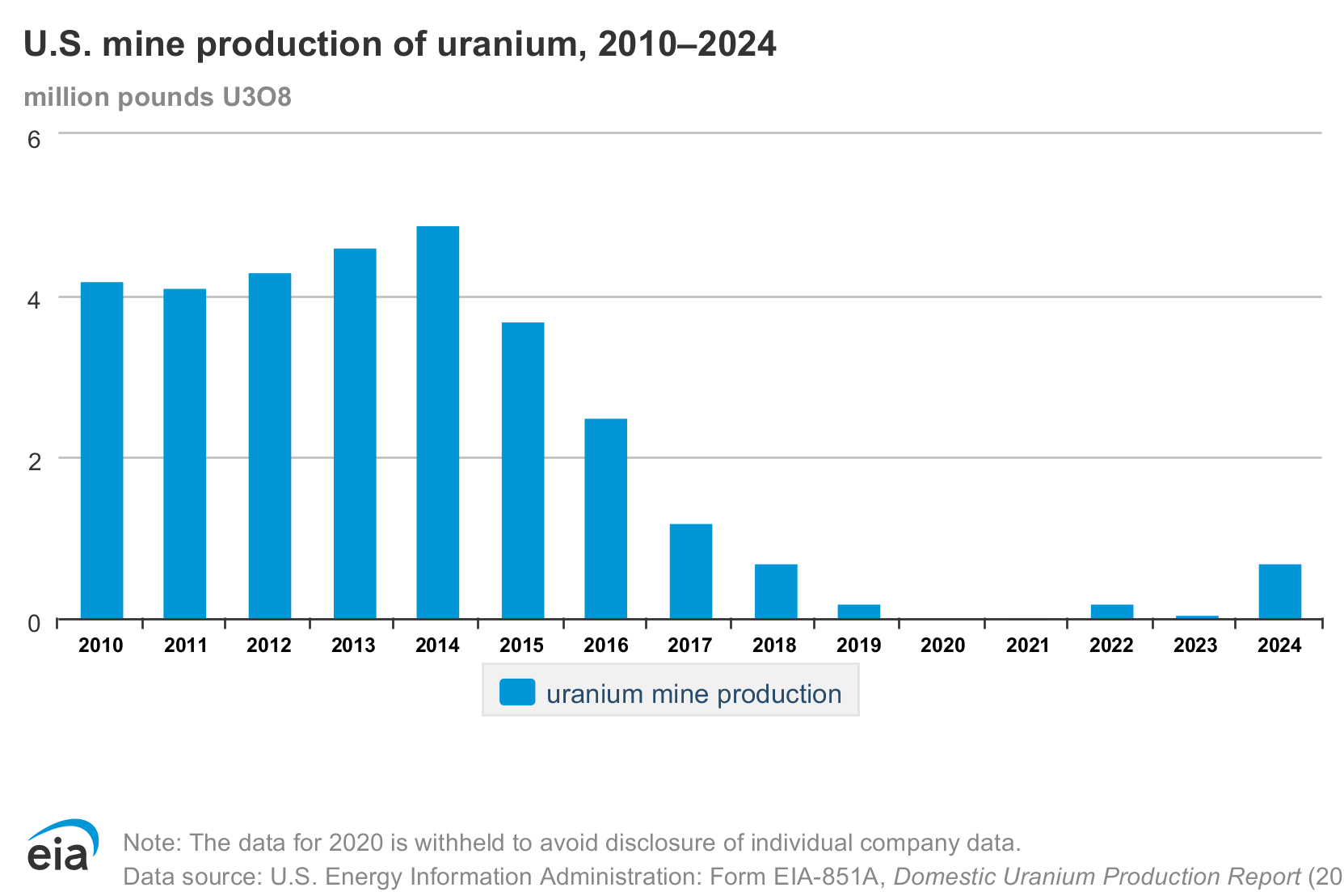

However, the challenge soon will become supplying fuel for these new nuclear units. The current status of uranium mining in the U.S. is shown here:

The issue is clear: domestic uranium production is insufficient.

Each new SMR demands between 300 and 500 tons of uranium fuel annually. Considering that producing one ton of reactor fuel requires about 45 to 50 tons of mined (yellowcake) uranium, a single SMR would increase uranium demand by approximately 13,500 to 25,000 tons.

The U.S. currently mines around 680,000 tons of uranium each year. However, total consumption is closer to 5 million tons annually, reflecting a substantial gap. This means each additional SMR will intensify the existing supply shortfall, and many SMRs are under development.

Small modular reactors are poised to rejuvenate nuclear energy in the United States, yet much higher uranium output is necessary to satisfy expanding needs.

Although these reactors are smaller, their fuel requirements remain substantial—needs that the current supply cannot meet. Consequently, U.S. uranium mining companies represent a compelling investment prospect for the coming decade.