Tax the Rich, Watch Them Leave

California is a stunning state blessed with abundant natural beauty and a thriving technology sector.

Unfortunately, it is hampered by some of the least competent politicians.

This November, voters in the Golden State will decide on implementing a wealth tax.

The proposal calls for a “one time” 5% tax on the total net worth of billionaires—not just their capital gains. This notion carries substantial risks, which we will examine today.

Fleeing Billionaires

The surge of tech wealth once meant California was home to many billionaires, but they are quickly departing.

The California Tax Foundation reports that $777 billion in wealth has already exited the state, and this figure only accounts for those departures made public.

Notable billionaires leaving or having left include:

- Google co-founders Larry Page and Sergey Brin

- Oracle founder Larry Ellison

- Tesla and SpaceX founder Elon Musk

- Uber founder Travis Kalanick

- Billionaire investor David Sacks

These are just some of the prominent wealthy individuals exiting California.

Over time, the state stands to lose far more revenue than the wealth tax would generate. Billionaires contribute tens of millions in taxes annually, fund startups, and uphold many well-paying jobs.

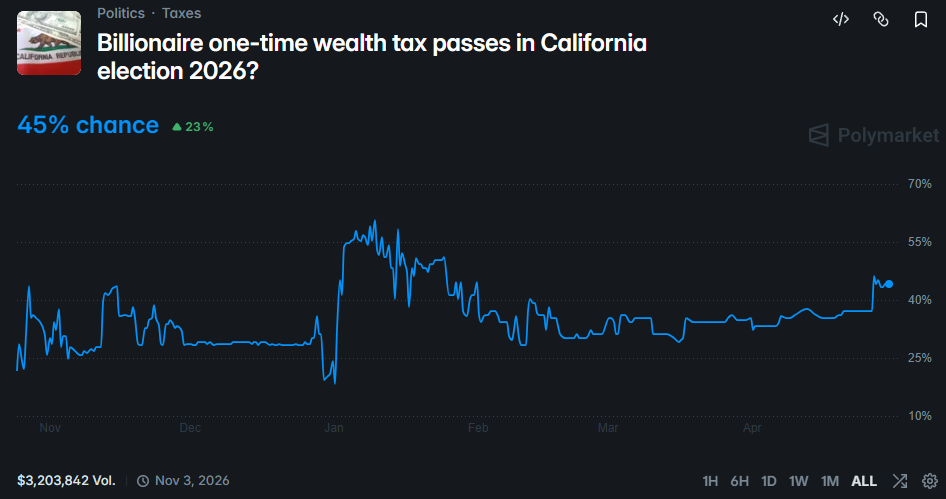

Yet, passage seems possible. On Polymarket, the odds of the wealth tax passing have climbed to 45%, up 23% since last year.

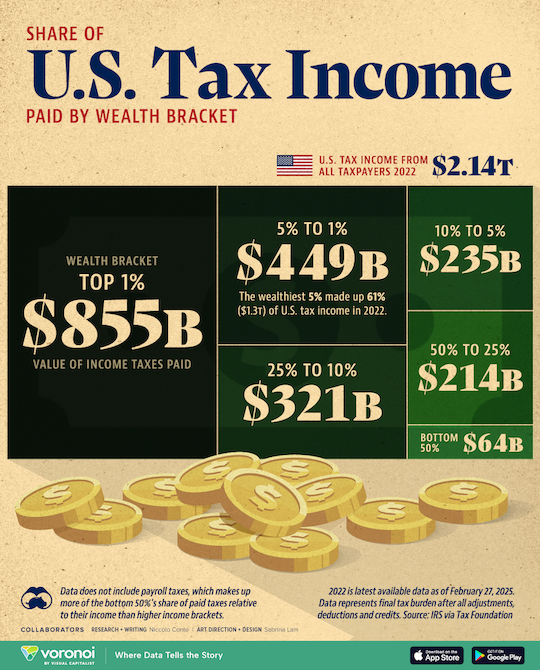

All this in pursuit of billionaires “paying their fair share.” But in America, the top 10% already contribute 77% of income tax.

Source: Visual Capitalist

If approved, this tax could hasten California’s financial decline.

When the next recession arises, what is now a “one time” tax will likely extend to a broader population. “First they came for the billionaires, and I did nothing because I wasn’t a…”

The state that once shone so brightly is now dimming. Urban crime surges as Soros-backed District Attorneys release offenders for serious offenses. Generous benefits attract homeless populations seeking relief here.

As Byron King pointed out this week, California has shuttered most of its refineries and restricted drilling. Diesel prices soar near $8 a gallon, while reckless government spending has severely damaged the budget.

A wealth tax would be the final blow.

Chase the Money Out

Back in 2000, France introduced a wealth tax requiring millionaires to pay up to 1.5% of their net worth annually, alongside a 75% top income tax rate.

The outcome was disastrous. At least 42,000 millionaires escaped to Switzerland, the U.K., and other countries.

Tax revenues declined. Business owners relocated their operations elsewhere.

Why aren’t many major companies emerging from France now? Because the excessive taxation has driven entrepreneurs away.

In 2017, France scrapped the wealth tax, though the damage was irreversible. Tax rates remain onerous, stifling innovation and economic growth.

Don’t Give Them an Inch

In 1939, only about 5% of Americans were liable for federal income tax.

By 1945, that figure exceeded 60%, with most paying a share to the federal government.

This pattern tends to repeat: taxes rise for emergencies and rarely decline after those crises subside.

Before long, public sector salaries inflate beyond $200k annually, with hiring spiraling out of control.

This story is unfolding nationwide, but it’s especially severe in solidly blue states.

State Matters More Than Ever

In Maryland, we contend with some of the nation’s steepest taxes—which continue to climb.

In recent years, two close friends relocated to Florida and Texas for better financial conditions. One is a surgeon; the other, a CPA.

After our children finish school, my wife and I will likely follow suit. Paying state income taxes on top of federal, sales, capital gains, and more has become unreasonable. This might be tolerable if these heavy taxes delivered exceptional public services.

But they do not. Roads are riddled with potholes. Corruption permeates every layer of government. We face continuous battles to avoid being removed from top-tier school districts through re-districting.

The outlook for high-tax states is grim. Pension systems are underfunded, debts soar, and expenses keep rising.

A difficult fiscal reckoning will eventually be unavoidable at both state and federal levels. Budget cuts will be necessary, including staff reductions and potentially trimming pension benefits and healthcare coverage.

There is no escaping this reality.

When that day arrives, residing in a fiscally prudent, low-tax state will be the smart choice. It’s unfortunate, but that is the current state of affairs.