Druckenmiller’s -$3B FOMO Moment

By 1999, Stan Druckenmiller had already earned legendary status.

Between 1981 and 2000, his hedge funds experienced no losing years.

He consistently generated astonishing average returns of 30% annually. His success caught the eye of George Soros, and Druckenmiller soon took charge of the famed Quantum hedge fund.

In 1999, noticing the tech bubble inflating, Druckenmiller established a $200 million short position in technology stocks.

However, the bubble kept expanding, causing his short position to lose $600 million.

To counter this, he brought in two young tech “gunslingers” to manage some capital. They purchased the hottest stocks and quickly started earning 3% daily.

The ambitious tech traders made their seasoned boss appear outdated.

Druckenmiller explains how FOMO (fear of missing out) gripped him:

“So like around March [of 2000] I could feel it coming. I just — I had to play. I couldn’t help myself. And three times the same week I pick up a phone — don’t do it. Don’t do it. Anyway, I pick up the phone finally.

I think I missed the top by an hour. I bought $6 billion worth of tech stocks, and in six weeks I had left Soros and I had lost $3 billion in that one play.”

Let’s take a moment to consider this—one of the all-time great investors bought at the very peak of the dotcom bubble and suffered a colossal $3 billion loss.

Druckenmiller later admitted he knew it was a poor decision but simply couldn’t resist the urge.

“I didn’t learn anything. I already knew that I wasn’t supposed to do that… I was just an emotional basketcase and I couldn’t help myself.”

This story highlights how FOMO can dominate rational judgment. Watching prices surge often pushes even the smartest to make irrational moves.

Berkshire’s $397B Cash Hoard

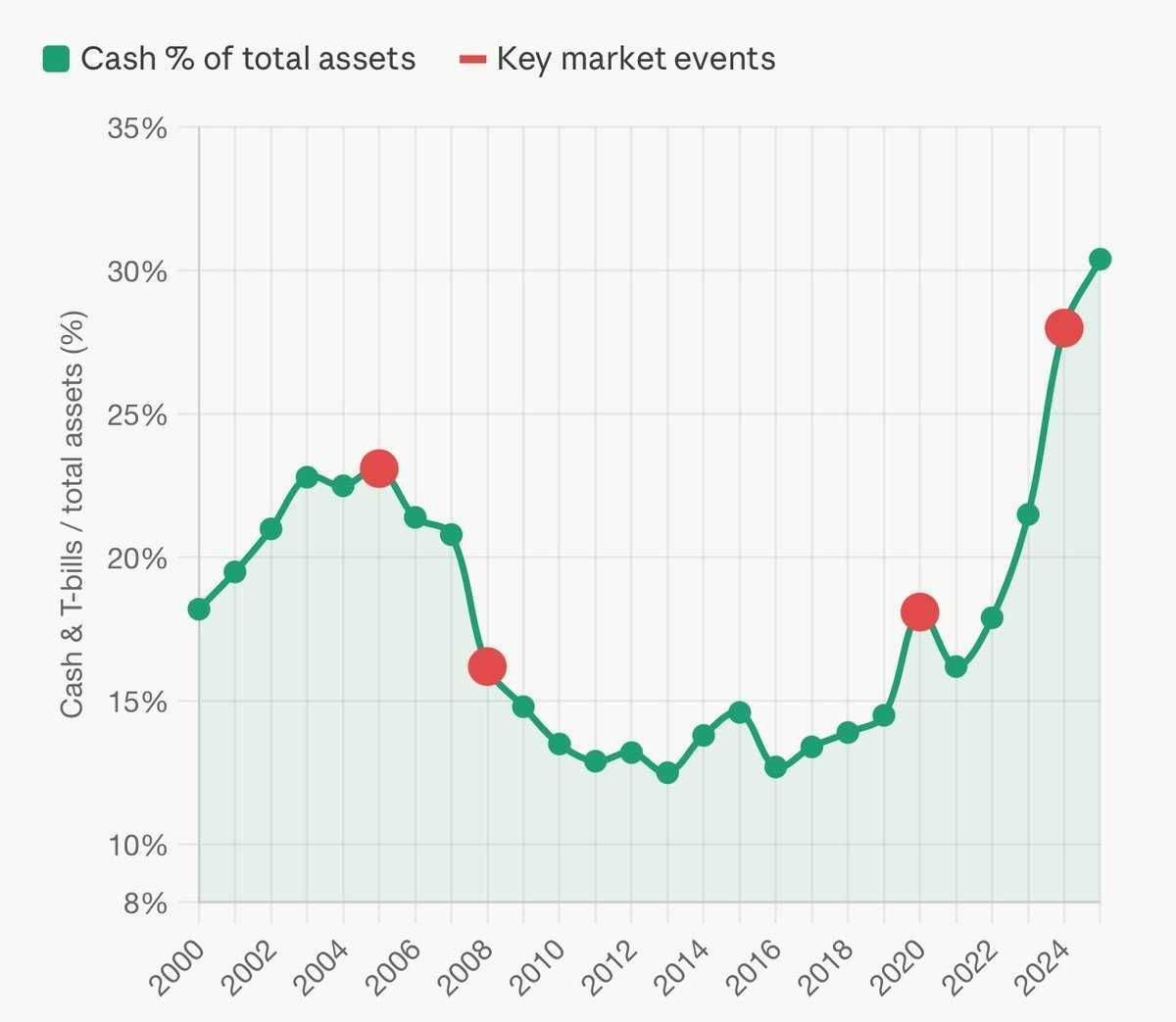

Berkshire Hathaway (BRK.A, BRK.B), the iconic company created by Warren Buffett, currently holds a staggering $397 billion in cash and Treasury securities.

That amount represents nearly one-third of Berkshire’s total assets. Meanwhile, this capital only earns 3-4%, even as the market continues to surge. For instance, the S&P 500 climbed 10% in April amid what ranks as one of the most severe energy crises ever—a market clearly disconnected from logic.

Nevertheless, Berkshire remains steadfast. They prefer to wait patiently for “fat pitches”—meaning market crashes that offer highly discounted stocks.

The company employed the same strategy before the 2008 financial crisis, accumulating cash reserves up to 23% prior to the downturn.

When those attractive buying opportunities appeared, Berkshire was ready to act. A memorable example is their Gambit with Goldman Sachs (GS) when confidence in banks was shaky.

Buffett acquired $5 billion in preferred shares that paid a 10% dividend indefinitely. Additionally, Berkshire received warrants to purchase $5 billion in common stock at $115 per share. Goldman Sachs shares now trade around $917.

Their smartest crisis-era investment was Bank of America (BAC), which yielded an impressive $20 billion profit.

Buffett’s team also snapped up shares of GE, Dow Chemical, and other companies at fire-sale prices during the downturn.

This approach underscores the value of disciplined patience and readiness.

However, Buffett purposely limits his opportunities. He avoids emerging market equities and dislikes investing in precious metals.

While holding some cash is wise, it isn’t necessary for investors to maintain as much as Berkshire’s 32%.

Assets With Less Downside, Huge Upside

Before diving in, a clarification: the following advice relates to long-term investment strategies. Short-term trading in popular stocks is a different matter.

For the long haul, my portfolio favors assets designed to endure market turbulence—such as natural resources, emerging markets, and precious metals. Many investors could benefit from increasing exposure to these areas.

When a market collapse occurs, having too large a share in overcrowded sectors can be risky. The exit will be narrow, with masses trying to get out simultaneously.

For instance, from 2000 to 2002, the Nasdaq plummeted 78% peak to trough, while the S&P 500 dropped nearly 49%.

During that same period, oil stocks gained around 20%, including dividends. Gold miners performed even better, with the NYSE Arca Gold BUGS Index surging over 100% between 2000 and 2002.

Natural resource equities outpaced the broader market for another eight years following that period.

Moreover, emerging markets outperformed both the S&P 500 and Nasdaq during the dotcom collapse. The MSCI EM index fell roughly 25%, quickly bounced back, and beat U.S. stocks in the subsequent years.

The takeaway is straightforward: U.S. stocks are currently costly. Historically, such valuations have resulted in very modest future returns.

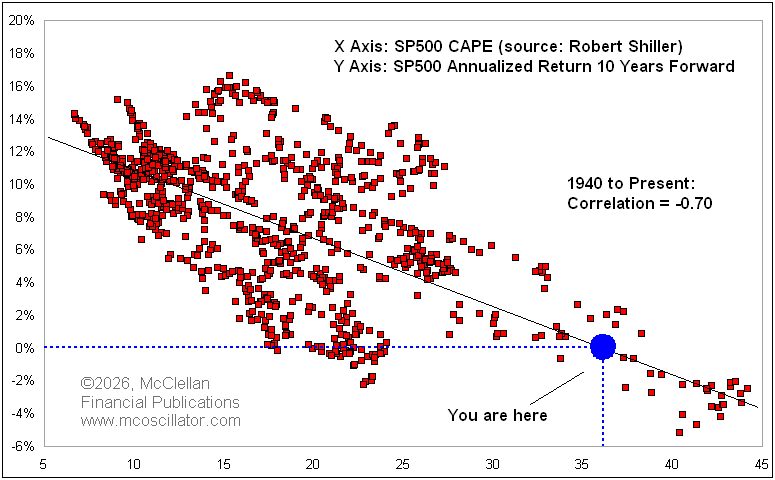

The chart below illustrates the CAPE ratio (a 10-year metric for stock valuation) of the S&P 500 on the x-axis versus subsequent annualized returns on the y-axis.

With today’s CAPE near 36, expected returns over the next decade have averaged close to zero.

Source: Tom McClellan

The S&P 500 might still surge another 15%, but that would likely mark a “blow-off” top before a crash inevitably arrives. Afterward, the recovery of overpriced stocks is unpredictable; it took more than ten years after the 2000 dotcom bust.

I’m not suggesting you dump all your expensive stocks. Rather, I advise diversifying into alternative investment categories like natural resources, emerging markets, and precious metals.

Eventually, the moment will come to sell these less conventional assets and transition back into traditional growth and income stocks.

That shift will only make sense once yields on “normal” U.S. equities rise significantly and stock prices fall considerably.

To emphasize—this guidance is aimed at long-term investors. For short-term traders, chasing high-priced stocks can be profitable, provided risks are well managed.