Worst Case Scenario – Rejected

As the Iran conflict draws to a close, it’s an opportune moment to reflect on the lessons gained.

Barring any disastrous setbacks to the agreement, the Strait of Hormuz is expected to reopen completely soon.

Crucial commodities such as oil, natural gas, and fertilizers will once again move without restrictions through this key maritime bottleneck.

Let’s take a look at what this confrontation has taught us about energy markets and the global economy.

Exaggerated Damage?

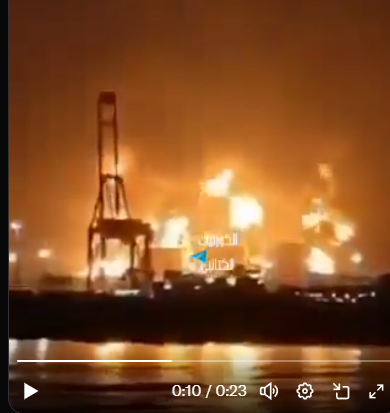

In mid-March, when Iran targeted Qatar’s vast Las Raffan liquefied natural gas (LNG) facility, the outlook appeared grim.

LNG is vital as both an imported fuel and industrial input. It generates power, is essential for fertilizer production, and fuels heating and cooking.

Since Qatar supplies approximately 20% of the world’s LNG, the Iranian missile strikes on its main hub seemed calamitous.

Qatar’s Ras Laffan LNG hub

Officials in Qatar initially claimed that at least 17% of production was halted and projected repairs would take between three to five years.

Moreover, the closure of the Strait reportedly triggered numerous issues that were expected to take months or years to resolve.

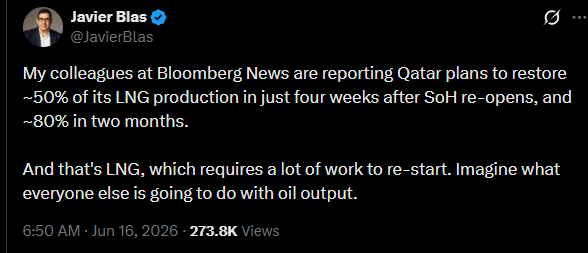

However, more recent reports offer a brighter perspective. Bloomberg energy analyst Javier Blas indicates Qatar’s LNG output should recover to 80% capacity within two months.

Source: X

The full extent of damage to Gulf oil fields and refineries remains unclear. Yet, some early damage assessments seemed likely exaggerated in the heat of the moment.

This is understandable, as Qatar and other major energy producers had reasons to emphasize the severity: “You’ve already damaged us enough, we won’t recover for years!”

Whether intentionally overstated or not, this narrative benefited both sides. Iran claimed accurate, asymmetric missile impacts, while affected countries avoided enduring, catastrophic harm.

China: Tougher Than We Thought

When the war began, a prevailing theory suggested it was largely a move targeting China.

The reasoning was simple. Since China imports about 11 million barrels of oil daily, mainly from the Persian Gulf, any disruption at Hormuz would supposedly devastate its economy.

Though I don’t believe the Iran conflict focused primarily on China, if it did, that strategy failed.

Beijing clearly anticipated such disruption. Here are three reasons shortages were avoided:

- Electric vehicles – Over half of new car sales in China are now electric

- Oil stockpiles – China holds the world’s largest reserves, totaling 1.5 billion barrels

- Coal-to-liquids conversion – Significant progress has been made turning coal into diesel and other fuel substitutes

Previously, many believed China’s vulnerability lay in dependence on Middle Eastern oil. Yet, the nation didn’t tap its reserves until mid-May and then withdrew much less crude than the U.S., around half a million barrels daily.

Last month, China even began exporting jet fuel and diesel to neighboring countries suffering from shortages—a surprising development.

Over the last decade, China has electrified transportation, expanded pipeline imports from Russia, strengthened its domestic oil industry, and amassed large crude stockpiles.

This preparation signals China is moving toward reduced reliance on Middle Eastern oil—a vital insight that enhances its energy security and resistance to economic pressure.

Worst Case Scenario – Rejected?

At the start of 2026, WTI Oil traded near $57 per barrel, whereas today it hovers around $77.

Reestablishing pre-conflict levels of shipping through the Strait of Hormuz will take time due to mine clearing and logistical challenges.

Additionally, global stockpiles and strategic reserves will need replenishing, which will keep oil prices above average for some time.

Yet, the feared extreme shortages did not materialize. Oil did not surge to record highs nor remain above $110 per barrel for long.

Still, price hikes in oil, fertilizers, and gas exacted a toll on both consumers and businesses.

Emerging markets faced noticeable strain, and the full impact of fertilizer deficits on agriculture remains to be seen.

Inflation is expected to stay elevated for a while, but it appears the worst-case outcome was avoided.

That said, stock markets will not necessarily keep climbing indefinitely. A sharp selloff is underway and may persist. Personally, I favor hard assets, precious metals, and emerging markets over hot sectors like tech.

Israel, Lebanon, and Iran

There remains a chance for the peace agreement to be disrupted, pushing us back into crisis. Israel, a key ally in the conflict, is openly dissatisfied with the proposed deal.

I expect these tensions can be resolved without resuming active warfare, as too much is at stake. However, any setbacks would probably center around these disputes.

The memorandum of understanding (MOU) calls for an end to hostilities on “all fronts, including Lebanon.” Yet Israel insists ongoing operations are necessary to prevent Hezbollah assaults on northern settlements and IDF border forces.

Tensions between President Trump and Israeli leaders are clearly escalating.

Source: X

President Trump’s remarks are intriguing and somewhat concerning. What does it mean to let “Syria take the lead against Hezbollah instead”?

This would effectively be shifting into a different conflict. It seems he might be frustrated that the Lebanon-Israel issue is a major obstacle to the deal and is exploring alternatives. Nonetheless, Iran remains steadfast in defending its Hezbollah proxies, and Syria is unlikely to engage in fighting them.

Trump’s clear priority is resolving the Iran situation quickly. With midterms approaching, prolonged closure of Hormuz could reignite crisis conditions. Therefore, I believe the agreement will be finalized.

It’s crucial to monitor this area closely since any failure would likely stem from these tensions. Still, I’m doubtful we’ll revert to a full-scale war with Hormuz closed. It looks like we’re headed toward a more peaceful Middle East phase, at least for the time being.

What to do with Oil Investments?

I have discussed Brazilian oil giant Petrobras (PBR, PBR.A) extensively. Like many oil majors, Petrobras has declined significantly from wartime peaks.

However, lower oil prices might benefit Petrobras. Because the Brazilian government regulates gasoline and diesel prices, Petrobras has had to heavily subsidize domestic fuel costs.

With oil prices falling, that financial burden will lessen. Though export revenues could decrease, Petrobras remains profitable with a roughly $40 all-in cost per barrel.

I’m currently holding Petrobras shares and plan to reinvest dividends over the long term. I may reduce my stake somewhat this year due to its size, but it’s a core holding alongside my investments in gold and silver miners.

Rest assured, we are monitoring the Iran situation carefully and will keep readers informed with timely updates.