The Secret to Finding Great Mining Investments

Today’s mining sector presents a significant gap that could create wealth for many. The key lies in understanding the underlying math and assumptions.

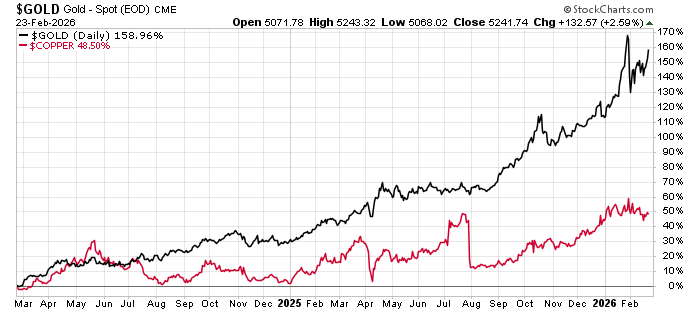

At the moment, many look at this chart and think, “I missed it.”

In reality, nothing has been missed yet. It’s crucial to remember how the commodities these companies produce—specifically gold and copper—have performed:

As illustrated, copper, gold, and various other metals have reached record price levels. Miners function as “price takers,” meaning they produce metals but don’t control their selling price. With soaring metal prices, these companies are generating substantial profits, though their valuations don’t yet reflect that.

This discrepancy is where the investment opportunity lies. Numerous projects are nearing production stages. I discussed the less promising ones in my recent essay.

But how can we distinguish good projects from poor ones?

To address this, we must understand which metal prices to apply when assessing current projects. Historically, acquisitions take place at or just below the net asset value (NAV) for advanced-stage projects and producers.

Companies with less advanced or single assets tend to be valued slightly lower, roughly around 0.8 times NAV. The challenge is how to precisely calculate the actual NAV.

Consider the example…

Snowline Gold (SNWGF) owns the Valley Project located in Canada’s Yukon Territory—a prime mining location known for safety, legality, and good infrastructure. This lowers jurisdictional risk, meaning less worry about governmental or community interference like asset seizures or tax hikes.

The deposit itself is significant, containing 7.9 million ounces of gold at a grade of 1.2 g/t, indicating an economically viable reserve across a range of gold price scenarios. The mining approach is straightforward, using traditional truck-and-shovel methods. Construction will cost about C$1.7 billion, which is reasonable.

However, the crucial factor for investors is determining its current worth, which requires understanding its NAV.

Snowline’s Valley project shows several NAV estimates depending on the gold price assumptions involved. Here are current NAV figures based on differing gold prices:

- C$2.8 billion at $2,250 per ounce gold (2025, CIBC bank)

- C$5.5 billion at $3,200 per ounce gold (2025, CIBC bank)

- C$3.4 billion at $2,150 per ounce gold (2026, company)

- C$10.7 billion at $4,300 per ounce gold (2026, company)

At present, Snowline’s market capitalization stands around C$3.0 billion, which means it trades near its NAV if gold prices remain below $2,500 per ounce. Compared to a $4,300 per ounce scenario, the stock is valued at under 0.3 times NAV.

Which valuation is accurate?

Buying the stock around 1x NAV likely won’t yield significant gains. But acquiring it at 0.3x NAV could lead to the investment doubling or even tripling.

Therefore, reconsidering the gold price becomes essential.

Throughout the past 30 years, gold prices have experienced three significant declines:

- From 1988 to 2001, the price dropped 45%.

- Between 2008 and 2009, it fell 25%.

- From 2011 to 2016, it decreased by 43%.

This indicates a chance for price drops, but the overall trend remains upward, and the future gold price remains uncertain. Factoring in a potential 45% decrease from current levels would put gold at approximately $2,880 per ounce.

Under that assumption, Snowline’s NAV would approximate C$4.0 billion. Thus, its current share price is under 1x the asset value, even if gold declines that steeply.

That seems like a remarkable bargain. Many other mining projects—covering gold, silver, copper, nickel, and more—are situated similarly.

The crucial step in valuing these opportunities is to begin with projects that have solid fundamentals. From there, investors can assess their worth and decide how to invest accordingly.