Miners Come Roaring Back

In the iconic film Groundhog Day, Bill Murray finds himself stuck reliving the same day repeatedly.

Lately, the news cycle has felt strikingly similar.

President Trump announces a diplomatic breakthrough with Iran. Oil prices plummet, stocks surge, and Treasury yields decline. We’re saved!

Gold, silver, and mining stocks often climb on these so-called “we’re saved” days as well.

Today proved no exception. Gold jumped $130 to $4,705/oz, while silver increased by $4.25 to $77.87/oz.

Mining stocks outperformed, with the GDX gold miner ETF soaring 7.69%, and the SILJ silver miner ETF climbing 8.9%.

Gold Miner Profits are Soaring

Newmont (NEM), the largest gold mining company globally, released its Q1 2026 results in late April (full disclosure: I own the stock). The figures are impressive.

They generated an outstanding $3.1 billion in free cash flow this quarter. From that, $2.7 billion was paid back to shareholders via buybacks and dividends.

Regarding oil expenses, Newmont noted that every $10 rise in the price per barrel adds roughly $12 to the all-in sustaining cost (AISC) for each ounce of production.

I anticipated a larger earnings impact from the spike in oil prices. This outcome is encouraging for the industry.

Nevertheless, elevated oil costs will continue to burden miners until tensions in the Middle East ease.

If a resolution arrives swiftly, we could see a quick resurgence of intense enthusiasm for miners. Should oil prices fall back into the $70s (or below), it would create an excellent investment environment once again.

Silver + Silver Miners Looking Good, Too

Hecla Mining Company (HL), primarily a silver producer but also generating a sizeable gold output, reported its earnings yesterday.

Hecla’s revenue in Q1 2026 hit $411 million, doubling from Q1 2025 and rising 13% compared to the prior quarter.

Other silver miners are delivering strong first-quarter results as well. This aligns with a robust Q1 for silver, which briefly exceeded $100/oz, though overall prices were not dramatically higher than current levels.

The future performance of silver miners will mainly hinge on silver’s price, with oil costs playing a smaller role.

I remain bullish on silver as a long-term investment. While short-term price moves are uncertain, I expect its value to rise considerably over the coming years due to expanding industrial demand and renewed investor interest, especially in China and India.

Gold or Silver?

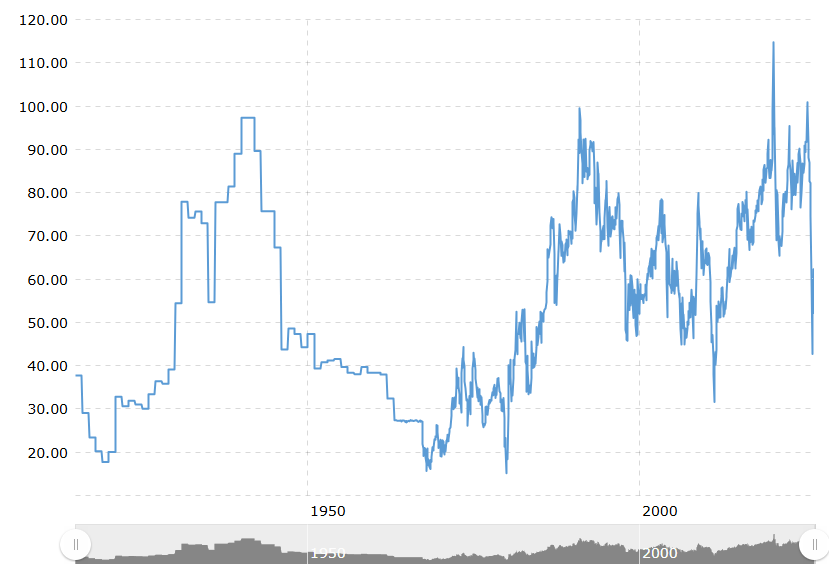

The gold-to-silver ratio is still unusually high, showing that gold remains significantly pricier relative to silver. Currently, it stands at 61, indicating gold costs 61 times more than silver.

Here is a century-long chart tracking the gold-to-silver ratio.

Source: Macrotrends

At some point in this cycle, I fully expect the ratio to dip to at least 30. With current gold prices, that would translate to silver at approximately $157/oz.

During prior bull markets in precious metals, the ratio fell to as low as 15. Historically, a range between 10 and 15 was typical until the 20th century, offering an even stronger silver target. But no need to rush ahead.

Overall, I find silver offers a more appealing risk/reward profile than gold, though it will experience greater price swings.

The key driver behind rising precious metals remains unchanged: the expanding debt bubble. We are merely observing the volatile ups and downs characteristic of manic markets.

I’m holding onto my precious metals because I recognize that further turmoil lies ahead. Eventually, this will allow me to convert these holdings into more conventional assets with much better exchange rates.

In short, the moment to do so has not yet arrived.