The Perfect Oil Chaos Stock

Everyone is striving to successfully navigate this turbulent market.

And the challenges are unlikely to ease anytime soon.

While many hope for a swift end to the Iran conflict, it’s probable the fighting will continue for some time.

Even if a ceasefire occurs, chances are the hostilities will resume after both sides regroup and rearm. Remember, Israel and Iran were engaged in conflict as recently as last summer.

As investors, we must adapt to the circumstances we’re given. With this in mind, many are looking to increase their holdings in oil stocks.

However, the specific oil stocks you choose to own are critically important right now.

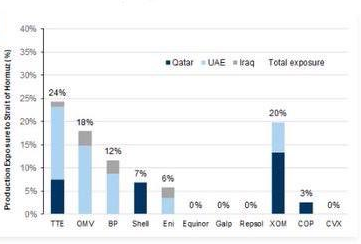

A key issue is that most major oil companies transport crude oil through the Strait of Hormuz, currently blocked by Iran. At present, only Iranian and Chinese vessels are passing through.

The chart below from Goldman Sachs illustrates the share of oil majors’ output routed via the Strait of Hormuz.

Source: Goldman Sachs

This chart isn’t the clearest, so here’s a concise summary of the key data.

Portion of oil production passing through the Strait of Hormuz:

- Exxon: 20%

- BP: 12%

- Shell: 7%

- COP: 3%

Exxon (XOM) has been one of my preferred ways to invest in oil, but this situation raises concerns. A fifth of its production is currently trapped. Storage capacity is likely approaching its limit, causing potential shutdowns of many wells if the Strait remains closed.

Although Exxon is well-diversified and benefits from rising prices, much of that gain is undermined by the Hormuz blockade. While the Middle East conflict will resolve eventually, it might take some time.

Investors currently favor oil companies without exposure to this unstable region. As covered by the Houston Chronicle:

Prices for crude and gasoline at the pump have skyrocketed, but the high price of oil isn’t necessarily enough to counteract the impacts to some of Houston’s global oil majors with operations in the Middle East and in parts of Africa affected by the conflict.

Stock prices for the majors have not benefited nearly as much as those for oil and gas giants who focus almost entirely on American production, such as Diamondback Energy and Devon Energy. Both companies have seen lucrative spikes in share price in the wake of the conflict.

Therefore, firms without Middle Eastern involvement are outperforming those that do. Diamondback and Devon appear promising, though I have yet to research them thoroughly.

That said, one oil stock we’ve talked about at length is currently experiencing strong gains.

Back to Brazil and Petrobras!

Longtime readers know I’ve been optimistic on Brazilian oil powerhouse Petrobras (tickers: PBR and PBR.A) since last May. We’ve featured it six times since then.

When we initially covered Petrobras, shares traded at $12.07. For the first eight months, the price remained fairly stable, which suited me as I reinvested dividends and waited patiently.

But since January, the stock climbed to $18.81. Even after such a gain, the price-to-earnings ratio remains around 8 (based on ~$60 oil prices), indicating it’s still extremely inexpensive.

Provided oil remains at current levels, the dividend yield is expected to surpass 10% moving forward.

Operationally, the company is delivering solid results. Oil and gas output rose 11% in 2025, a notable accomplishment for a $112 billion firm.

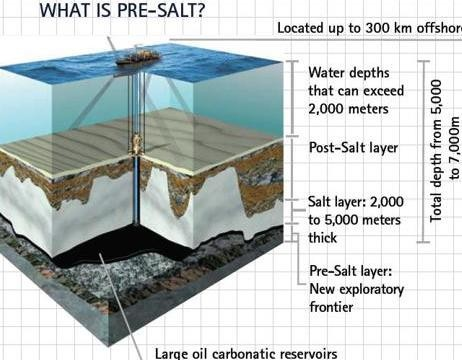

Petrobras’s competitive edge comes from its advanced exploration and drilling techniques. The company focuses on “pre-salt” offshore oil fields. Here’s a schematic:

Source: Petrobras

Brazil’s pre-salt reserves are estimated at roughly 100 billion barrels, with further discoveries likely. Petrobras will develop the vast bulk of these deposits.

Pre-salt oil lies deep beneath the ocean floor and is difficult to extract. It took decades to refine the technology now used. Yet, this oil is among the purest available and extremely abundant. A single FPSO (Floating Production Storage and Offloading vessel) like the one shown can produce as much as 250,000 barrels daily.

On average, Petrobras’s cost to produce a barrel is about $35, while current prices hover near $87. That represents an excellent business model.

Moreover, the company recently reported Q4 earnings that surpassed expectations significantly.

No Middle East Exposure

Since Petrobras operates almost exclusively within Brazil, it remains shielded from Middle Eastern instability.

Production currently averages about 3.11 million barrels of oil-equivalent daily.

The company runs 11 refineries and produces a broad array of petroleum products, including diesel, gasoline, natural gas, lubricants, chemical feedstocks, and solvents.

With many refineries in the Middle East offline, demand for Petrobras’s products should rise sharply.

Even if oil prices drop to $65 per barrel (which I don’t anticipate), Petrobras would still generate strong cash flow and pay generous dividends.

This remains, by far, my preferred oil investment in these volatile times. It offers low valuation, high yields, steady growth, vast reserves, and a positive price trend.

What more could an oil investor desire? I increased my position just this week.

One last point: Petrobras shares come in two classes—PBR (common) and PBR.A (preferred). Both represent equal ownership stakes and receive identical dividends. While PBR.A theoretically has dividend preference, this hasn’t been evident in practice.

PBR.A typically trades at a slightly lower price, resulting in a higher dividend yield. I hold that class, though the difference is minimal.

As with any stock, there are risks. While shares have risen sharply, continued elevated oil prices suggest significant further upside. In this chaotic environment, it’s among the best options available.