Nat Gas Wars: Winners, Losers, and Fallout

The conflict in Iran stands as the most significant global issue at present, comparable to an economic nuclear conflict. While many—including myself—watch oil prices climb steadily, there will inevitably be serious consequences.

Among the most critical is the impact on nitrogen fertilizer.

Nitrogen fertilizer, mainly in the form of urea, plays an essential role in current farming practices. Adequate nitrogen boosts grain yields by 50% to 100%, surpassing the effect of any other single nutrient. Fortunately, urea is generally abundant, affordable, easy to transport, and simple to apply.

Nevertheless, the key constraint lies in the raw material used to produce urea—natural gas.

Natural gas accounts for about 90% of the production cost of nitrogen fertilizer, so fluctuations in its price heavily influence fertilizer expenses.

During the preceding surge in natural gas prices, urea costs skyrocketed from $200 per metric ton in 2020 to $1,050 per metric ton by April 2022. This spike was driven by a scarcity of natural gas due to Russia’s invasion of Ukraine.

This crisis shut down 70% of Europe’s urea manufacturing capacity…

As I wrote here, Iran targeted Qatar’s massive Ras Laffan natural gas complex, which houses the world’s largest urea facility. This site produces six million metric tons annually, roughly 12% of global supply. Saudi Arabia produces about 17.2 million metric tons yearly, and Iran around nine million metric tons.

Combined, these three nations contribute nearly half of the world’s annual urea output. Currently, all three are offline. Since the conflict began, urea prices have jumped 25–35%, with further increases expected.

Natural gas prices in the U.S. have risen modestly, up 14% since late February 2026, but European prices are surging. Dutch natural gas costs soared 65% after the Strait of Hormuz closure disrupted QatarEnergy’s gas shipments.

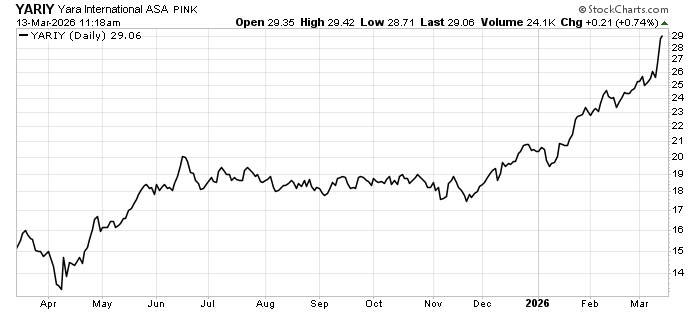

In 2022, companies such as BASF and Yara suffered due to their reliance on natural gas for fertilizer and other products:

The data reveal BASF’s share price plunged over 50%, while Yara’s dropped 40% during that period. This pattern differs now, as the market views Yara as resilient amid the current turmoil:

BASF’s stock has held steadier but has not experienced significant declines. This stability owes in part to uninterrupted production by the Middle Eastern producers in 2022, which had kept fertilizer prices relatively low. Today, however, fertilizer costs are climbing rapidly, helping to cushion natural gas expenses.

Still, natural gas prices may climb to levels where Yara is unable to profitably manufacture urea. This occurred in 2022 and might happen again in 2026, potentially causing Yara’s stock to sharply decline.

Meanwhile, one major beneficiary from 2022 has resurfaced amid the current crisis. U.S. nitrogen fertilizer producer CF Industries (NYSE: CF) experienced a 180% surge from August 2021 through early 2022:

Investors have once again shown enthusiasm in 2026:

This investment could continue advancing as the full consequences on urea prices have yet to materialize. Nonetheless, as I advised in my previous article, purchasing natural gas ETFs might be a smarter strategy:

There are several simple ways to speculate on natural gas prices. The U.S. Natural Gas Fund (NYSE: UNG) tracks the price of natural gas through futures. For those who want a little juice in the trade, there’s the ProShares Ultra Bloomberg Natural Gas Fund (NYSE: BOIL). BOIL provides a 2x leveraged return on natural gas futures prices.

These speculative options remain the most effective means to capitalize on increasing natural gas costs. Make no mistake—the price of natural gas will rise further this year.

This increase means higher heating bills for many households. Additionally, the shortage of nitrogen fertilizer will drive significant hikes in food prices.