American Oil Won’t Save the Day

Recently, a good friend who teaches asked this on Facebook:

An honest question- PLEASE don’t turn it into politics- Do we not have our own oil in this country? Why do we not drill more and supply more? If we have it and can drill, why are we not? Prices would drop, no?

I gave a brief response, but this question keeps coming up frequently. The straightforward, economic explanation is that markets regulate themselves, and oil’s value is too significant to stay low for long. Before diving deeper, there’s a term some of us need to become familiar with:

Economists describe oil as fungible, which means a barrel of oil in Abilene is identical in value to one in Singapore. Therefore, if oil costs more in Singapore than in Abilene (factoring in transportation), buyers should opt for the cheaper Texas barrel.

However, the explanation goes beyond that…

Prepare yourself for a thorough exploration. I’m passionate about oil. In the early 2000s, I considered pursuing a career in this field and even partnered with wildcatters working on wells in West Texas. It’s a fascinating topic, and I hope to convey some of that enthusiasm here!

First, it’s important to acknowledge that oil operates on a global stage. Barrels can be exchanged nearly anywhere in the world. Though there are additional complexities, the general rule is that substitutions in crude are made at price points that optimize cost-saving.

This process equalizes oil prices, preventing scenarios where one location experiences extremely low prices while another faces exorbitant costs. The market, in essence, functions smoothly…

Because of my deep interest, I want to dig deeper into the subject, starting with chemistry.

Oil isn’t uniform like a pure metal composed of identical atoms; instead, it resembles a complex mixture. It consists of chains of “hydrocarbons,” molecules formed by hydrogen and carbon atoms linked in varying lengths, with other elements mixed in. Crude with high sulfur content is termed sour; with low sulfur, it’s sweet.

We encounter both kinds regularly. Gasoline is another mixture of chains, typically containing between 4 to 12 carbon atoms. Its average formula is C8H18—chains of eight carbons connected with eighteen hydrogens.

Asphalt, used on roads, consists of hydrocarbons with chains longer than 42 carbon atoms. Longer chains make oil heavier and thicker, but both gasoline and asphalt are comprised of hydrocarbons. Some chains from sources like Canadian oil sands are so extended that heating is required to make them flow.

The average hydrocarbon chain length in oil is gauged by “API Gravity,” which measures density. A higher API Gravity indicates lighter oil.

Water’s API Gravity is 10. Oil with a gravity less than that sinks beneath water.

Generally, lighter crude contains a bigger share of shorter hydrocarbon chains, making it easier to refine into fuels for vehicles and commanding a premium compared to heavier, sour crude.

Because oil characteristics vary by location, the world uses “benchmark” prices. When a new well is drilled, its oil is compared against these standards. In the U.S., West Texas Intermediate serves as the benchmark.

Crude extracted in the United States is evaluated against WTI, setting the domestic price.

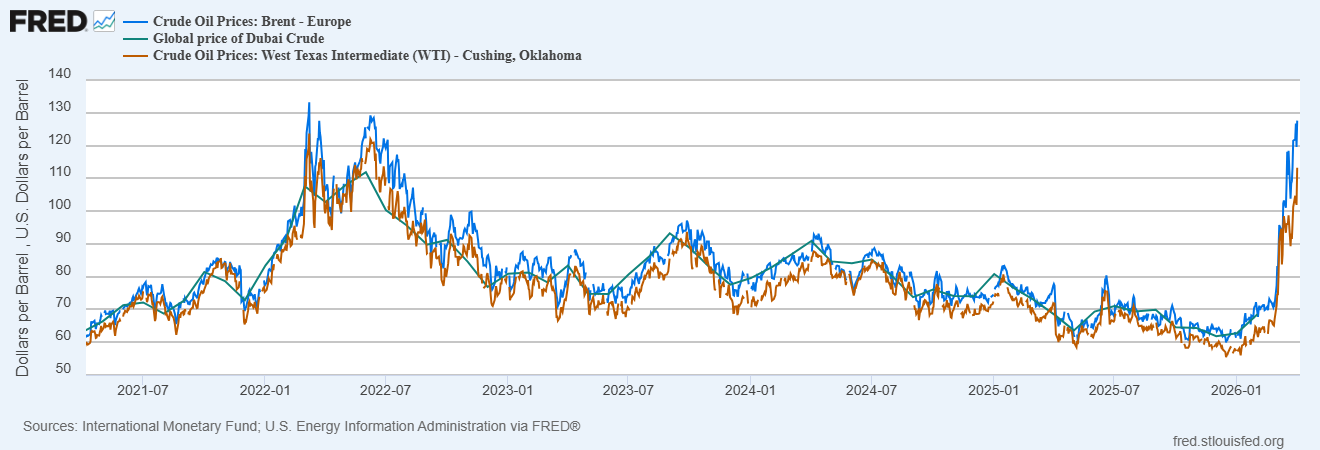

Here are the key global oil benchmarks along with their current prices:

Typically, these benchmark prices move in close sync, as shown by the price trends of three major crudes below:

The quality differences might cause slight premiums or discounts, but overall, these markets align.

For instance, when the Strait of Hormuz was blocked due to conflict, oil prices surged simultaneously from Dubai to the UK and all the way to Cushing, Oklahoma, illustrating that ownership doesn’t affect the global pricing mechanism.

Oil is central to the global economy, with markets interconnected worldwide.

Before recent geopolitical shifts, the world produced and refined about 103 million barrels a day. That means even if one nation increases output, it won’t significantly influence prices locally or internationally.