Sounding the Alarm on American Debt

The Strait of Hormuz remains open, though perhaps only partially or in a limited way for the moment.

Meanwhile, oil prices are plunging. U.S. stock markets have climbed for the twelfth consecutive day. Precious metals like gold, silver, and mining stocks are surging.

Clarity on the resolution timeline of the conflict with Iran remains elusive.

Today, we’re shifting focus to explore the consequences of the impending U.S. debt crisis.

Amidst the Middle East tensions, an article from Bloomberg yesterday largely escaped attention.

Source: X

The piece features an unsettling interview with Hank Paulson, the Treasury Secretary known for steering the $700 billion TARP bank bailouts during the Global Financial Crisis.

Paulson’s intervention safeguarded major banks using taxpayer money, including Goldman Sachs, the firm where he had been CEO. Though these bailouts occurred nearly 20 years ago, they still provoke strong emotions.

In this latest interview, Paulson cautions that the U.S. must devise a “back-up plan in order to avert a potential collapse in demand for Treasuries.”

“When you hit the wall and you’re trying to issue Treasuries and the Fed is the only buyer and the prices of the Treasuries are going down and interest rates are up, that’s a dangerous thing.”

Put simply, investors may soon require higher returns from U.S. Treasury bonds, notes, and bills.

This scenario would be catastrophic because a surge in Treasury yields would cause our debt issues to escalate rapidly.

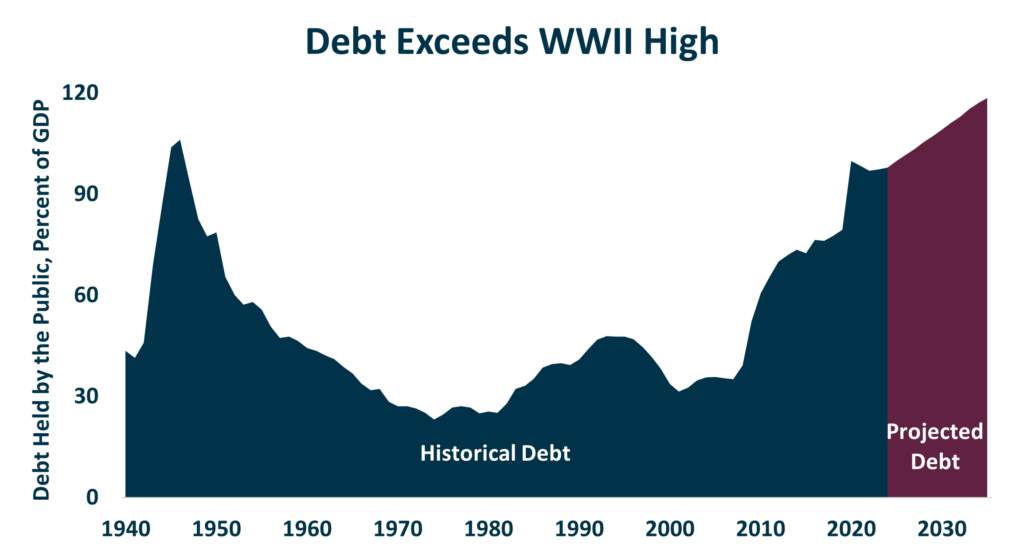

For perspective, out of America’s $39 trillion federal debt, about $9.3 trillion needs refinancing this year. Most of the current debt is in short-term instruments (long-term, 30-year bonds have lost appeal).

The yield on a 3-month Treasury currently stands at 3.68%. Should it climb to 5% or beyond, the debt situation could spiral out of control. Annual interest payments now exceed $1 trillion. If yields rise sharply, interest costs might balloon to $2 trillion, then $3 trillion—an untenable path.

It carries weight that someone as influential as Hank Paulson is raising the alarm. This underscores the urgency; the problem is not decades away but immediate.

1940s Solutions?

The last time the U.S. carried this level of debt relative to GDP was during World War II.

Source: Economic Policy Innovation Center

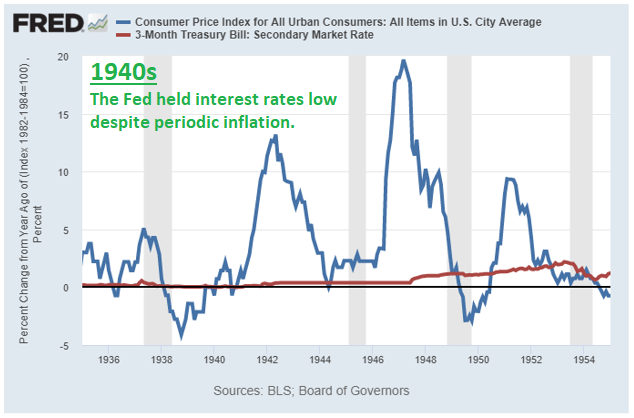

Back then, the Federal Reserve and Treasury tackled the soaring debt using “yield curve control.”

Essentially, the Fed pledged to purchase enough Treasuries to maintain extremely low yields. Paulson’s remark about a future where “the Fed is the only buyer” of Treasuries is strikingly reminiscent of this approach.

The following chart tells the story of the 1940s, with inflation shown in blue and yields on 3-month Treasuries in red.

This visual highlights how holders of cash and bonds suffered. This “financial repression” meant that despite inflation nearing 20%, Treasury bills yielded less than 1%, eroding purchasing power by about 19% annually.

At that time, Americans couldn’t invest in gold—owning bullion was illegal, and its price was fixed at $35 per ounce.

Today, citizens can purchase precious metals freely, which will be crucial for safeguarding wealth moving forward.

Assets like commodities, tangible goods, industrials, and defense sectors proved effective in the 1940s.

I anticipate a return to yield curve control in the future, though likely not for several years. When it happens, holding select foreign equities and natural resources will be advantageous.

Even Higher Taxes?!

In 1939, only about 5% of Americans paid income taxes, limited mainly to the affluent.

By 1945, income tax affected 60% of the population, showing that the debt crisis wasn’t solved solely with yield curve control but also through steep tax increases.

As history teaches, governments tend to extend their reach once given opportunities.

Paulson hinted at the likelihood of more tax hikes ahead, noting, “It’s going to take increased revenues, taxes, and dealing with expenses.”

This strategy worked post-WWII because initial tax rates were low. Today, many people already face income taxes of 30-40%, along with additional capital gains, sales, and estate taxes. The tax burden is already substantial.

Nevertheless, if Democrats secure victories in the midterms and presidency by 2028, higher taxes could become a reality.

This elevates the importance of maximizing contributions to tax-advantaged accounts such as IRAs, 401(k)s, and college savings plans.

After securing tax shelters, ensure some diversification into hard assets, precious metals, and emerging market investments. These will be vital for preserving and growing wealth during disruptive times ahead.

Additionally, I recommend reducing long-term holdings in U.S. Treasuries. Holding some over the next year or two can be beneficial—especially if rates decline, increasing bond values. But in the long term, these won’t be a cornerstone of a sound retirement portfolio.

Inflation will erode purchasing power as yields stay artificially suppressed, striking U.S. Treasuries hardest in the upcoming period of financial repression.

We will soon explore alternative options to U.S. Treasuries for retirement planning.