Avoid “Lifestyle Creep” at All Costs

Affordability had already been deteriorating well before the recent surge in energy prices. This is part of a deeper, long-term structural shift.

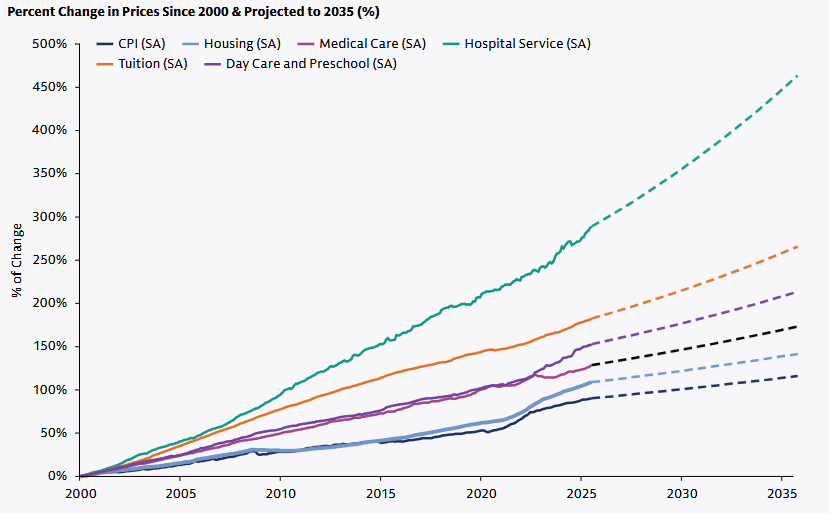

The following chart, provided by Goldman Sachs, illustrates the rise in costs across the U.S. since 2000, with dotted lines indicating projections through 2035.

Source: Goldman Sachs

Over a span of 26 years, hospital service costs have soared by almost 300%. Tuition fees have climbed over 165%, and daycare expenses have increased by 150%. These figures come from government data, which typically understate the actual inflation experienced.

While there are some ups and downs, the overall trend points sharply upward.

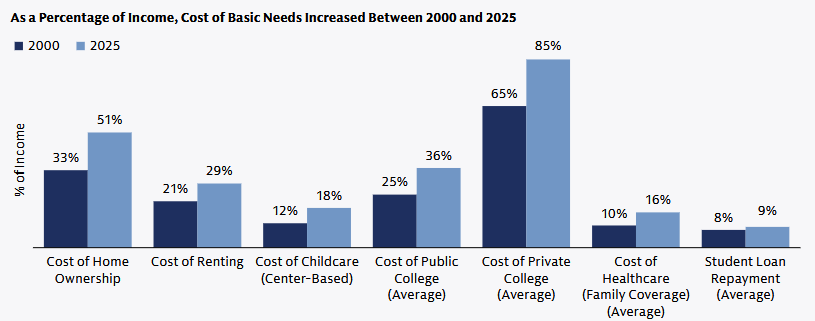

These expenditures are consuming an ever-larger share of household incomes.

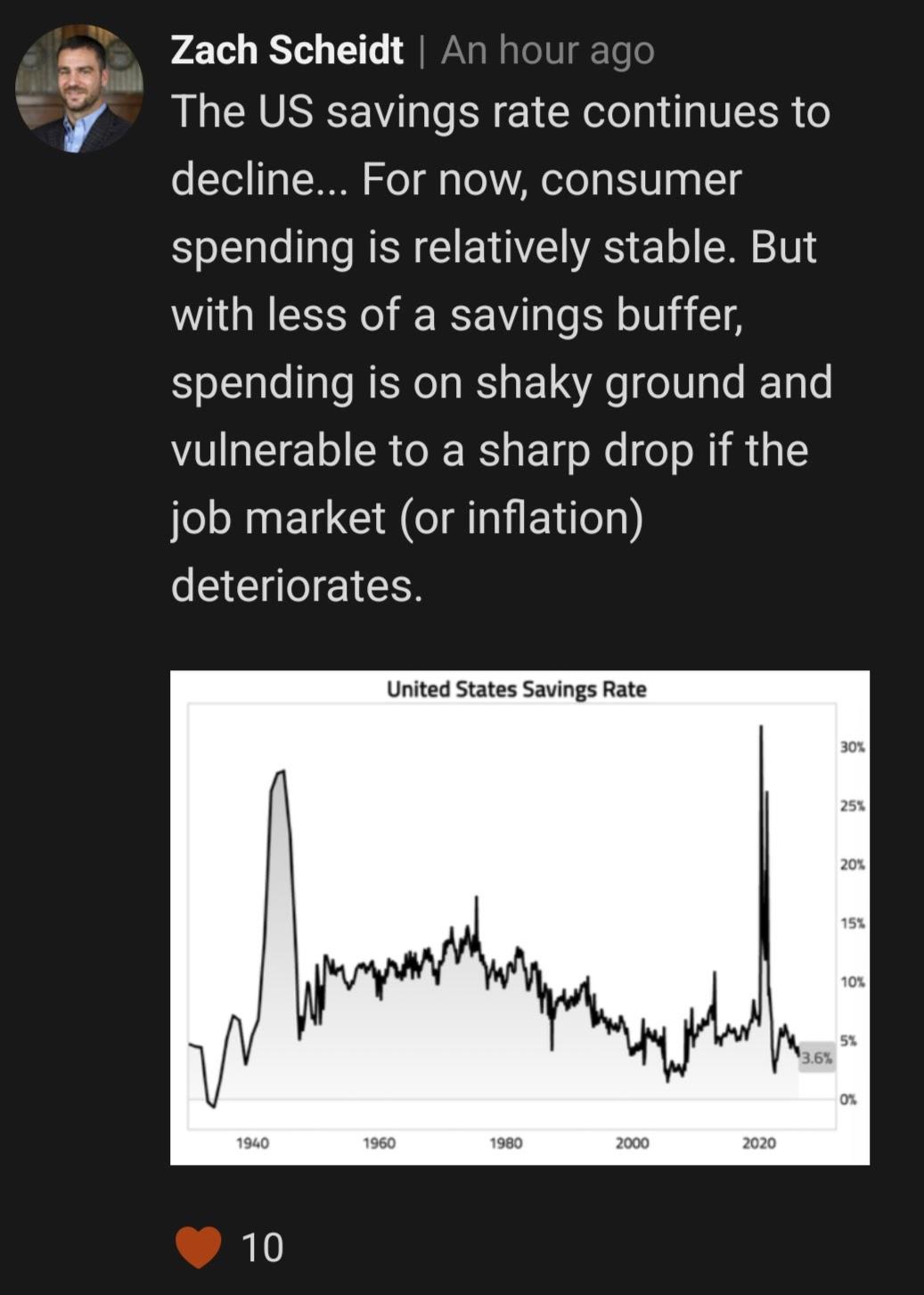

The impact is widespread among Americans. As highlighted by our colleague Zach Scheidt in the app’s Daily Feed, the national savings rate recently dropped to just 3.6%.

Download the free Paradigm Press app here.

Savings are dwindling while an increasing number of individuals find themselves living paycheck to paycheck.

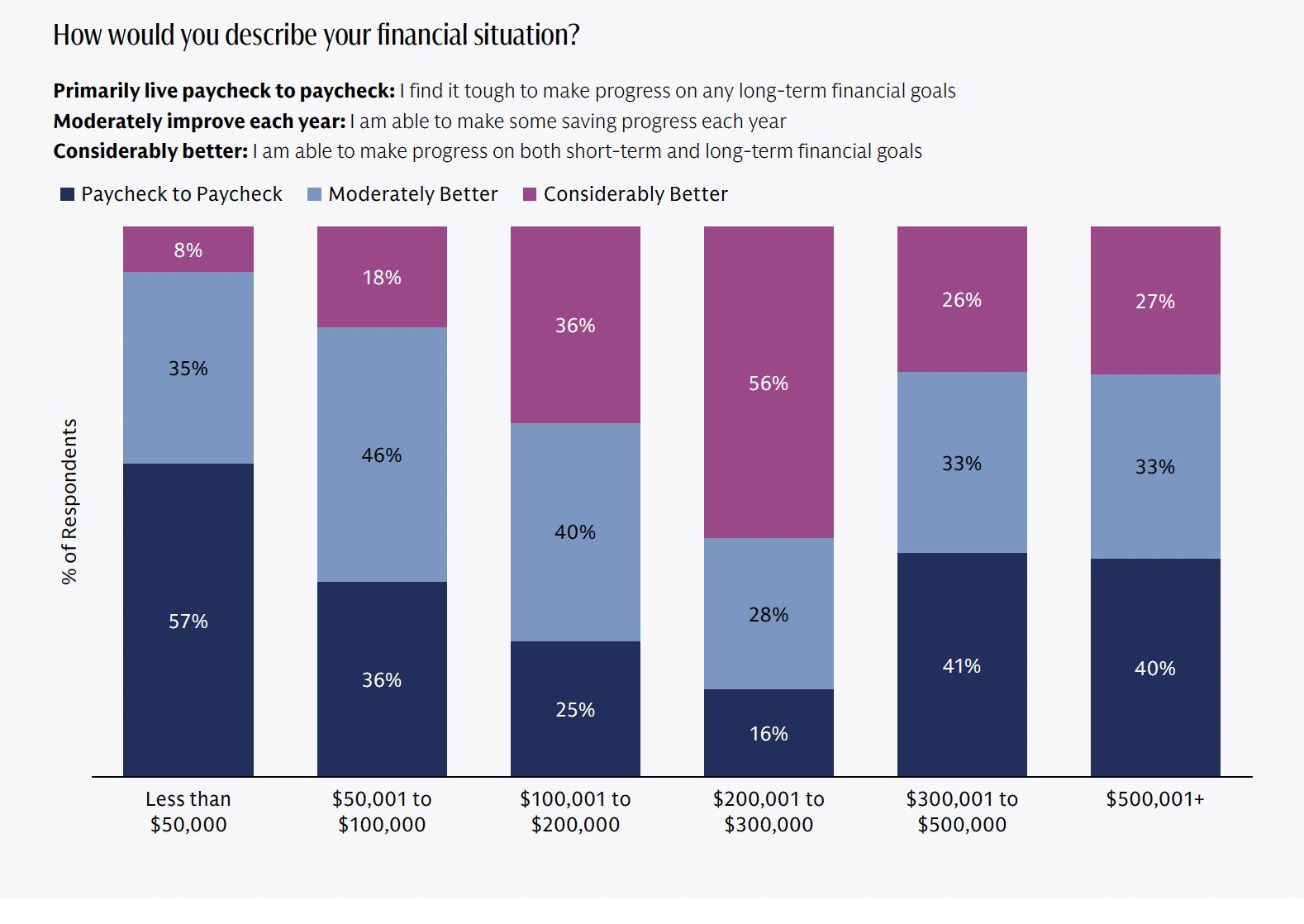

A particularly startling insight from the Goldman Sachs report reveals that 41% of households earning above $300,000 annually identify as “paycheck to paycheck”.

Source: Goldman Sachs

Equally surprising is that 40% of those with incomes over $500,000 report living paycheck to paycheck.

Of course, much of this stems from inflationary pressures beyond our influence. However, for those earning $300,000 or $500,000 or more annually without saving, that situation is far from ideal.

Lifestyle Creep

This trend is referred to as “lifestyle creep”: as earnings rise, spending increases as well.

Many use raises or bonuses to finance costly vacations, optional home improvements, or new vehicles instead of channeling that money into investments.

This behavior is common to most people to varying degrees. But if you’re engaging with this newsletter, it suggests a commitment to becoming a more savvy investor.

In today’s expensive environment, smarter investing often means reducing expenditures.

Consider driving your vehicle until it no longer runs, cutting the cable subscription for a more affordable streaming service, moving funds from a large bank that yields 0.03% to one offering higher returns, holding onto older appliances and fixtures, and opting to prepare excellent meals at home instead of dining out.

A key part of this is avoiding status-driven spending habits. Embracing frugality and living below your means ought to be seen as a powerful advantage. That’s the foundation.

And then comes the investment component…

Adapt, Survive, Thrive

We recognize that saving and investing are difficult under current conditions. Costs keep climbing, and the labor market is challenging.

Retirees face difficulties finding appealing income-producing investments. The S&P 500’s dividend yield has fallen to a mere 1.1%. While stocks have performed well, dividend yields remain low at present.

Treasury securities might do well if the Federal Reserve lowers rates and resumes quantitative easing. However, over time inflation could surpass bond returns, and there’s always the risk of rate hikes causing Treasury prices to fall before the Fed intervenes.

In situations like this, diversifying into alternative investments is crucial. This explains why Paradigm has emphasized these sectors.

Investments in gold, silver, mining companies, oil, and other natural resources have significantly outperformed the S&P 500 in recent years, yet most investors held only small amounts. Those who subscribed to Jim Rickards’ services, however, benefited from this exposure.

We aim to continue guiding you toward strong, profitable opportunities during these unpredictable times. But to fully capitalize on them, some must first commit to reducing their spending.