The Next Inflation Wave is Here

April saw inflation surge sharply.

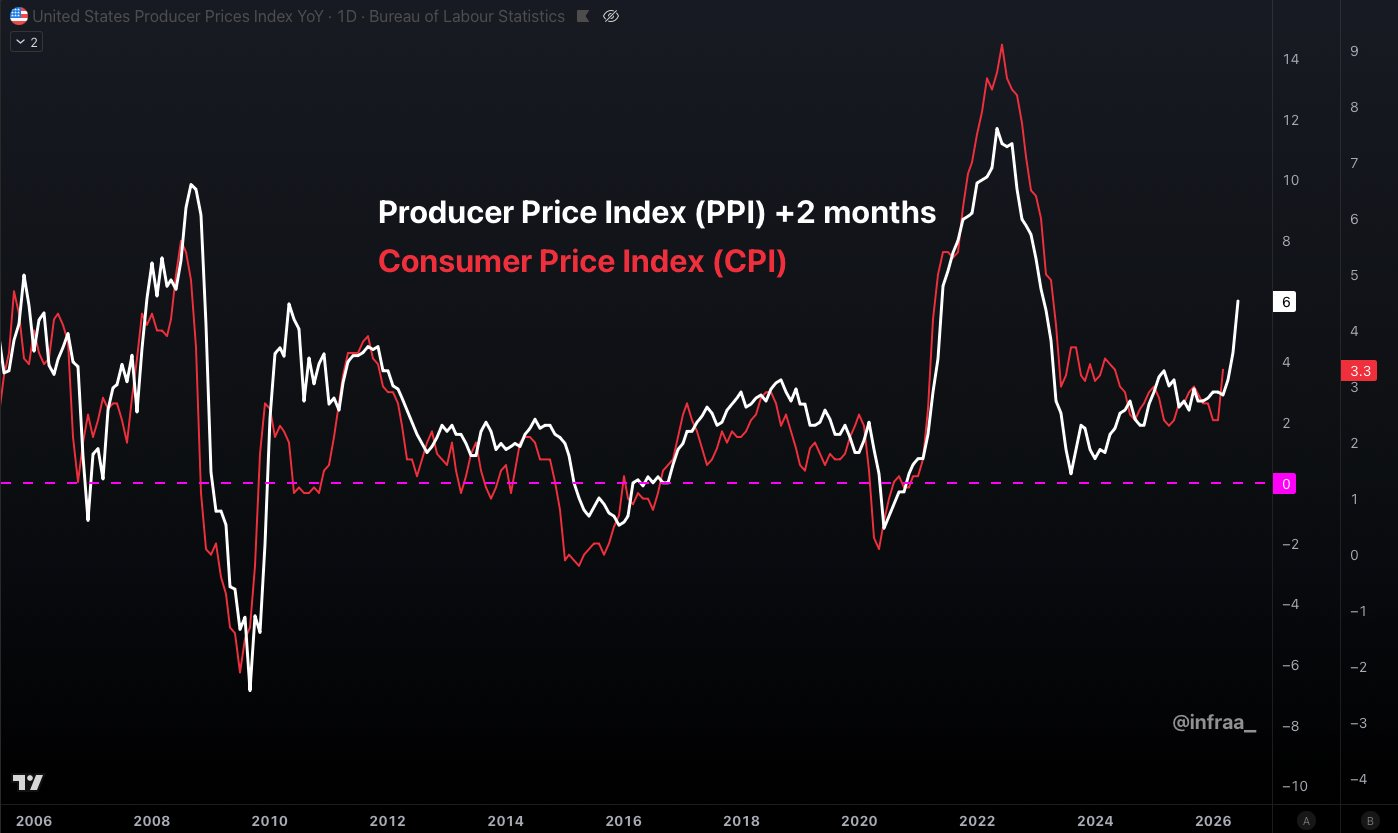

The producer price index (PPI), which reflects the costs paid by companies for wholesale goods, climbed 6% compared to last year.

Unfortunately, consumer inflation (CPI) usually follows PPI with about a two-month delay.

The chart below illustrates the close relationship between CPI and PPI, with PPI leading by roughly two months:

Source: Robert infra on X

Observe the significant spike from 2021 and 2022, driven by post-COVID inflation linked to extensive monetary stimulus. Additionally, Russia’s 2022 invasion of Ukraine aggravated the situation by causing sharp increases in oil and fertilizer prices.

Another chart compares recent inflation trends (shown in green) with those of the 1970s (displayed in blue):

It’s important to mention that inflation rates in the 1970s were higher, peaking around 12% in the mid phase and reaching 14.5% in the final surge.

Our recent “middle wave,” peaking in 2022, maxed out near 8.5% inflation.

This discrepancy is largely due to the current methodologies for calculating CPI, including tools like “hedonic adjustment” that tend to understate the true inflation rate.

In truth, the inflation path we’re on closely resembles that of the 1970s. The key difference lies in the scale of debt today.

The United States now carries a debt-to-GDP ratio near 125%, whereas during the 1970s it was roughly 35%. This means our current debt load is about 3.5 times greater relative to our economy’s size.

This significant debt burden greatly restricts the Federal Reserve’s available strategies.

In the 1970s, Paul Volcker tackled inflation by raising the fed funds rate to an extreme 20%. Such an approach is not feasible today given the debt levels.

Even facing another inflation surge, it’s unlikely the Fed will further increase interest rates since the math simply doesn’t add up.

The Fed’s Dilemma

Kevin Warsh, President Trump’s appointee, was recently confirmed by the Senate.

He is set to replace Jerome Powell, who is viewed as an inflation “hawk” due to his past rate hikes intended to curb inflation.

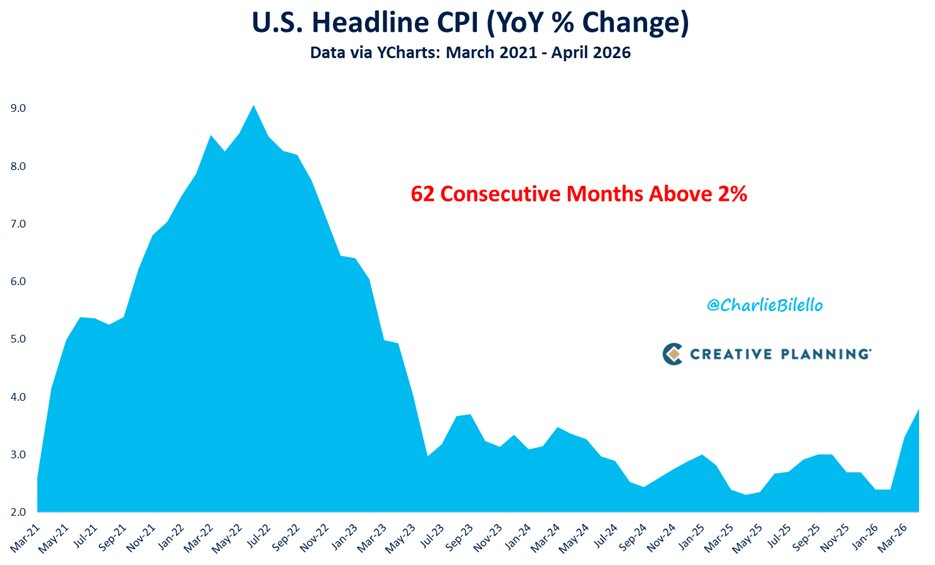

Nevertheless, the following chart reveals inflation has exceeded the Fed’s 2% target for 62 straight months.

Source: Charlie Bilello on X

President Trump has openly criticized Powell over his unwillingness to reduce rates further, and this criticism holds some merit.

Though technically the Fed “should” raise rates, doing so now would cause significant harm.

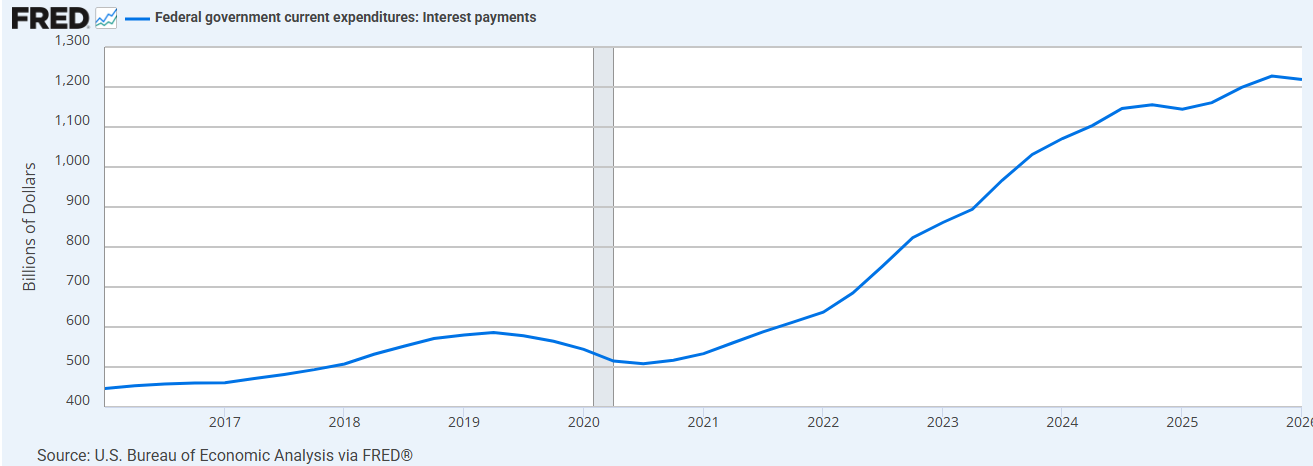

We’re at a stage in the debt cycle where just servicing the federal government’s debt costs $1.2 trillion annually. The chart below illustrates this over the past decade:

Source: St. Louis Federal Reserve

When rates were near zero in 2020, annual interest expenses were about $500 billion. Now, that figure has risen to $1.218 trillion.

In 2025, U.S. tax revenues totaled roughly $5.2 trillion, meaning nearly 23% is allocated solely to debt interest payments. This is staggering.

Increasing interest rates further would be catastrophic, as interest payments could quickly soar to $2 trillion and exacerbate the problem exponentially.

Ideally, the Federal Reserve operates independently, with a mandate to keep inflation near 2% and employment high.

However, in reality, the national debt situation demands their attention, indicating that interest rates will need to stay lower for the medium to long term.

Financial Repression

This leads us to the concept of “financial repression.” I anticipate the Fed will be compelled to lower rates even while inflation remains above target. They may also have to purchase large volumes of U.S. debt to help fund government deficits.

Eventually, “yield curve control” will likely be implemented to maintain artificially low rates, regardless of inflation pressures.

My focus on this topic stems from the approaching need for drastic actions to manage the escalating debt crisis.

As Kevin Warsh begins his tenure as Fed Chair, I expect he will follow Trump’s direction to reduce rates despite elevated inflation.

Though rate cuts may not happen immediately, lowering rates should begin this year due to the urgency of the debt situation, which will outweigh inflation concerns despite the discomfort it causes.

Starting next year, more aggressive policies like large-scale quantitative easing (QE) and eventually yield curve control are probable.

During periods of financial repression, investing in tangible assets such as natural resources becomes essential for preserving and growing wealth.

My focus is on miners with extensive projects spanning 20 to 30 years, as well as top oil producers holding billions of barrels in reserves—firms with solid assets poised to appreciate regardless of economic instability.

We will keep examining strategies to assist readers in weathering the upcoming challenges.