Our Four Fathers Were Right

Throughout much of its history, the United States viewed debt with caution, often bordering on fear. This mindset originated from four men who recognized something modern leaders seem to overlook: debt functions less as an economic instrument and more as a tool of political influence.

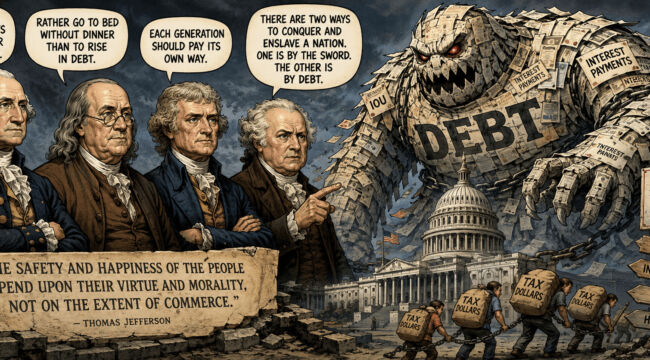

George Washington, Benjamin Franklin, Thomas Jefferson, and John Adams—America’s founding fathers, visionaries, and revolutionaries—were keen students of history. Their experience taught a clear truth: nations don’t fail suddenly. Instead, they erode gradually under the burden of obligations beyond their control.

Washington cautioned against entanglements that might drag the fledgling nation into endless commitments. Today, America finds itself deeply involved in foreign alliances and weighed down financially at home.

Franklin, ever practical, grasped how overindulgence corrodes stability. “Rather go to bed without dinner than to rise in debt,” he famously stated. Presently, the United States does neither—it spends freely and borrows recklessly… at least for the moment.

Unlike the centralized approach favored by Alexander Hamilton, Jefferson distrusted consolidated financial authority and perpetual debt, insisting that each generation should shoulder its own expenses. Today, that principle seems almost nostalgic. The existing system not only burdens future generations but also causes the debt to escalate exponentially.

Adams was even more straightforward: “There are two ways to conquer and enslave a nation. One is by the sword. The other is by debt.”

We opted for the latter.

Now, the consequences are unavoidable—not merely theoretical, but evident in cold, hard numbers.

When Interest Becomes the Budget

In the near future, interest payments on the national debt are expected to become the largest single expenditure in the federal budget—surpassing defense, Medicare, and eventually Social Security if current trends continue.

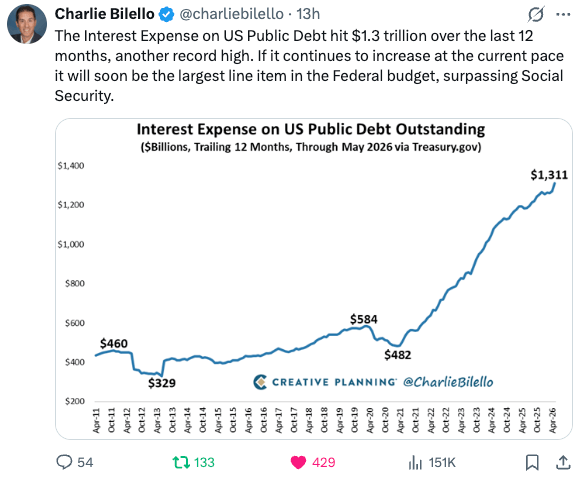

This post is truly striking:

Credit: @charliebilello

The figures are already staggering. In fiscal 2024, net interest payments totaled roughly $882 billion—almost three times the $345 billion paid in 2020—and exceeded spending on national defense or Medicare. Estimates for 2025 put that number near $970 billion, accounting for about 19 percent of all federal revenue.

Pause for a moment. Almost one-fifth of tax revenue now goes solely to servicing interest. This is before paying soldiers, social security benefits, or funding infrastructure repairs.

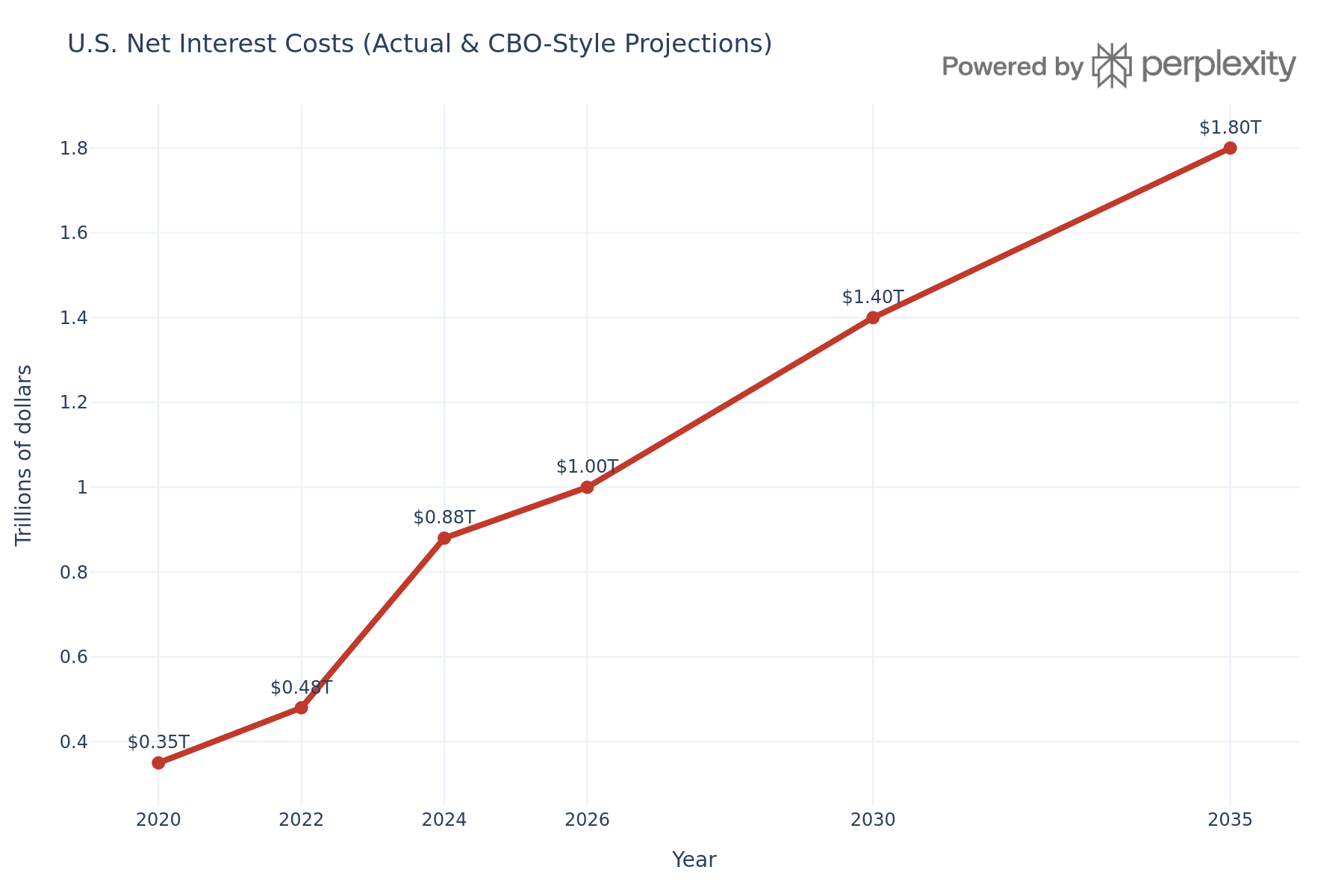

According to CBO forecasts, the annual interest burden will surpass $1 trillion around 2026 and keep climbing to approximately $1.8 trillion by 2035. Over the next decade, cumulative interest payments will reach into the tens of trillions. Across 30 years, the U.S. could spend close to $100 trillion on interest alone if present policies persist.

This represents a gradual but massive shift of national wealth from taxpayers to bondholders.

The chart above illustrates this trend clearly. Net interest expenses rise sharply from a few hundred billion in 2020 to about $1 trillion by the mid-2020s, then accelerate relentlessly toward $1.8 trillion by 2035—it’s not a gradual incline but a steep increase.

From Spending Priorities to Interest Tribute

The real concern goes beyond nominal sums—it’s the shifting makeup of the federal budget itself.

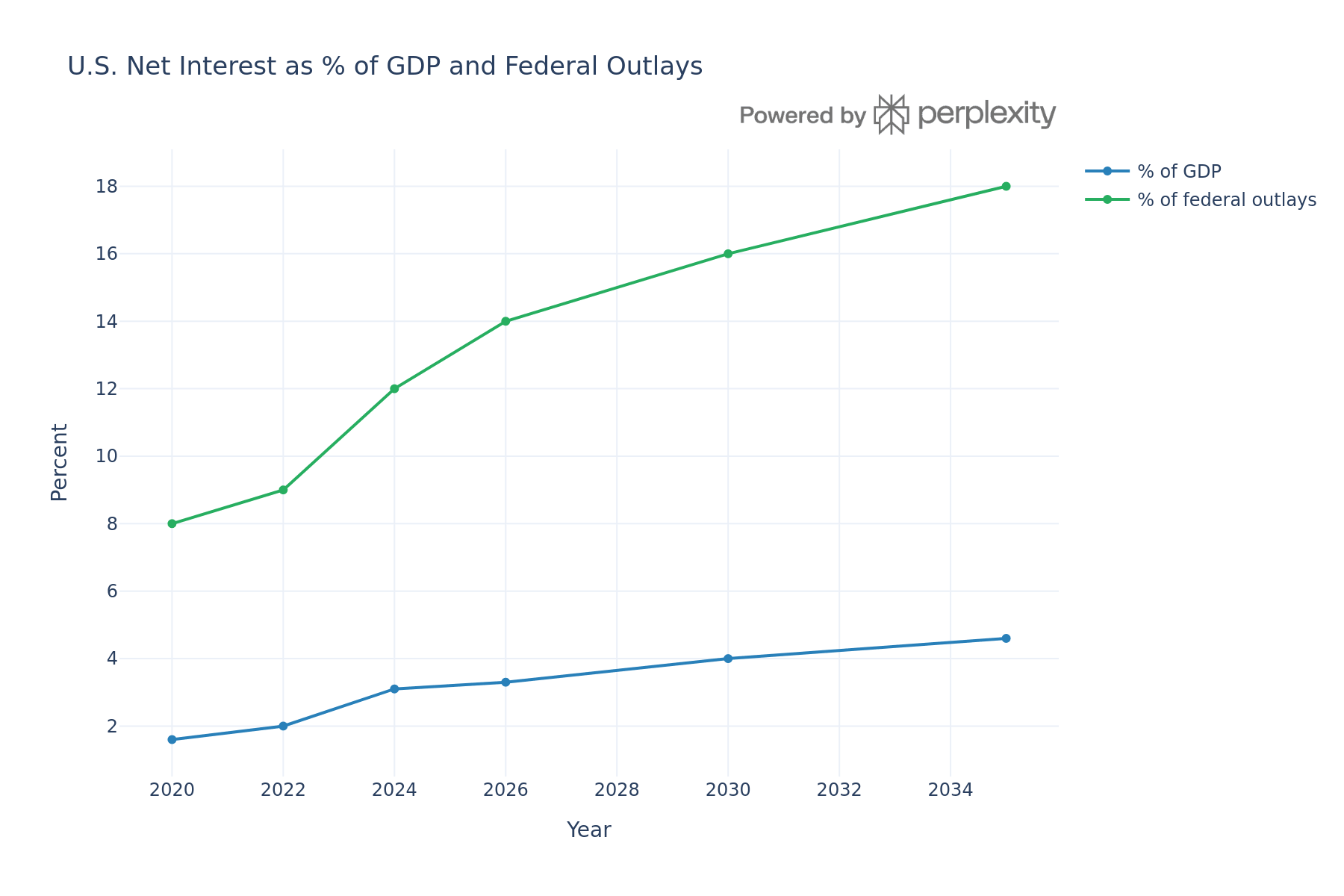

Interest payments already rank as the government’s second largest expense, second only to Social Security, outpacing every other major federal program. By the decade’s close, interest is expected to consume 15–16 percent of total federal expenditures—exceeding peaks seen in the 1990s, but on a far larger debt base and with considerably less flexibility.

Relative to the broader economy, the rise of interest costs is breaking new ground. CBO projections estimate net interest will climb from just over 3 percent of GDP in the mid-2020s to near 4.5–5 percent by the mid-2030s, and continue growing thereafter.

This graph summarizes the predicament: one curve shows net interest steadily rising as a percentage of GDP; another tracks its growth as a share of federal spending, reaching into the mid-teens.

At some stage, federal budgeting ceases to reflect national priorities. Instead, it becomes about meeting previous obligations.

That threshold would be immediately understood by the four founders.

When interest payments dominate your budget, you cease to govern freely. Instead, you manage liabilities.

Debt as Stealth Political Control

Every dollar allocated to interest is one less dollar for defense, infrastructure, or public services. It transfers wealth from the populace directly to creditors, including foreign governments and institutional investors focused solely on continued repayment.

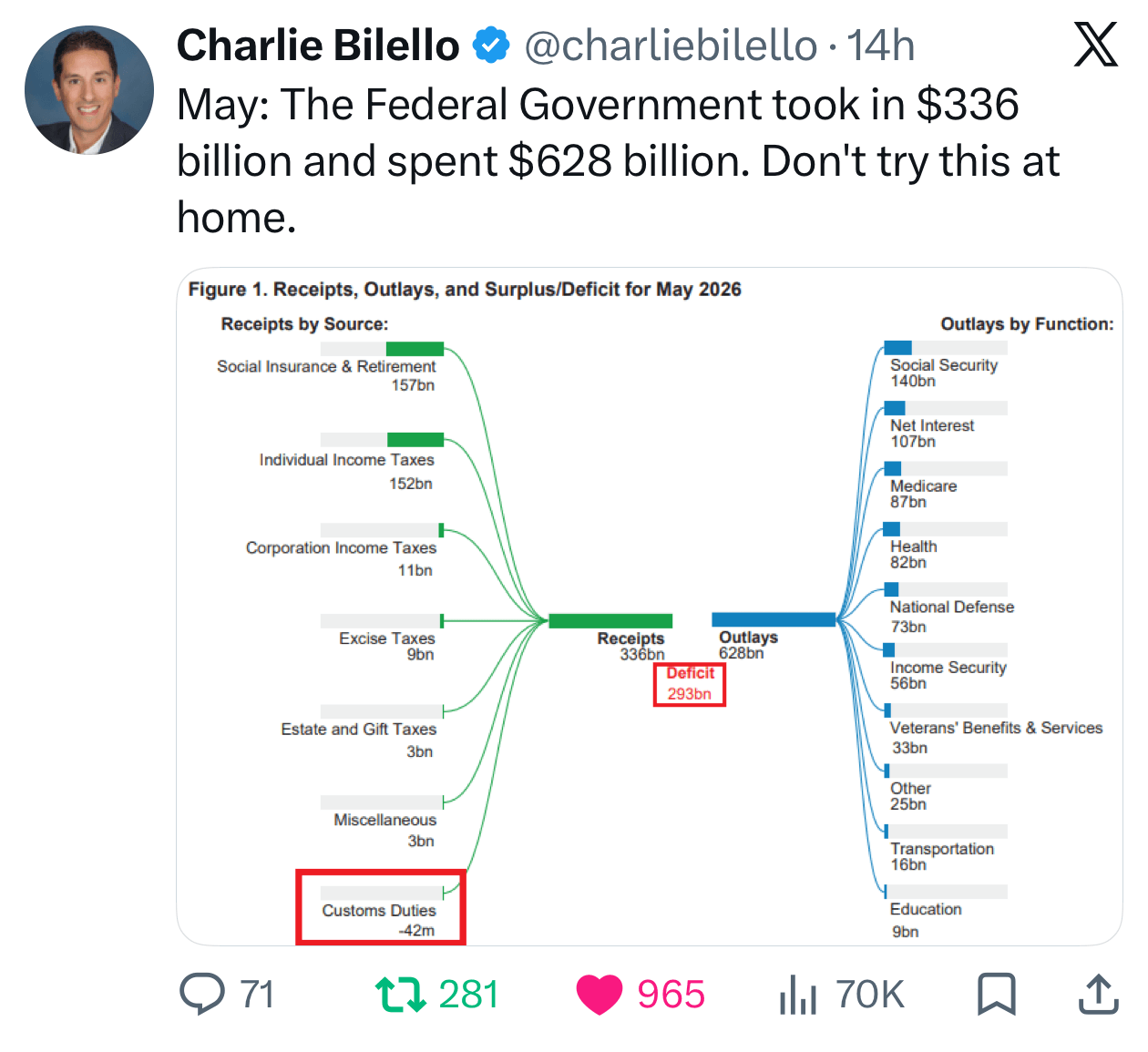

To underscore this, consider the figures from May 2026, courtesy of Charlie Bilello:

Credit: @charliebilello

You read that correctly: $107 billion went to interest payments in just the month of May 2026, second only to Social Security.

At this point, the warnings from the founders sound less like abstract philosophy and more like urgent risk assessments.

Washington feared engagements that would compromise the republic’s independence. A nation obliged to refinance trillions at rising interest rates is far from autonomous; it is subject to market constraints. Just observe The Donald’s unpredictable policies, seemingly guided by market hours.

Jefferson’s disdain for perpetual debt wasn’t naivety about growth; it was insight into how a nation perpetually in arrears mortgages its future decision-making.

Adams’s statement on conquering a nation through debt rather than force wasn’t exaggeration. It reflects how control increasingly operates—not through direct coercion, but by dominating financial flows.

This is the reality today. Despite military might and issuing the global reserve currency, the U.S. finds its fiscal fate governed by a simple equation: how to service an expanding debt burden amid rising interest rates.

When interest consumes 15–20% of your budget and a quarter of your revenues, governance serves bondholders, not the people.

What Happens When the Bill Comes Due

The markets will support this situation—until they suddenly won’t.

There is no exact moment when confidence evaporates, but the warning signs are familiar:

- Borrowing costs surge as investors demand higher premiums for fiscal instability.

- The currency declines as foreign holders question its lasting value and reliability. (Just review TLT’s poor performance since 2020.)

- Policymakers face difficult choices: raising taxes, abrupt spending reductions, financial repression, or increased inflation.

The CBO’s long-term models already assume consistently high interest rates that grow faster than both revenue and economic output. This dynamic propels the projection where interest stands as the largest slice of federal spending in under ten years.

The founding fathers would not find these outcomes surprising. They analyzed the demise of overextended empires such as Spain, France, and Britain whose expenditures outpaced revenues. Our Four Fathers recognized that excessive debt is a subtle form of national subjugation.

Regrettably, those who came after them—and the electorate—neglected their cautions.

Wrap Up

The impact is no longer theoretical; it is visible in the federal budget, where interest payments verge on eclipsing all other expenditures.

Successive generations have systematically dismantled the cultural, political, and financial protections the four founders established to prevent this fate.

Debt has become destiny. And the data signals that destiny is rapidly approaching.