The larger initiative to “Make America Great Again” cannot achieve success if Americans do not live long enough to witness its fruition.

This effort is doomed if Americans continue to suffer from illness, face overwhelming medical expenses, or worse, die prematurely before experiencing its benefits.

On the evening of November 9th, U.S. President Donald Trump shared his belief that the government shutdown might soon come to a resolution. Regardless of how this episode of partisan conflict concludes, it highlights a more pervasive and systemic issue within the nation. At first glance, the U.S. government shutdown may appear to outsiders as yet another cycle of political theater between ‘tax and spend’ liberals and ‘small government’ conservatives struggling over budget austerity. However, this overlooks the crisis’s breadth: federal employees miss paychecks, SNAP assistance is delayed, flights are canceled, and families face soaring health insurance premiums. The longest federal shutdown in American history has revolved chiefly around healthcare funding. Subsidies for the Affordable Care Act marketplaces are expiring without allocated funds, leaving millions uninsured until a solution is reached, despite the ACA remaining legally in effect. The impasse between Democrats demanding subsidy extensions and Republicans refusing negotiations until the government reopens exposes a harsher reality: the U.S. healthcare system is designed to extract wealth while limiting care.

As the U.S. attempts to rehabilitate its domestic and international reputation, the healthcare crisis fueling the shutdown reveals internal fractures. Are these challenges insurmountable? The crisis is a global embarrassment: how can the U.S. champion rule-setting abroad when its own system remains in disarray? The prevailing notion is clear: America may be a pleasant destination, but becoming ill or injured there is a dire prospect.

The Affordable Care Act primarily benefits individuals lacking affordable employer-backed insurance—such as part-time workers, the self-employed, unemployed persons, and low- to moderate-income families. Its subsidies aim to make coverage accessible to those who otherwise could not afford it. Simply put, the ACA marketplace, popularly called ‘Obama Care’, is imposing a significant 20% rise over last year’s costs on taxpayers. This represents a hefty extraction by aggressive private insurers like UnitedHealthcare, Anthem/Blue Cross Blue Shield affiliates, Cigna, Kaiser Permanente, Molina Healthcare, and Centene/Ambetter.

Money and political logic

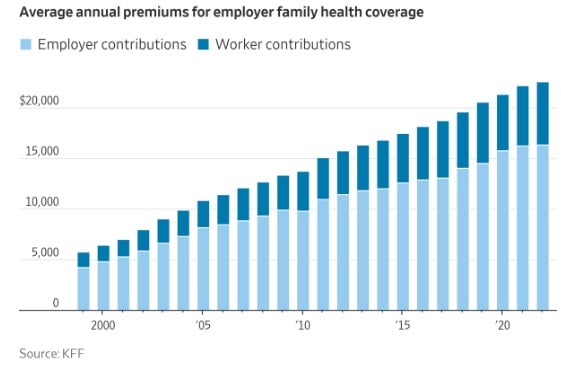

Since the ACA’s inception, average monthly premiums for a mid-level Silver plan have risen from about $900–$1,100 ($10,800–$13,200 annually) in 2010–2011 to approximately $2,200–$2,600 ($26,400–$31,200 yearly) by 2022–2024—a staggering 120–150% hike that far outstrips wage growth and inflation.

Beyond ACA plans, private insurance—whether purchased individually or employer-subsidized—anticipates a steady 9%-11% premium increase. So, for a family plan now costing $25,000 to $27,000, this translates to an extra $2,250–$2,970 per year in 2026. Approaching $30,000 annually, this reality is staggering. This forces many to reassess the true cost versus the benefit involved.

The harsh reality is that ACA premiums are escalating nearly twice as fast as comparable private plans because insurers rely on government subsidies to cover much of the expense, allowing them to push prices higher without immediate backlash. This dynamic fuels the frustration. Employers either cannot or choose not to cover many workers, and the ACA inadvertently guarantees excessive private insurance profits beyond any semblance of fair competition. At its core, America faces a problem rooted in greed.

The healthcare debate surpasses conventional partisan boundaries. It underlines a political shift developing over recent years: MAGA Republicans largely represent a working-class constituency, often rural and dependent on ACA subsidies themselves. The Democratic base, conversely, is increasingly made up of those with combined incomes exceeding $300k–$400k, benefiting from modest premium hikes around 10%. Meanwhile, Democrats also retain support from retirees, lower-income urban residents, and public sector employees who depend on a mix of ACA and unsubsidized private insurance. Thus, the traditional partisan alignment no longer applies as it once did.

The shutdown also reveals the political influence of the Health Industrial Complex (HIC). Private insurers contribute substantially more to Democrats than Republicans, a reversal from previous decades. This dynamic helps explain the repeated promises of incremental reform and the historic lack of systemic innovation. Democrats’ criticism of HMOs is constrained by donor dependencies, while Republicans’ opposition to the ACA is tempered by political realities: many conservatives acknowledge that without subsidies, premiums would become unaffordable for their constituents.

The healthcare struggle reflects fundamental disagreements about American society’s future. Most citizens regard medical coverage as a fundamental right and shared responsibility ensured by collective mechanisms. A 2020 Kaiser Family Foundation study, titled, “Democrats Like Both the Public Option and Medicare-for-all, But Overall More People Support the Public Option, Including a Significant Share of Republicans,” found that 68% of Americans favor a public option. Fewer view health coverage as a market commodity governed by individual choice and risk management. Yet this market-focused viewpoint dominates mainstream media discourse, irrespective of political leanings. This reveals that the divide is predominantly economic rather than strictly partisan. How might support increase if corporate media presented the public option fairly? And if over two-thirds already back it, why hasn’t government action followed? The powerful insurance lobby wields influence in ways that elsewhere would be considered corruption or bribery but are normalized in America.

The class conflict underlying the discussion

The 2025 federal shutdown, now nearing forty days, underscores the peculiar entanglement of government and healthcare interests—primarily serving wealthy stakeholders in America’s upper class.

U.S. healthcare functions similarly to the military industrial complex, forming what could be called a ‘Health Industrial Complex.’ Taxpayer money funds medical infrastructure, research, and drug development, yet ordinary Americans bear premiums, deductibles, copays, and surprise bills. Losses are socialized, while profits remain private, creating a darkly corporatist system that embodies the worst of both worlds. The federal government props up the HMO and insurance ecosystem, and when this support falters, the human toll is immediate and severe.

At its foundation, the healthcare conflict also reflects socio-economic class tensions in a Weberian or Marxian framework—the ‘haves’ versus the ‘have nots’—though media seldom present it this way. Americans recognize the broken status quo because excessive insurance profits depend on denying valid claims. The system disproportionately rewards executives, shareholders, and major insurers, while middle- and working-class families bear the financial burdens. This creates a situation in which the system’s funders lack control, whereas its beneficiaries hold immense political sway.

Luigi Mangione and the embodiment of collective frustration

In December 2024, the nation was stunned when Luigi Mangione, a private citizen driven by frustration with the healthcare system’s inequities, committed the murder of an insurance executive in Midtown Manhattan. Mangione’s actions resonated with many Americans by spotlighting a deep-seated helplessness. He became, albeit tragically and violently, a symbol of confrontation with a rigged system. Millions related to his anger: workers tied to jobs for benefits, self-employed families struggling with premiums, parents unable to secure prompt medical care for their children, and, crucially, individuals who see claims denied despite costly payments.

Though condemned, Mangione became emblematic of the despair generated by a system that prizes profit over well-being. A December 2024 poll, conducted shortly after Mangione’s act, Most Americans say insurance profits and denials share blame in CEO’s slaying, revealed that 70% of respondents hold insurance companies partially accountable for the murder.

Luigi Mangione’s extreme response shed light on widespread dissatisfaction with U.S. health insurers. Public surveys continually find that many view corporations like UnitedHealth Group as exploitative, secretive, and largely without accountability. In this light, Mangione’s killing of UnitedHealthcare CEO Brian Thompson has been interpreted by some not as condoning violence but as a symbolic eruption against a system that burdens families and too often sentences them to death. For observers beyond the U.S., this event reveals more about systemic pressures than the individual perpetrator.

America’s Health Industrial Complex

The Health Industrial Complex (HIC) is designed to exploit scale. Insurers hold near-monopolistic control, leveraging algorithmic price-setting and opaque provider networks to maximize profits. Consumers pay twice: once through government subsidies underwriting the system and again via out-of-pocket expenses for services that are nominally covered. Copays, deductibles, and steep premiums transform even minor medical visits—such as an ER trip for a cold or routine blood tests—into costly affairs despite insurance.

The resemblance to the military industrial complex is striking. Both systems consolidate profit and power by government-funded capital investment while passing consumption costs to the public. In healthcare, however, the stakes are deeply personal: family finances, health, and lifespan are on the line.

What if families opted out of insurance? Over a decade, they could save or invest nearly $280,000—funds sufficient for a home, business growth, or major lifestyle enhancements. Allocating just 10% of that to healthcare needs and being willing to seek treatment abroad for catastrophic events would offer an immediate, practical alternative. Instead, these resources are funneled into insurance company overhead, bureaucratic red tape, and shareholder returns. Yet, for most, only routine doctor visits and prescription medications are essential.

The Trump-Kennedy MAHA strategy

Launching in January 2026, Trump’s TrumpRx.gov aims to reduce medication costs by bypassing pharmacy intermediaries, lowering patients’ direct expenses. Trump’s 2020 executive order sought to enhance price transparency and implement international reference pricing, but the Biden administration reversed these policies, leaving patients reliant on costly insurance frameworks. Robert F. Kennedy Jr.’s concierge care initiative, unveiled in June 2025 as part of his MAHA (Make America Healthy Again) platform, bypasses the conventional HMO system. It emphasizes direct primary care, telemedicine, and preventive care. For $75 monthly, patients gain 24/7 physician access, with health savings accounts covering gym memberships and wellness activities. Workplace clinics provide basic diagnostics and preventive services, while telehealth enables early intervention for issues ranging from allergies to chronic illnesses.

The concierge model remains aspirational rather than fully operational, and lacks complete funding in recent legislation. The One Big Beautiful Bill (OBBB), passed July 4th, includes a $50 billion “Rural Health Transformation Program” to improve access in underserved areas, but does not explicitly finance Kennedy’s nationwide concierge or direct primary care approaches. Powerful insurers’ lobbying efforts contributed to this omission.

Instead of universal access legislation, the concierge approach provides Americans with a practical, affordable, and accessible alternative that renders traditional HMO models nearly obsolete. It rebuilds the doctor-patient connection, eliminates prior authorizations, and removes network constraints. Insurance becomes optional rather than mandatory.

Kennedy and China: Innovation in preventive care and telemedicine

Kennedy’s plan draws inspiration from China’s model, incorporating preventative care, modern communication tools, and AI—technologies underutilized in the U.S.—to deliver efficient, cost-effective care. This method addresses issues untouched by previous private-versus-public debates.

Early detection reduces treatment costs and complexity while improving patient outcomes. Telemedicine enables consultations from home, reducing unnecessary ER visits, hospital stays, crowded clinics, and transmission of contagious diseases. Workplace clinics and health savings accounts promote wellness. Fundamentally, Kennedy’s plan operationalizes the idea that healthcare should prioritize sickness prevention rather than merely treatment payment.

Americans from three generations have accepted expensive, complicated, intermediary-driven care as a given. The concierge concept challenges this norm by proposing care that is simple, direct, affordable, and preventive. Its widespread adoption could eliminate costly administrative layers without improving outcomes.

Drawing historical lessons – Bismarck (not Kaiser!) and practical conservatism

Otto von Bismarck, Germany’s Iron Chancellor, introduced multi-payer universal healthcare in 1883 motivated less by ideology than by pragmatic conservatism. He understood that a healthy workforce was productive and that a social insurance fund could undercut socialist agitation. Similarly, the concierge plan offers what progressives have long sought: universal care, preventive medicine, and cost control, but through market-friendly, conservative strategies.

Bismarck versus Kaiser (Permanente) — these ideas demonstrate that social welfare and conservative governance can coexist. Kennedy’s approach embodies this philosophy, emphasizing pragmatism over ideology. It avoids partisan stalemates, circumvents entrenched monopolies, and delivers a practical alternative.

Kennedy’s concierge concept leverages telemedicine, AI diagnostics, and prevention to streamline healthcare and cut unnecessary costs. Combined with a Bismarck-inspired public-private coverage model, these ideas propose a modern public option that preserves quality and access while reducing reliance on the Health Industrial Complex. They extend beyond the immediate fight over ACA funding.

Nonetheless, the record-breaking government shutdown and high-profile outbursts of rage—like Luigi Mangione’s murder of UnitedHealthcare CEO Brian Thompson—signal deep systemic dysfunction. Until Americans confront a broken system where institutions protect corporate interests over citizens, such crises will persist, undermining trust domestically and internationally. The broader goal to “Make America Great Again” cannot be realized while citizens remain ill, financially crippled by healthcare costs, or perish prematurely before witnessing that vision.