Climbing the Mt. Everest of Worry

The S&P 500 has just achieved a new record high.

This has happened amid an energy crisis, two ongoing wars, a developing credit crunch, and soaring deficits.

While stocks are known for “climbing the wall of worry,” this scenario feels more like attempting to scale Mount Everest wearing sweatpants and a hoodie.

Current optimism largely stems from a broad belief that the conflicts are winding down. However, even if that holds true, the existing damage is considerable.

Indeed, the ceasefire with Iran remains intact and is hopefully set for renewal before it expires on April 20th.

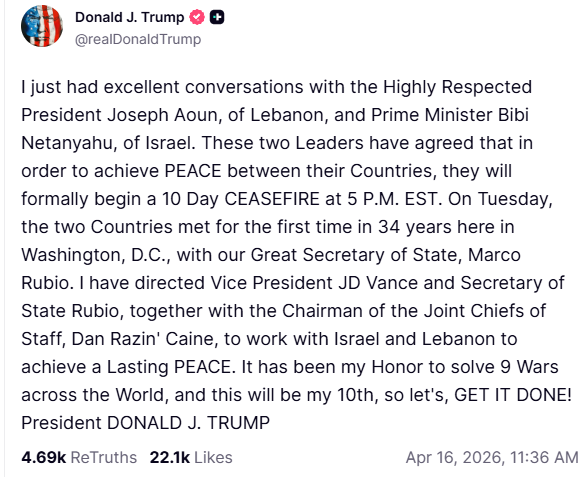

In more encouraging developments, President Trump announced that Israel has consented to a 10-day truce with Lebanon (where Hezbollah is based).

Source: Truth Social

This is an encouraging sign, but forging lasting peace between Israel and Hezbollah remains a significant hurdle.

Nevertheless, the Lebanon ceasefire addressed one of Iran’s main concerns. We’ll need to observe if this progress leads to reopening the Strait of Hormuz.

A Deal Could Be 6 Months Out

While the ceasefires mark genuine advancement, they are delicate and might prove temporary.

Crucially, the Strait of Hormuz remains shut, even more so as the U.S. blockade restricts Iranian shipments from exiting the Gulf.

The path to a sustainable resolution hinges on an agreement.

According to Bloomberg reporting, negotiations might stretch for six months:

“Some Gulf Arab and European leaders believe that a US-Iran peace deal will take about six months to be agreed and that the warring sides should extend their ceasefire to cover that timeframe, according to officials from the regions familiar with the matter.”

I concur; securing a durable deal will likely require at least that much time.

Of course, we hope the Strait reopens sooner, but it represents Iran’s chief bargaining chip, and they won’t relinquish it easily.

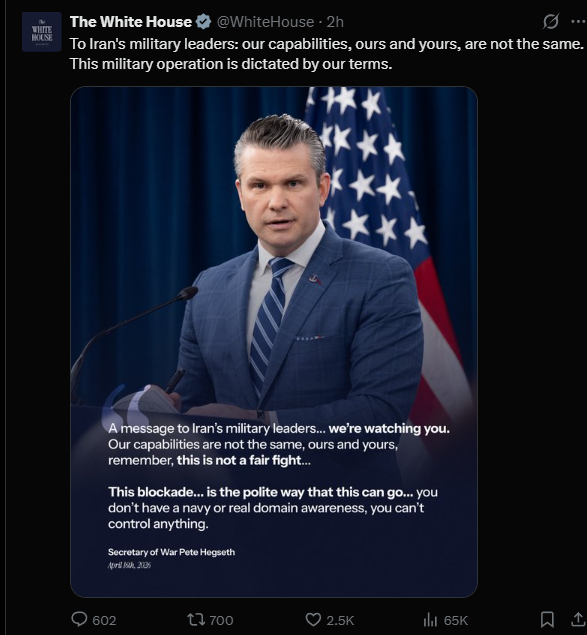

Meanwhile, the White House recently emphasized a comment from Secretary of War Pete Hegseth, who said, “This military operation is dictated by our terms”.

President Trump appears confident that Iran can be pressured into reopening the Strait quickly and reaching a deal. We can only hope this strategy succeeds.

A Return to Wartime Production Mode?

Elsewhere, the Pentagon has approached Ford and GM about repurposing some plants for military weapons manufacturing, according to the WSJ:

“The Trump administration wants automakers and other American manufacturers to play a larger role in weapons production, reminiscent of a practice used during World War II.

…The Pentagon is interested in enlisting the companies to use their personnel and factory capacity to increase production of munitions and other equipment as the wars in Ukraine and Iran deplete stocks.”

It’s clear there’s a need to replenish armaments deployed in Ukraine and the Middle East. Key systems like HIMARS and cruise missiles are backlogged, with allies waiting for years.

The push to convert factories suggests these weapons might be urgently required soon.

Last night, the Washington Post reported that an additional 10,000 U.S. troops are heading to the Middle East, accompanied by the George H. W. Bush aircraft carrier strike group.

More American missiles, bombs, and military aircraft are also being deployed from various parts of the globe.

Iran is busy restoring its underground “missile cities,” which suffered severe damage from U.S. and Israeli bunker-busting bombs. The country is also utilizing the ceasefire to fix bridges, power stations, energy facilities, and relocate military hardware.

Make no mistake: this conflict could reignite at any moment, yet the market largely overlooks this threat.

Portfolio Prepping

I remain invested in a few long-dated put options, though they constitute only a small fraction of my holdings. The most reliable hedge right now is specific oil stocks not impacted by turmoil in the Middle East.

Gold and silver have bounced back well, with miners following suit. However, I remain cautious about miners’ short-term prospects until the Strait of Hormuz reopens.

As long as oil prices stay high, miners face headwinds. Yet, the bullish case remains intact, and once the energy crisis resolves, miners should once again significantly outperform. For long-term investors, maintaining positions is the wisest move—this is my approach.

It’s prudent to keep a higher-than-usual cash reserve now. While many investors rush back into tech stocks, a more measured stance is advisable.

Ridiculously Expensive

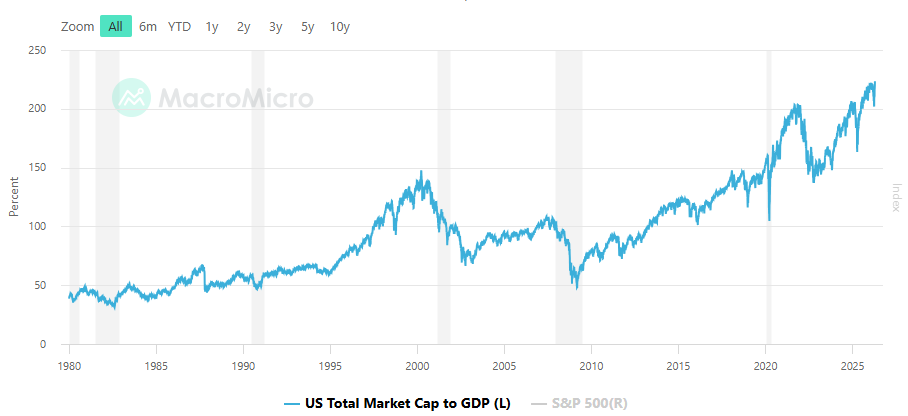

U.S. equities are currently far more expensive than during the dotcom bubble peak in 2000, based on multiple metrics including dividend yield, price-to-sales ratios, and especially the Buffett Indicator.

The Buffett Indicator, Warren Buffett’s preferred valuation metric, contrasts U.S. stock market capitalization with GDP. Here’s a historical chart:

During the dotcom bust, the Buffett Indicator peaked at 137%. This level wasn’t exceeded again until the market frenzy triggered by COVID.

Today, the figure stands at an astonishing 223%!

This means U.S. stocks are valued at 223% of GDP—a historically inflated level. Consequently, Warren Buffett holds $373 billion in cash, which is more than a third of Berkshire Hathaway’s assets.

Given this turmoil, the rush of investors into U.S. stocks seems somewhat irrational.

Our approach of focusing on hard assets and emerging markets is yielding positive results and should continue to outperform the S&P 500 and Nasdaq. In a widespread selloff, these investments tend to decline less, while offering better upside than pricey U.S. indices.

My recommendation: avoid getting swept up in hype and buying into overvalued stocks.

More updates soon.