He Bought the Tippy-Top

By 1999, Stanley Druckenmiller had already established himself as a legend.

Between 1981 and 2000, his hedge funds never recorded a losing year.

His annual returns averaged an astonishing 30%. Druckenmiller caught George Soros’s eye and soon took the helm of the renowned Quantum hedge fund.

In 1999, spotting the internet bubble expanding, he placed a $200 million short bet on tech stocks.

However, as the bubble continued to swell, his short position suffered a $600 million loss.

In response, Druckenmiller recruited two talented tech specialists and allocated funds for them to manage. They invested in the hottest stocks and soon gained 3% daily.

These young tech traders made their leader seem outdated.

Druckenmiller recounts how FOMO gripped him:

“So like around March [of 2000] I could feel it coming. I just — I had to play. I couldn’t help myself. And three times the same week I pick up a phone — don’t do it. Don’t do it. Anyway, I pick up the phone finally.

I think I missed the top by an hour. I bought $6 billion worth of tech stocks, and in six weeks I had left Soros and I had lost $3 billion in that one play.”

Pause for a moment to consider this: one of history’s greatest investors purchased at the very peak of the dotcom bubble—and endured a $3 billion loss.

Druckenmiller has admitted that he knew it was a poor move but couldn’t resist the temptation.

“I didn’t learn anything. I already knew that I wasn’t supposed to do that… I was just an emotional basketcase and I couldn’t help myself.”

This illustrates the power and peril of FOMO. Witnessing skyrocketing stock prices can push us toward irrational decisions.

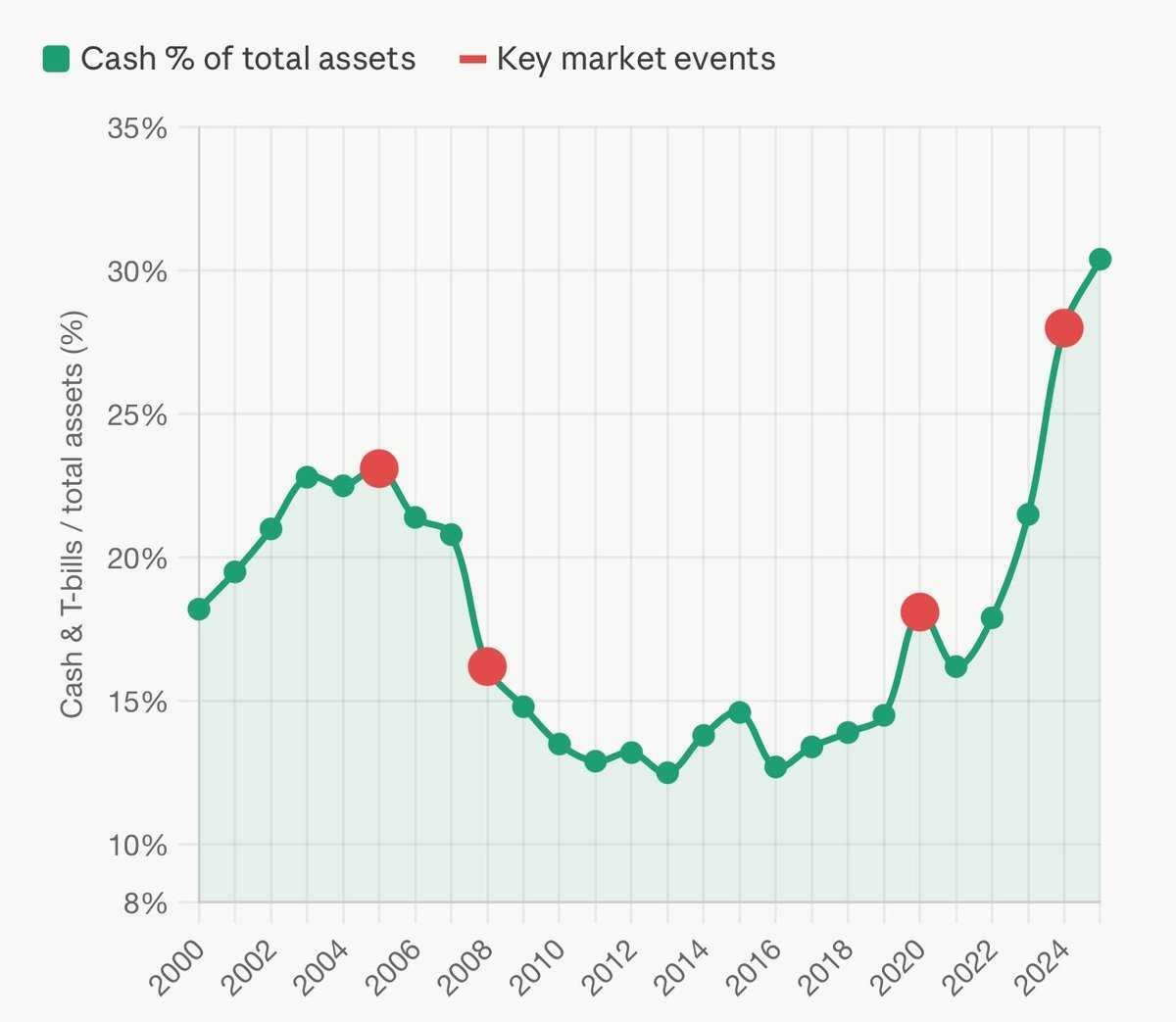

Berkshire’s $397B Cash Hoard

Berkshire Hathaway (BRK.A, BRK.B), Warren Buffett’s famed enterprise, is currently holding a record $397 billion in cash and Treasury bills.

As a holding company, Berkshire owns substantial shares in various stocks and private firms such as Geico insurance.

This $397 billion represents nearly a third of Berkshire’s total assets, sitting idle at just 3-4% returns while the broader market advances.

Nonetheless, Berkshire remains steadfast, patiently awaiting “fat pitches”—in other words, market downturns offering significantly discounted stocks.

Before the 2008 financial crisis, Berkshire adopted a similar strategy, with cash reserves peaking at 23% of assets.

When those prime opportunities surfaced, Berkshire had ample liquidity to deploy. Notably, they invested in Goldman Sachs (GS) when the banking sector showed signs of instability.

Buffett acquired $5 billion in preferred shares with a perpetual 10% dividend and secured warrants to purchase $5 billion worth of stock at $115 each. Today, Goldman Sachs shares trade near $917.

Their standout crisis play was Bank of America (BAC), where Warren Buffett earned approximately $20 billion on that “blood in the streets” investment.

Alongside BAC, they also purchased GE, Dow Chemical, and numerous other stocks at rock-bottom prices during the crash.

This approach showcased the value of patience and striking at the right moments.

However, Buffett deliberately limits his territory. He avoids emerging market stocks and has a distaste for precious metals.

While maintaining some cash reserves is wise, there’s no need to hold as much as Berkshire’s 32%.

Assets With Less Downside, Huge Upside

Before diving further, it’s important to clarify that this advice applies to long-term investing. Short-term trading in hot stocks can be appropriate for some.

The long-term segment of my portfolio is geared toward assets that can withstand market turmoil: natural resources, emerging markets, and precious metals. Most people lack sufficient exposure to these areas.

When a market correction occurs, being heavily invested in overcrowded sectors can leave you trapped by a narrow exit.

For instance, from 2000 to 2002, the Nasdaq plummeted 78%, and the S&P 500 dropped about 49%.

During that downtrend, oil stocks appreciated roughly 20% plus dividends. Gold miners flourished even more, with the NYSE Arca Gold BUGS Index surging over 100% from 2000 to 2002.

These resource stocks continued to outperform for an additional eight years.

Emerging markets also outpaced the S&P 500 and Nasdaq throughout the dotcom collapse. The MSCI EM index declined only about 25%, rebounded swiftly, and topped U.S. stocks for years thereafter.

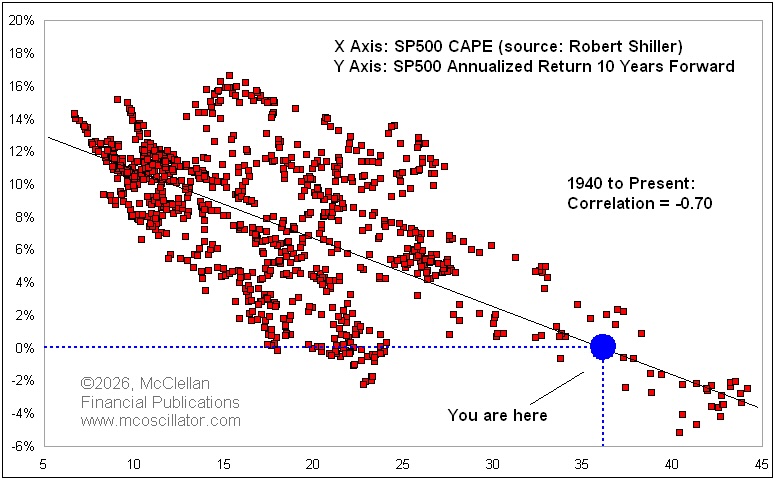

The takeaway is straightforward: U.S. equities are currently highly valued, and historically, such conditions have led to weak future returns.

The chart below plots the CAPE ratio (a 10-year metric of stock valuation) for the S&P 500 on the x-axis against subsequent annualized returns on the y-axis.

With today’s CAPE ratio near 36, average returns over the following decade have been close to 0%.

Source: Tom McClellan

Though the S&P 500 might surge another 15%, that would likely indicate a “blow-off” peak. A market crash is inevitable at some point. The length of time for overpriced stocks to recover after a crash is uncertain—as seen after the 2000 dotcom bust when it took over a decade.

I’m not advising you to sell all your shares. My recommendation is to diversify by adding alternative assets such as natural resources, emerging markets, and precious metals.

These asset classes have seen significant declines recently, especially after the Iran conflict began. However, I continue to hold and gradually increase my positions when I have extra capital.

Eventually, there will be an opportunity to exit these non-traditional assets and rotate into conventional growth and income stocks.

That shift will only be prudent when yields on typical U.S. stocks improve and valuations fall.

To emphasize once more—this strategy suits long-term investors. Trading overheated stocks may offer profits but requires disciplined risk management.