Will the SpaceX IPO Zuck Early Buyers?

Davis Wilson, my friend and editor of Paradigm Press’s Million Mission, authored an article on the Facebook IPO that stirred a blend of fond memories and concern in me.

Let me begin with the nostalgia.

The Big G

By 2012, I had relocated to Singapore but frequently traveled back to London, my former home, to catch up with friends and clients. One of these friends, G, was a Goldman Sachs partner who had settled in New York after graduating from London Business School alongside me. However, he later returned to London to work at Goldman’s Fleet Street branch. With a mathematician and engineer as parents, G naturally excelled at the rather routine math that finance demands. He generated a great deal of wealth, both for Goldman and himself.

Spending time with G was always enjoyable—he was sharp, entertaining, and incredibly wealthy. More importantly, whenever I faced complex material, he’d meet me at a pub to break it down. Once, I had to teach a Credit Derivatives class. After a single glass of single malt scotch and two hours with him, I had a Goldman-level grasp of the concepts: definitions, pricing, applications, and back office processes. Plus, he shared intriguing stories that captivated the class. They certainly got their money’s worth.

Those were truly great days.

I mention G because of a particular conversation we had about the Facebook IPO that has stuck with me ever since. It was a transformative moment—a true “scales falling from the eyes” realization—showing me just how ruthless the business world can be.

Before META, There Was FB

META feels like old news now, especially since its Metaverse project flopped so badly the company dropped the term. Meta’s virtual reality wing, Reality Labs, has recorded losses totaling $83.6 billion over six years.

Back in 2012, Facebook was the hottest topic. It’s almost comical to recall that their biggest challenge was still cracking online advertising. Eventually, with innovations like the Facebook Pixel, they dominated that space and earned enormous sums for themselves and their investors—money enough to waste on a failed VR gamble costing billions.

The IPO was eagerly awaited, in part to finally appraise Facebook’s true worth. Older readers might recall Diane Sawyer’s famously awkward interview with Zuckerberg, a bizarre mix of Mrs. Robinson and Sheldon Cooper. Ewwww…

Morgan Stanley was appointed lead bank after doing extensive pro bono work for Facebook before the IPO. JP Morgan served as the second bank, with Goldman Sachs lagging behind in third place—an embarrassing spot for them. Even Facebook’s executives, with close ties to government, had little fondness for the “vampire squid.”

This turned out to be a hidden blessing for Goldman. Morgan Stanley’s mishandling of the IPO caused a severe reputational blow, sparing Goldman from the fallout. How exactly did Morgan Stanley flub the deal?

The IPO Numbers

On face value, Facebook’s IPO seemed a capitalist victory. The demand exceeded supply fivefold, prompting Morgan Stanley to increase the price from $28–35 to $34–38, boost the share count by 25% to 421 million, and deliver Zuckerberg a $100 billion valuation.

Facebook CFO David Ebersman had quietly aimed for that figure all along—round, symbolic, and essentially meaningless as a future indicator but perfect for Wall Street theatrics.

Yet below this polished exterior was trouble: just 11 days before the IPO, Facebook quietly informed Morgan Stanley they were cutting revenue forecasts. Mobile usage was cannibalizing desktop faster than Zuckerberg’s ads team could monetize, leading to fewer ad views and less income. This was a significant detail.

Institutions at Morgan Stanley received this heads-up, but retail investors eagerly snapping up shares on the IPO day were left with only a shiny prospectus built on selective disclosure. The oversubscription making the deal appear invincible was crafted through an information imbalance.

This scenario puts bankers in a tough spot: balancing the interests of the issuer—in this case, Facebook, whose goal is maximizing capital raised—with those of investors such as pension funds, insurers, endowments, hedge funds, and other asset managers banking on the typical 10% IPO day bounce.

Morgan Stanley had just guaranteed a year and a half of praise-seeking and concessions from IPO buyers.

Was FB’s IPO a Failure?

The straightforward answer is, “It depends.”

For IPO investors? Definitely. They got a raw deal.

For Morgan Stanley? Yes, an utter embarrassment for the equity origination team.

For Mark Zuckerberg? Absolutely not. It marked one of the best days of his young career.

This reminds me of my conversation with G. I recall saying something like “Ha! Morgan Stanley—what a flop…”

He responded, “Failure? For whom?”

I gave him a puzzled look.

“Seanie, Facebook raised $16 billion. Zuck never has to return to the market!”

If you invest often in mining stocks, think of how many times you’ve been diluted just within the past year.

Mark Zuckerberg, in contrast, has barely burdened his shareholders with dilution. Apart from the IPO, the only other notable equity offering he made was in December 2013 to cover a tax bill. The details:

- 27 million shares sold by Facebook itself (~$1.5B, for operational funds and general corporate use)

- 35 million shares sold by Zuckerberg personally (to cover taxes from exercising 60 million Class B stock options)

- 6 million shares sold by Marc Andreessen

That’s all.

From Facebook’s standpoint, this was perhaps the most successful IPO ever.

But for those who bought shares on Day One… that stung.

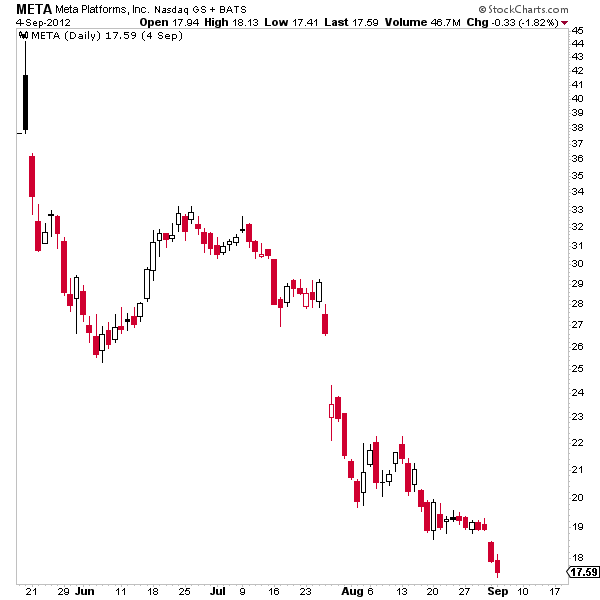

Consider the chart.

After debuting at $38 and briefly touching nearly $45 during its first trading day, FB’s value halved over five months, closing at $17.59. If you’re a fund suffering those losses, you likely berate your inept banker daily.

It’s said the three banks had to complete 85 subsequent IPOs over the next 18 months to compensate their institutional clients for the missing “money on the table.” Several hedge funds claimed shorting Facebook stock was their most profitable move that year.

Of course, Facebook later turned into an investor favorite, creating multimillionaires.

Elon’s SpaceX IPO

Now, for the alarm following the nostalgia.

To be clear, I’m writing this via my Starlink dish because Telecom Italia is hopelessly unreliable. Elon Musk is undeniably a genius and a clear net positive for humanity, and I’d have gladly supported him finishing the DOGE project by slashing government expenditures.

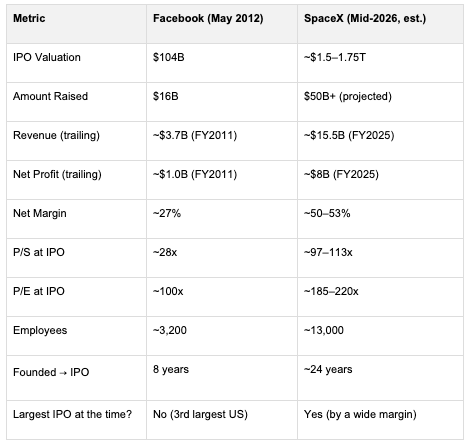

Here’s how Facebook’s IPO compares to SpaceX’s:

Elon aims to raise $50 billion, and frankly, I hope he succeeds.

But should you invest?

Yes, but only after the IPO, when the price likely plunges at least 50% from the absurdly high levels it will initially be set at.

I recall Scott McNealy’s thoughts years after Sun Microsystems’ stock collapsed:

At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?

With a price-to-sales ratio close to 100, Elon would need to deliver 100% of revenues for 100 straight years as dividends, all while meeting McNealy’s other daunting assumptions.

Good luck to him.

Again, Elon’s work benefits humanity greatly, but I plan to let the overinflated fund managers—who have thrived on decades of Federal Reserve-issued easy money—shoulder this risk.

And you should consider doing the same.

Wrap Up

Few moments in history offer clearer warnings. Facebook’s IPO sets the precedent. SpaceX lies ahead of us.

While we root for Elon’s cosmic ambitions—or at least his Martian hopes—we ordinary folks on Earth should protect our own interests instead of getting wiped out by this IPO.