Portfolio Prepping

Last Friday marked the most significant Nasdaq drop ever recorded by points.

Monday, however, brought unexpected calm as stocks bounced back, allowing traders to relax briefly.

Today saw volatility return, albeit only for a short time.

As of 2:40pm, the Nasdaq 100 has declined 1.2%, after earlier plummeting as much as 3.5%. The S&P 500 dropped less than 1% but was down around 2% near midday. Gold, silver, and mining stocks also experienced losses.

Although the selloff was intense initially, equities have since clawed back some losses.

The key question remains: are we nearing a market peak or is this just another false signal before new record highs?

The Guy Who Called Bear

During the past year, I’ve suggested multiple times that the market might be close to a top, most recently at the start of the Iran conflict.

Turns out, I was mistaken. The bull market has proven relentless, overpowering any opposition.

Undoubtedly, a significant correction or even a “lost decade” lies ahead eventually. Yet, the timing and extent of the eventual downturn remain uncertain.

One thing is clear: stocks are historically overvalued, priced for perfection. The chart below illustrates the S&P 500’s CAPE ratio (cyclically-adjusted price-to-earnings), reflecting valuation levels over a 10-year span adjusted for inflation.

Source: Multpl.com

As shown, only the 2000 dotcom bubble exceeded these valuation levels. Interestingly, that peak was much larger than the one in 1929. It’s uncertain if this time could surpass those highs.

When a bubble of such magnitude bursts, it often takes years to regain lost ground. After the 2000 crash, the S&P 500 took about 13 years to fully recover, factoring in inflation and reinvested dividends.

The Nasdaq 100, by similar measures, required roughly 18 years to reclaim its prior peak, highlighting the lengthy recovery process.

This pattern typically follows episodes of extreme overvaluation: extended periods of underperformance. That appears to be our current situation.

Personally, I’m bracing for the bull market to end relatively soon, though I am not betting against it with shorts. Instead, I’ve gradually redirected some holdings away from broad U.S. equities toward specific sectors expected to excel moving forward.

I’m not advising a wholesale sell-off or abandoning all tech or U.S. stocks. But for those who have realized solid gains, locking in profits and diversifying into less favored and lower-priced areas could be wise.

Where to Hide Out

In a severe market plunge, cash might be the safest refuge. Holding a reasonable cash position today has merit, especially when it yields a competitive return, whether via banks or money market funds.

U.S. government bonds (Treasuries) might offer some short-term safety, but I’m cautious about heavy long-term exposure for various reasons. Still, Treasury bills and notes remain a relatively secure source of yield.

Physical assets like gold, mining stocks, and oil can decline during crashes, yet they typically rebound strongly once markets stabilize.

History backs this up: after the 2000 crash, gold, silver, and miners soared for over a decade, significantly outperforming equities. That’s why I maintain positions in precious metals and keep cash ready to purchase more if a substantial selloff occurs.

Emerging markets, particularly Brazil (EWZ), remain appealing to me. The downturn presents a promising long-term buying opportunity in this favored South American market.

Another area of interest is battered consumer staples such as Campbell’s (CPD), which we discussed yesterday. Notably, Campbell’s climbed up to 2.3% today amid broad market weakness, with General Mills (GIS) also showing strength.

Many of these stocks have been cut in half or more recently. Should the market turn upward, cheap and unloved sectors are likely to lead gains.

That said, I’m not entirely bearish. My portfolio holds a few small put options, representing less than 1%. This market could still “rip faces off” to bears, as the saying goes.

I prefer to invest in assets with strong upside potential, limited downside risk, and resilience in downturns compared to high-flying stocks.

The SpaceX Complication

This week is pivotal in market history, with the largest IPO ever scheduled for Friday.

If the market continues sliding, the chance of the IPO underperforming (pun intended) increases. Conversely, a rally combined with a strong debut could boost investor sentiment for weeks ahead.

I don’t claim certainty on the outcome. Yet, the market feels top-heavy again. A weak SpaceX IPO would likely weigh negatively on future market momentum.

On the other hand, if SpaceX surges 30% on its first day, it would inject more liquidity and gains into the market. It’s difficult to call — this event could swing either way.

The Iran Situation

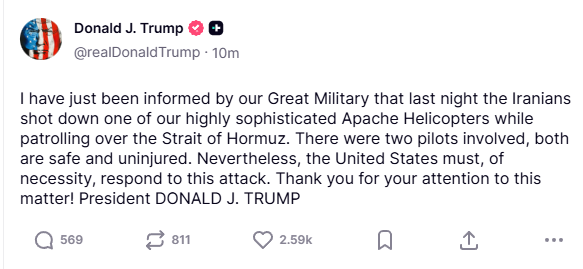

Earlier today, shortly after noon, President Trump shared a message on Truth Social.

Given this, reopening the Strait of Hormuz soon appears increasingly unlikely.

The prospect of a full-scale war resuming poses a significant threat to markets—one largely overlooked until now.

In recent months, optimism and hope have driven sentiment, ignoring the harsh realities of shrinking oil inventories and consumers facing higher costs.

If conflict reignites and oil infrastructure is targeted, energy prices could spike, likely triggering a market crash. Yet, this volatile market sometimes defies logic, so perhaps prices will stabilize and new highs will be reached despite ongoing risks.

Tomorrow, a special Daily Reckoning by Jim Rickards focusing on the Iran crisis will be released. Jim has demonstrated unmatched foresight regarding this conflict, so expect valuable insights in your inbox at 6:00pm ET.