Warsh Declares Fed Independence

As predicted in Tuesday’s preview of the FOMC meeting, the Federal Reserve opted to keep interest rates steady during the June 17 session. This decision maintains the Fed funds target range at 3.5%–3.75%, a level unchanged since December 10, 2025.

We will break down the Fed’s recent policy move, the key messages delivered by Kevin Warsh in his debut as chair, and why this could signal a transformative shift for the central bank.

UPDATE: “Not the stale Bernanke-Yellen-Powell Fed”

To start, here is the pertinent segment of the Fed’s statement released at 2:00 p.m. ET on Wednesday:

The Committee decided to maintain the target range for the federal funds rate at 3.5% to 3.75%, in support of the Federal Reserve’s dual mandate. The Committee reaffirmed its policy of maintaining ample reserves in the banking system.

Economic activity is expanding at a solid pace despite elevated uncertainty that owes, in part, to the conflict in the Middle East. Productivity growth and capital investment are strong. Job gains have kept pace with the workforce, and the unemployment rate has changed little.

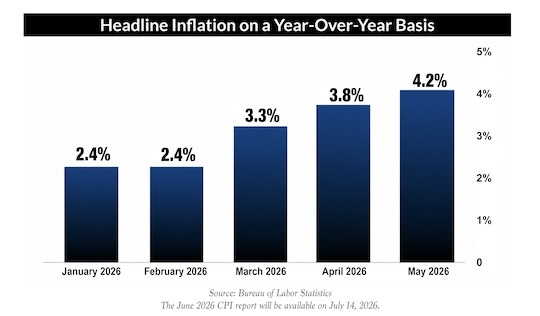

Inflation remains elevated relative to the Committee’s 2% goal, in part reflecting supply shocks that have driven price increases in certain sectors, including energy. The Committee will deliver price stability.

This meeting included a Summary of Economic Projections (SEP), which is a set of predictions on interest rates, unemployment, economic growth and other key metrics issued by the Fed governors and the 12 regional Federal Reserve Bank presidents.

These “dots,” representing the SEP on a graph, are largely speculative and unreliable. While they hint at current thinking, their predictive power is minimal and they have a strong track record of inaccuracy.

The logic behind maintaining steady rates is clear. Inflation remains above the Fed’s 2.0% target, climbing quickly without near-term signs of easing.

Meanwhile, unemployment has hovered between 4.3% and 4.5% since July 2025. This rate is moderate and stable.

With inflation intensifying and unemployment steady, the Fed’s policies clearly prioritize combating inflation above all else.

Practically speaking, this meant no rate cuts. Although some advocated for a hike, most believed inflation might self-correct in upcoming months due to a sharp fall in oil prices, prompted by a ceasefire extension in Iran and prospects of reopening the Strait of Hormuz.

That expectation was enough to hold off on raising rates this time.

Given that this was Kevin Warsh’s inaugural meeting as chair, there appeared to be a consensus within the FOMC to back him strongly right from the start.

The vote reflected this with a unanimous 12-0 decision to maintain the status quo.

While the rate decision was routine, the meeting’s broader significance was profound.

Chair Warsh used both the FOMC statement and his press conference to underscore crucial points. He made it evident that this Fed will be distinct—“not the stale Bernanke-Yellen-Powell Fed.”

Highlights of key changes include:

- Warsh opted out of contributing to the Summary of Economic Projections (SEP), signaling two things: he does not assign it much importance, and he is likely to eliminate the “dots” soon. This will be a welcome change.

- The unanimous vote to approve the policy contrasts with prior meetings that featured dissents, including April 2026’s unprecedented four-no votes. This unanimity demonstrates Warsh’s current strong grip on the committee.

- The FOMC statement was notably succinct—much shorter than in previous years—reflecting Warsh’s preference for brevity. Expect fewer leaks, less verbose releases, and a greater focus on attentively observing market signals.

- Neither the FOMC nor Warsh provided any forward guidance. Historically, since Ben Bernanke’s tenure, the Fed has believed that projecting future inflation and growth could shape consumer and investor expectations to meet targets. (This approach was always questionable; I’ve encountered Bernanke in person, and he’s as confident as his reputation suggests.)

Warsh acknowledges that markets and the broader economy operate independently of the Fed’s machinations, influenced by far more variables than the Fed can control or anticipate.

- Warsh established five autonomous task forces charged with reviewing essential Fed operations. Their focus areas encompass communications, balance sheet management, use of existing data, the role of productivity and jobs amid transformation, and the Fed’s inflation framework.

The task forces’ findings might take months or longer to emerge. However, the chosen subjects point toward substantive operational reforms.

Expected changes include increased Fed listening and reduced communication, possible downsizing of the balance sheet through selling or not reinvesting intermediate- to long-term securities, a focus on AI’s workforce impact, and favoring more diverse inflation gauges rather than relying solely on core PCE.

Taken as a whole, these shifts signify more than a new chair—they signal the advent of a fundamentally different Fed.

Warsh’s views and plans were summed up by this excerpt from his post-FOMC press conference:

We recognize that inflation has been running well ahead of the Fed’s long-stated inflation goal of 2%. That’s been going on for more than five years. Persistently high prices are a burden for the American people.

But the recent past need not be prologue. I am pleased to report that members of the FOMC are unambiguous and unanimous: This Committee will deliver price stability.

At any institution, a change in leadership is a natural and timely opportunity to reaffirm its mission, to review current practices and to consider whether those practices best meet our objectives.

On that score, you might have already noticed something: a difference in today’s policy statement. It’s a bit shorter, a bit simpler — and it dispenses with some older language.

That statement just gives you the facts, as best we can judge it. Absent, also, is so-called ‘forward guidance,’ which we agreed was not well-suited to the current policy conjuncture.

This afternoon you also received the usual Summary of Economic Projections. It’s been the practice of this Committee for participants to submit these projections, and I have encouraged my colleagues to continue to do so. I, however, have refrained from offering any projections of my own — consistent with my long-held views on the SEP, at least as currently structured.

In the median projections, real GDP rises at 2.2% this year, 2.3% next year, and total PCE inflation runs at 3.6% this year, 2.3% next year. The unemployment rate stands at about 4.3%. The median participant judges the appropriate federal funds rate to be at 3.8% at the end of this year and 3.6% at the end of next.

In essence, Warsh is signaling that the Fed plans to stop directing markets and instead focus on interpreting their cues.

Markets exceed the Fed’s influence and provide rich insight into the economy’s health—if one knows where and how to analyze.

Indicators such as yield curves, swap spreads, and TIPS breakevens are far more insightful than outdated Fed doctrines like the Phillips Curve, forward guidance, or supposed wealth effects.

It remains to be seen whether Warsh can succeed in ending the Fed’s longstanding streak of erroneous forecasts.

Apart from structural reforms, the Fed’s internal conflict between prioritizing inflation versus unemployment will be clarified. Inflation is expected to diminish naturally due to a slowing global economy and an impending recession, while unemployment is likely to surge accordingly.

The Fed’s current pause in raising rates exacerbates both problems, but its narrow focus on inflation blinds it to the broader consequences. Ordinary Americans will bear the brunt, facing job losses and business closures.

The next scheduled meeting of the Fed’s Federal Open Market Committee (FOMC) will take place on July 29, 2026. Given ongoing uncertainties around the Iran conflict and the effects of elevated short- and intermediate-term rates, the U.S. economic landscape is expected to look very different by then.