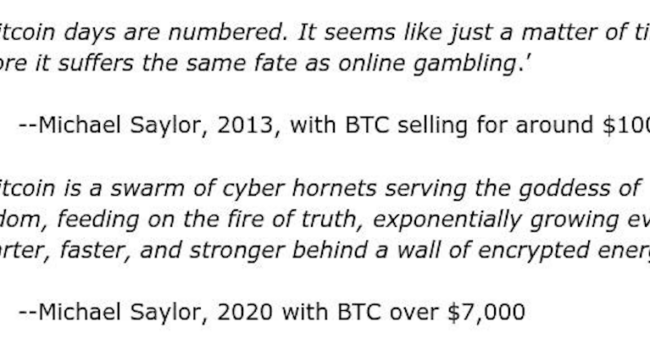

Bad Strategy

Michael Saylor, CEO of Strategy (previously known as MicroStrategy), has a reputation for pushing boundaries, exaggerating claims, and overspending. With Bitcoin currently on a downward trend, he might now be overly invested in it. Bloomberg reports:

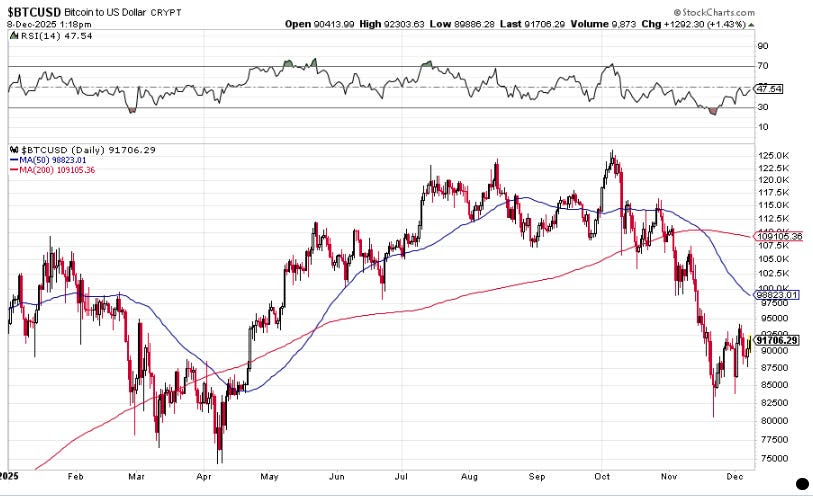

The S&P 500 has climbed more than 16% in 2025, while Bitcoin is down 3% — the first time since 2014 that stocks have rallied while the token is down, according to data compiled by Bloomberg.

The digital asset has rarely deviated so cleanly from other risk assets even during past crypto winters. The dislocation defies expectations that cryptocurrencies would thrive under President Donald Trump’s return to the White House amid favorable regulation and a wave of institutional adoption.

During the dot-com era, Saylor built his reputation by greatly overvaluing internet innovation. He emerged as a leading voice of the dot-com boom—a fervent believer whose average software firm helped drive the bubble.

His confidence might have been misplaced:

“I think my software is going to become so ubiquitous, so essential, that if it stops working, there will be riots.”

The company’s stock price surged. Yet, Saylor had inflated both the worth of his business and its significance. The Nasdaq crashed in March 2000, causing Saylor to lose $6 billion in just one day. Beyond that, the SEC scrutinized him for accounting misconduct, leading to a costly settlement.

Such a collapse could have deterred many, but Saylor persevered. He invested in domain names like Angel.com, Wisdom.com, and Voice.com, which eventually netted him profits. Later, when bitcoin hovered around $8,000, he became excessively optimistic.

We have observed how counterfeit money can create dangerous consequences—manifested in $38 trillion federal debt, a $420,000 average home price, multiple Wall Street bubbles, conflicts, corruption, and a declining empire. This also drives interest in alternatives like cryptocurrency, which claims to avoid the pitfalls of traditional currency.

However, it will inevitably suffer failures of a different sort.

Bitcoin and other cryptocurrencies have demonstrated utility and resilience. Still steering MicroStrategy, Saylor identified a chance for a resurgence—not by innovating a new business, but by adopting a speculative approach.

He transformed his company into a vehicle for owning bitcoin, purchasing bitcoin outright and borrowing funds to acquire more. This arrangement simplified access for investors, removing the need for handling passwords, wallets, or other technical hurdles involved with direct ownership.

Instead, investors could simply buy Strategy (MSTR).

As demand grew, the stock price climbed, eventually trading at roughly double the bitcoin’s value. This positioned the stock not just as a bitcoin proxy, but also as a leveraged way to amplify returns. Matt Levine explains:

Strategy was a leveraged way to invest in Bitcoin, and it got good leverage. A retail (or institutional, really) investor who wants to borrow money to buy Bitcoin will probably have to do so in a risky way: The loans might be expensive and short-term, and they will almost certainly have margin calls, so if the price of Bitcoin drops you need to come up with more money at the worst time. Strategy is a public company, and it borrowed money in safe, long-term, no-margin-call, corporate sorts of ways. It issued convertible bonds with low coupons, and then later it got into issuing perpetual preferred stock: Strategy could borrow money to buy Bitcoin and never pay the money back.

Yet the setup was peculiar. Purchasing MSTR gave exposure to bitcoin, but only about half the amount you’d receive from buying bitcoin directly. Investors saw this as beneficial so long as prices rose. MSTR outperformed bitcoin itself.

Then bitcoin’s value plunged, and that leveraged edge vanished—sometimes turning against investors.

Currently, MSTR is not in immediate peril. The company claims it holds sufficient cash to cover obligations for 21 months. If bitcoin rebounds, the situation could improve.

As Matt Levine observes, MSTR’s leverage comes from selling stock and bonds directly to investors—its lenders. This is advantageous because it eliminates the need for bank financing. Should funds run dry, shareholders bear the loss.