Delayed Impact

In October 1973, Arab oil exporters drastically cut shipments to the U.S.

This occurred amid the Yom Kippur war, a short yet intense clash between Israel and a coalition of Arab nations.

Saudi Arabia and other Arab members of OPEC were upset by America’s support for Israel, leading them to halt oil deliveries temporarily.

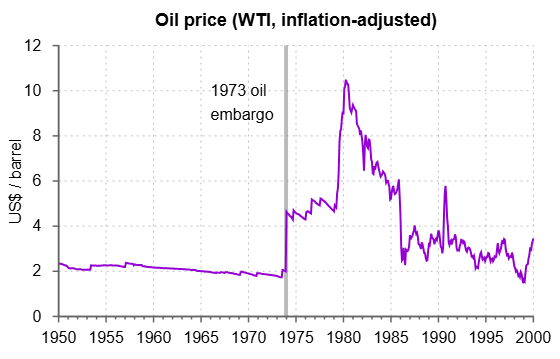

Fuel costs surged. Below is a chart displaying oil prices from 1950 to 2000 (note: the chart is adjusted for inflation, but the 1973 spike is clearly visible).

Oil prices doubled rapidly, and at their highest, barrel costs soared more than four times above early 1973 figures.

Oil prices never reverted to pre-embargo levels, except for a short decline around 1998 (adjusted for inflation), despite the embargo lasting only five months.

Instability in the Middle East tends to breed additional turmoil. Following the Yom Kippur war, the 1979 Iranian revolution expelled Western oil firms, setting the groundwork for current tensions.

Subsequently, the Iran-Iraq war severely disrupted oil output and shipment again, followed by the first Gulf War and the Global War on Terrorism.

The 1973 crisis resulted from about a 5% reduction in oil supply. Currently, we face roughly a 13% decline, which could increase to 20% if the Houthis block the Red Sea as well.

Though we are only nearing two months into this disruption, prolonging the situation could lead to far harsher consequences than the 1973 embargo.

Stocks: A Delayed Reaction

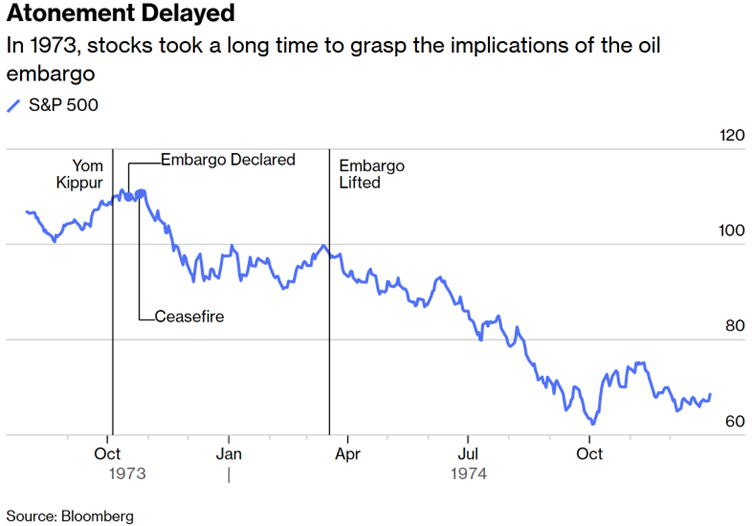

During the five-month 1973-1974 oil embargo, the S&P 500 dropped around 10%. Initially, investors seemed relatively unconcerned.

Interestingly, the stock market plunged significantly after the embargo ended, resembling a textbook “sell the news” scenario:

In the half year after the embargo lifted, U.S. stocks crashed another 35%. Oil prices stayed elevated, and underlying issues persisted.

The economic fallout continued as investors had yet to fully grasp the situation. Government interventions like price controls aggravated matters.

Inflation suppressed consumer spending, slowing the economy, which prompted the Federal Reserve to print excessive money and lower interest rates prematurely.

This cycle defined the stagflation of the 1970s, extending seven years post-embargo.

Not Out of the Woods Yet

Whenever this crisis resolves, hopefully oil prices won’t climb as sharply as they did after 1973. Nonetheless, prices are expected to remain elevated longer than most investors anticipate.

In the best-case scenario, even if this ends swiftly, the damage to oil infrastructure and suppressed demand will leave lasting effects.

Countries will need to rebuild strategic petroleum reserves and substantially increase emergency fuel storage before replenishing them. This alone will sustain pressure beneath oil prices for some time.

In a less favorable outcome, conflict may resume and escalate, a situation that appears increasingly likely.

Jim Rickards has warned about this for a while. In Monday’s Five Links, he informed Strategic Intelligence readers that America and Iran remain far apart on deal expectations, cautioning:

The U.S. is surging special forces, aircraft carriers and Marine amphibious landing units to the area.

Does this sound like the war is ending?

All signs point to more fighting, escalation, higher energy prices, energy scarcity and a major global recession or worse. Trump’s cheerleading won’t change that. Markets need a reality check. They may get one soon.

His perspective is valid. Another U.S. aircraft carrier strike group is currently heading to the Middle East. Missiles, bombs, and aircraft are being moved in from bases worldwide.

Meanwhile, talks are at a standstill. We’re back to “passing notes” through Pakistan. When conflicting parties cannot negotiate directly, a resolution seems distant. Deep mistrust prevails on both sides.

This ceasefire may simply be a pause, as we discussed recently.

I sincerely hope it’s not the case. However, the Strait of Hormuz remains closed to 99% of traffic. As Jim Rickards highlighted today in the Paradigm Press app’s Daily Feed, this remains the key indicator. Everything else is just background noise.

Yet, the stock market acts as if nothing is amiss. A comparable pattern emerged in 1973 initially, followed by a 35% drop over six months.

A similar downturn could unfold again. Currently, the downside risks outweigh potential gains in most U.S. equities, which are too costly to buy except for short-term trades.

In my long-term holdings, I maintain heavy positions in hard assets, precious metals, and inexpensive high-yield emerging market stocks. More insights on this coming soon.