Viva Brasil! A 3X In The Making

Latin American equities have severely underperformed U.S. stocks over the last 15 years.

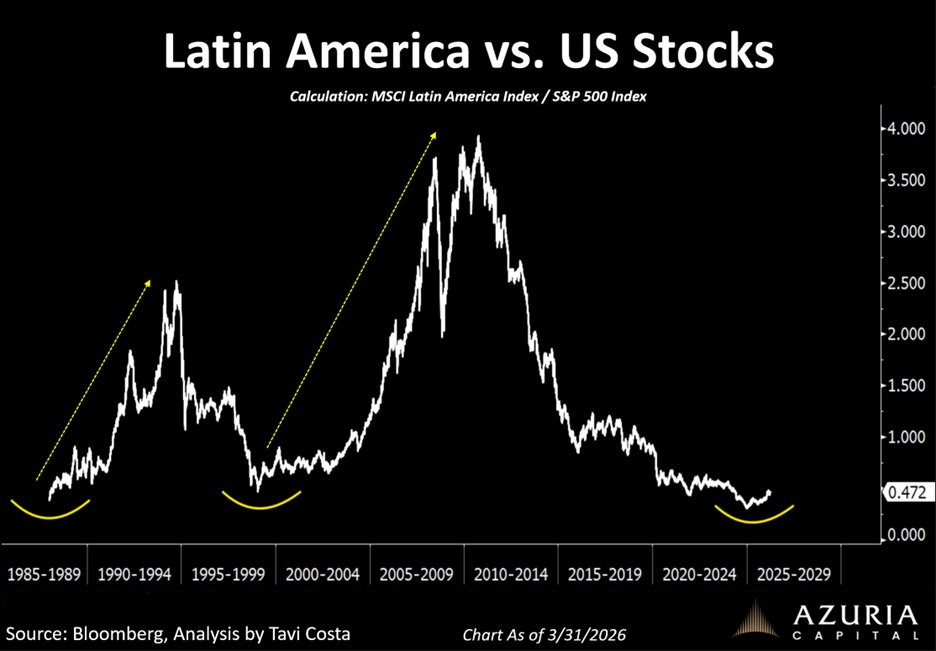

The chart below illustrates the performance of LatAm stocks compared to the S&P 500 since 1985.

When the chart trends upward, Latin American stocks are leading; a downward slope signals U.S. stocks are ahead.

Source: Tavi Costa of Azuria Capital

The U.S. markets have dominated Latin America over the past decade and a half.

However, note that from 2000 to 2009, Latin American equities outpaced the U.S., only to fall behind again from 2009 through 2024. This cyclical behavior was also evident during the late 1980s and early 1990s.

These patterns repeat. We are now at the dawn of a new cycle where Latin America—particularly Brazil—is primed for notable outperformance.

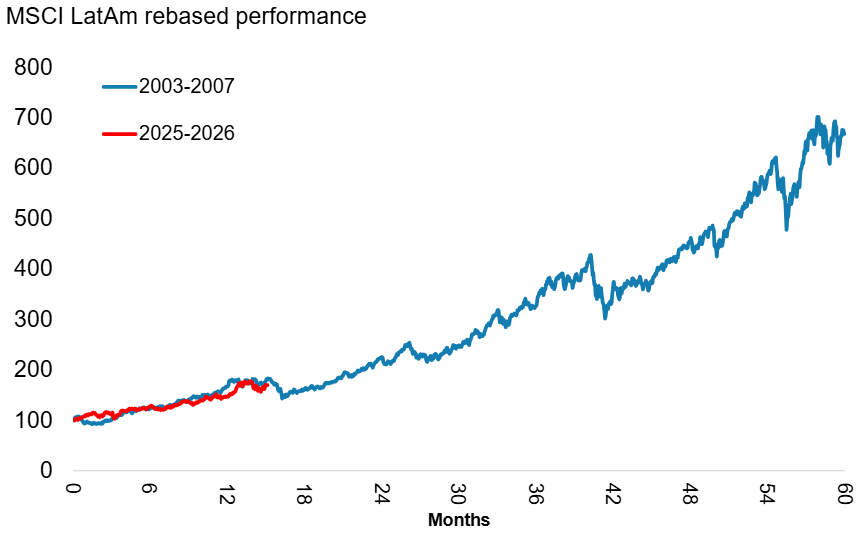

Take a look at this compelling graphic I extracted from a recent investment bank report. It compares the impressive LatAm stock surge from 2003 to 2007 (in blue) with the current rally (in red).

Source: Morgan Stanley Research

This visualization suggests Latin American stocks might be poised for further growth, potentially achieving another roughly threefold increase.

Brazil, currently the most undervalued market in Latin America, has also led the region’s gains over the past year. It boasts abundant natural resources—including oil, iron, gold, copper, silver, rare earth elements, and significant natural gas reserves. Additionally, about 70% of Brazil’s electricity is generated via extremely affordable hydropower.

For exposure to the Latin American resurgence, Brazil remains my top pick.

Viva Brasil!

Since we initially recommended Brazil as a buy in February 2025, the iShares Brazil ETF (EWZ) has climbed approximately 66%, along with attractive dividend payouts.

If this cycle mirrors previous ones (refer to the chart above), the current advance is far from over.

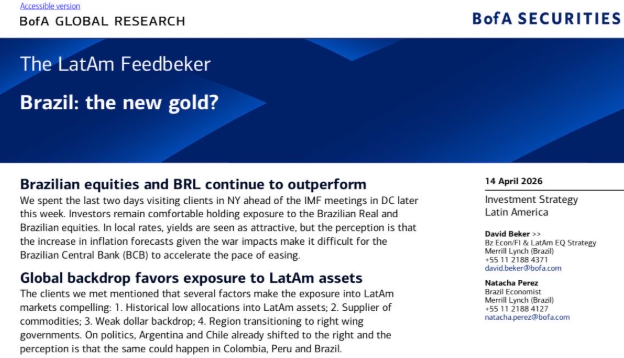

Major investment firms are just now embracing Brazil’s potential. For example, Bank of America recently published a research report titled: Brazil: the new gold?

Source: Bank of America Global Research

Analysts at Morgan Stanley also highlight Brazil as their premier opportunity in South America.

Brazilian equities still trade at very low valuations, with an average forward P/E near 9.

The re-rating of Brazilian stocks is underway and seems likely to continue for several years.

While the LatAm and broader emerging market rally won’t last forever, history shows valuations will be much higher when it eventually ends.

Emerging market cycles follow standard patterns: they begin undervalued and overlooked, then become overvalued and popular. It’s too early to sell until prices reach extreme levels. Much growth still lies ahead.

Why So Cheap?

Why have Brazilian stocks been so undervalued? Much of it stems from the country’s difficult tax structure and regulatory complexity, which made operating there challenging for businesses.

Brazil was often perceived as unfriendly to investment capital.

That has changed recently with the largest tax reform in Brazil’s history.

Drew Crawford, an American investor residing in Brazil, described the reform’s impact in a recent post on X:

Before this, a Brazilian company spent 1,501 hours every year just filling out tax paperwork.

That is five times the Latin America average and ten times the OECD rich country average.

Five separate taxes stacked on top of each other (PIS, COFINS, IPI, ICMS, ISS).

Some of these taxes were calculated on the price that already included other taxes.

A tax on a tax on a tax.

The reform wipes out all five and replaces them with two clean VAT-style taxes (CBS at the federal level, IBS at the state and city level).

Brazil tried and failed to pass this for roughly 40 years.

It is now done.

This development marks a significant shift toward business-friendly policies in Brazil.

As a result, foreign capital inflows should increase, driving faster growth and boosting stock valuations.

Looking ahead, I remain enthusiastic about Brazil. The easiest way to access this opportunity is through EWZ. We’ve also spotlighted Petrobras (PBR, PBR.A), Vale (VALE), and Nubank (NU), all of which have delivered strong returns.

We’ll continue to evaluate emerging market prospects, as I am confident EM will play a crucial role in delivering alpha (outperformance) over the coming years.

Emerging markets remain significantly underrepresented in many portfolios. With likely at least five more years of outperformance ahead, now is not the moment to cash out.

Instead, it’s a period to maintain holdings, reinvest dividends, and await broader investor participation.