The “Iran Deal” Deception

Once again, news suggests that a deal with Iran might soon materialize.

On Thursday, Axios, a media outlet closely linked with the Trump administration, shared this update:

U.S. and Iranian negotiators have reached an agreement on a 60-day memorandum of understanding to extend the ceasefire and launch negotiations on Iran’s nuclear program, but President Trump has yet to give his final approval, two U.S. officials and a regional source involved in the mediation efforts tell Axios. Iran has also not confirmed its acceptance.

Notice the language used: the deal is “mostly agreed to… but both sides still needed approval from senior leadership.”

That hardly sounds like a finalized agreement.

Nevertheless, stocks climbed and oil prices dropped.

Reality Distortion Field

During a conference in New York yesterday, Exxon Senior VP Neil Chapman gave a straightforward take on the oil markets.

“Commercial inventories of crude oil, of liquids, think petroleum, gasoline, diesel, jet fuel, they’ve all run down… We’re approaching unheard of inventory levels. I mean really, really low levels. You can debate whether that’s going to hit those really low levels in two weeks or three weeks.

Once you get to that point, then you’ll see the price shoot up.”

Chapman added that Exxon’s models predict how these low stockpiles might impact prices, concluding that oil reaching $150 to $160 per barrel is quite plausible soon.

Yet, WTI crude currently trades near $87 a barrel, indicating a significant disconnect between market prices and underlying fundamentals.

Despite the current price action, I maintain a strong conviction that oil prices could remain elevated far longer than most experts anticipate.

Talking Oil Down

Every time oil surges, a headline about an imminent peace deal surfaces. Oil prices tumble, while stocks gain momentum. This pattern repeats endlessly.

We’ve witnessed this cycle at least six times now—and it still influences markets.

The real question is: how many more rounds can this tactic keep working?

Violent Repricing

By now, this topic might sound repetitive. But unless the Strait of Hormuz reopens soon, expect oil and inflation to surge dramatically.

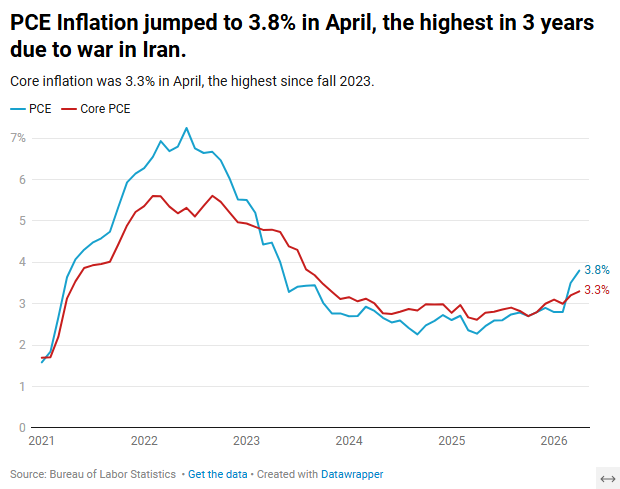

Inflation has been accelerating: wholesale inflation (PPI) jumped 6% in April. Take a look at Personal Consumption Expenditures inflation (blue) and core PCE, excluding food and energy (red):

While inflation is nowhere near the peaks seen in 2022, the trajectory points in that direction. It’s also crucial to remember these official figures typically underreport the extent of true price increases.

The oil crisis likely isn’t resolved yet. If the situation worsens, inflation could spiral out of control.

Deteriorating Economy

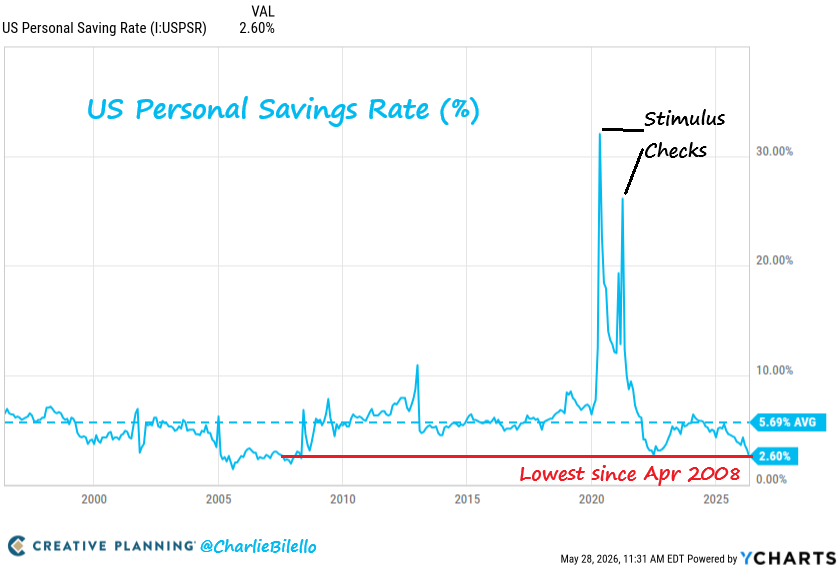

At the same time, real wages declined in April, even as consumer spending rose. This suggests many are relying on credit cards or dipping into savings to cover expenses. Consequently, the U.S. personal savings rate has dropped to 2.6%, a level not seen since 2008.

Source: Charlie Bilello

Many Americans are struggling financially. The only factors supporting our economy currently are AI advancements and spending by the wealthiest.

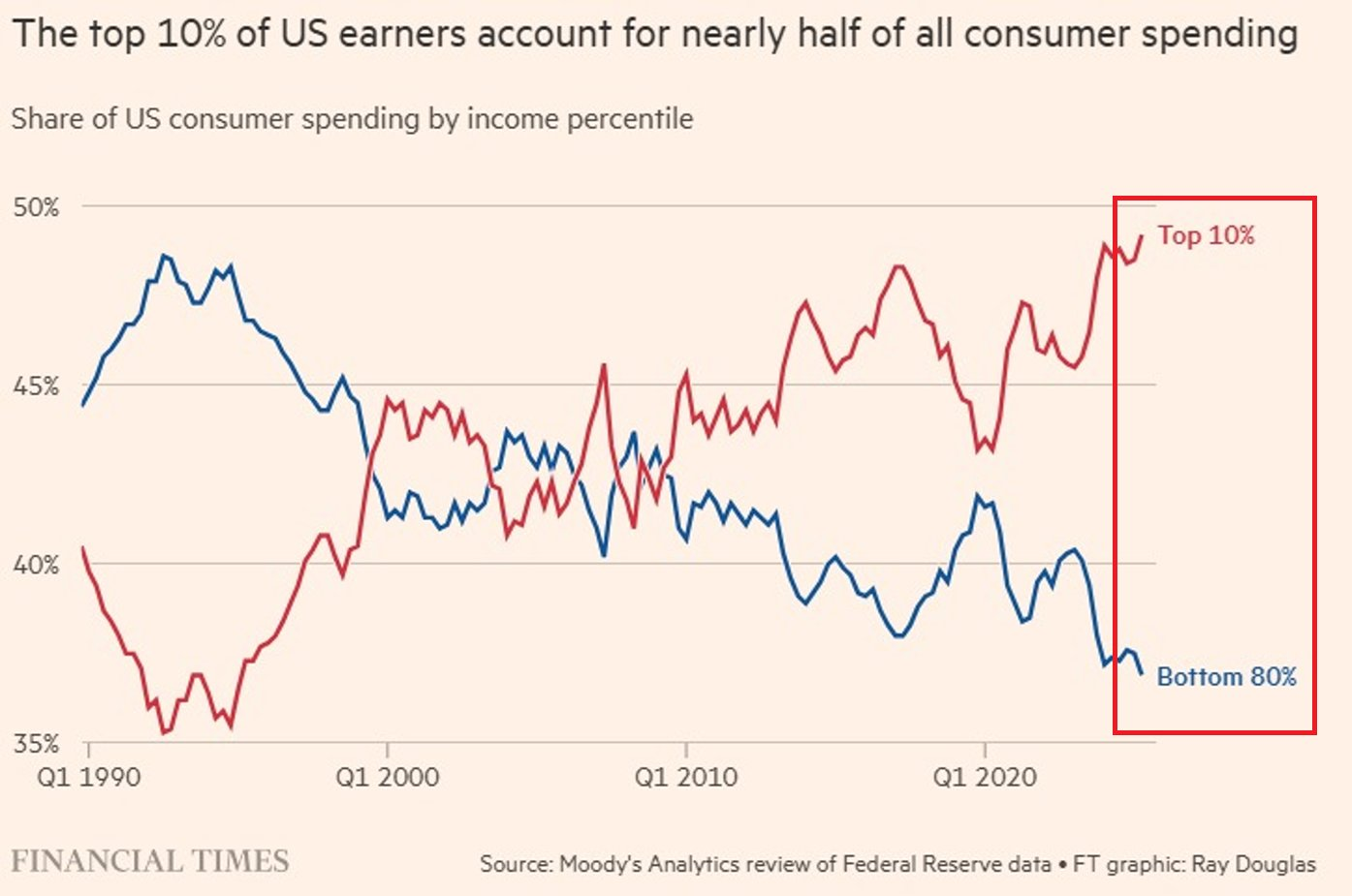

The chart below highlights the widening divide between top earners and the bottom 80%; the top 10% now accounts for 48% of total spending.

Source: FT

This trend looks increasingly bleak.

The economy is also decelerating. Q1 GDP growth was just 1.6%, down from earlier estimates near 3%. Like other official statistics, this figure is likely somewhat revised.

I anticipate the Trump administration might turn to stimulus checks before the year’s end.

A Real Deal

A genuine, enduring agreement with Iran still seems months away, and time isn’t on our side. We urgently need a resolution to reopen the Strait of Hormuz, but Iran’s hold over this key leverage means they won’t relinquish it easily.

The adverse effects on the global economy continue to accumulate.

Both parties behave as if they have ample time, a tactic described by Jim Rickards as “the grandest game of chicken ever played.”

Neither side wants to appear desperate for a deal, though both depend on it. This leaves both trapped in a difficult standoff.

Securing a long-term agreement will demand traditional diplomacy and compromise, but for now, posturing and maximal demands dominate.

Despite upbeat headlines, I remain pessimistic about a durable solution. This crisis could persist throughout the year, causing severe damage to the global economy.

Still, I’m not necessarily bearish on growth stocks right now. The market is in a clear mania phase, and shorting such an environment is risky. When investors crave reasons to drive stocks higher, they will find them. But when this bubble bursts, it will be dramatic.

Hopefully, I’m mistaken, and a lasting deal will come to pass soon.