Missiles and Drones Fly as Iran War Smolders

The fragile ceasefire with Iran appears to be on the verge of collapse.

Yesterday, the U.S. Navy targeted and disabled an unoccupied oil tanker that was en route to Kharg Island after it tried to evade the blockade and disregarded commands to stop.

An aircraft launched a Hellfire missile into the tanker’s engine room, rendering it immobile. CENTCOM shared footage of the event on X:

Source: CENTCOM

AGM-114 Hellfire missile. Source: Military.com

To uphold the blockade’s effectiveness, U.S. forces must neutralize ships attempting to run it—at least some of them.

Targets on Iran’s Qeshm Island near the Strait of Hormuz also came under attack.

Simultaneously, Iran launched assaults on U.S. military installations in Bahrain and Kuwait. CENTCOM states all strikes were unsuccessful or intercepted, but Iranian sources contest this. Satellite imaging of the regions has been tightly controlled, so the complete details remain unclear.

Today, Iran conducted missile and drone strikes on Kuwait’s international airport, causing significant damage to at least one terminal.

Kuwait’s International Airport

Kuwait remains a crucial U.S. ally, hosting major military bases and cooperating on missile defense, and possibly conducting retaliatory operations against Iran, although this remains disputed.

Escalation, or Aggressive Negotiation?

Are these recent developments signaling an outright return to war, or are both sides flexing military muscle to strengthen their negotiating positions?

My view leans toward the latter—a strategic show of force rather than a full resumption of hostilities.

Neither party seems eager for a full-scale conflict given what’s at stake. Iran’s economic survival remains precarious, despite enduring nearly five decades of sanctions and chronic inflation.

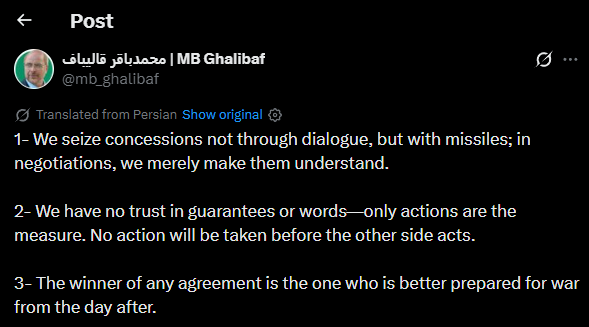

Yet, Iranian chief negotiator M.B. Ghalibaf issued a defiant post on X dated May 29th:

For President Trump, renewed fighting would be unpopular domestically, could destabilize markets, and might harm GOP midterm prospects. While he appears committed to diplomacy, he maintains firm red lines.

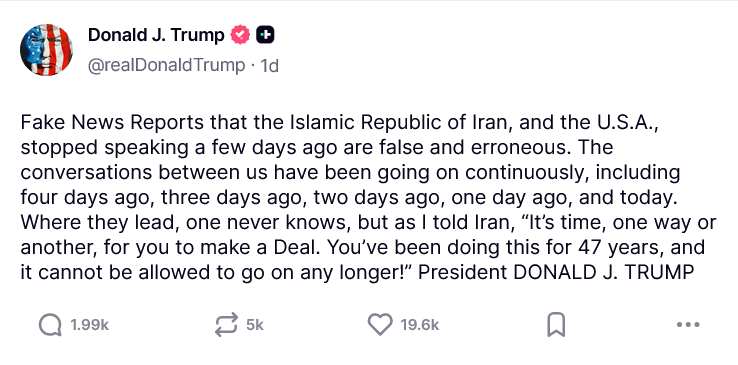

Here is the President’s latest statement on the Iran crisis from Truth Social:

Although both sides seem intent on reaching an agreement, neither appears willing to concede. Therefore, a full resumption of hostilities remains a possibility.

The most probable outcome is eventually reaching a deal, but it may take many months given the current dynamics.

Economic Fallout Approaches

Diesel prices in California have surged to $7.28 per gallon, while in Texas, they stand at $4.81.

This gap significantly impacts truck drivers, farmers, and other diesel consumers.

While California’s higher taxes partly explain its prices, deeper issues contribute to the situation.

Environmental regulations in California drove most oil refiners out decades ago, and the state resists building new pipelines. Consequently, California depends heavily on importing oil from Asian refineries, which source crude mainly from the Persian Gulf.

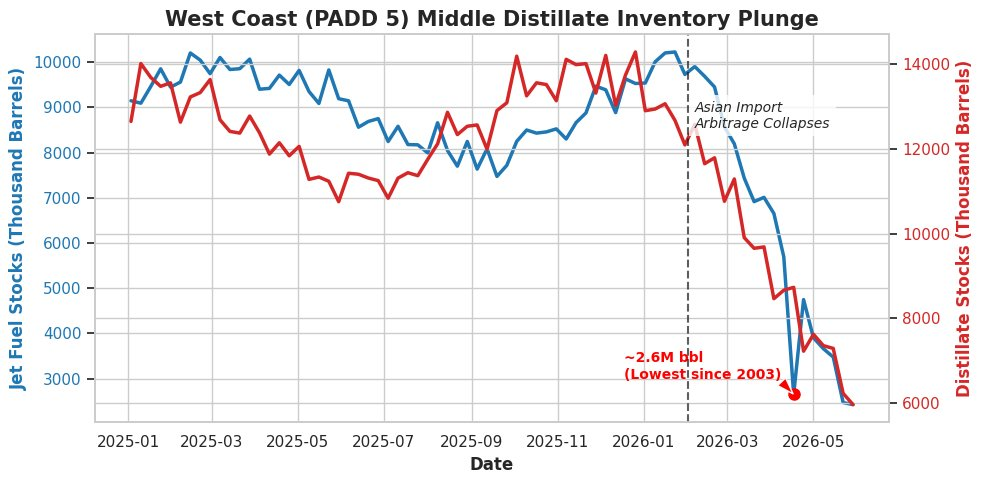

The West Coast—California in particular—is rapidly depleting supplies of jet fuel and other distillates, largely diesel:

California is increasingly relying on fuel imports from the Gulf of Mexico, which involves lengthy shipping routes through the Panama Canal, limiting tanker size.

This explains why the U.S. is only mostly self-sufficient in petroleum. Fuel exports are at an all-time high, but inventories are being drawn down as producers prioritize the highest international bidders.

Rickards’ Take

In a recent briefing to subscribers, Jim Rickards delivered a stark evaluation of the Iran crisis.

The peace talks are a farce.

At best, we have a fragile ceasefire. But the U.S. keeps bombing Iranian bases and Iran keeps firing drones and laying mines, so it’s a thin reed to lean on.

Trump’s only paths at this point are surrender, stalemate and escalation. Surrender won’t happen because the political damage to Trump and the loss of face are too much for Trump to bear. The Iranians won’t agree to anything that makes Trump look good. Why should they? They’re winning the war. Stalemate, in the form of a ceasefire, may continue, but that won’t reopen the Strait.

Escalation could happen, but it won’t achieve any of Trump’s goals, including handing over Iran’s highly enriched uranium or achieving regime change. Escalation might give Trump a short-term political boost among the war hawks. But it would be Trump’s Vietnam and would ruin his legacy. Most importantly, escalation won’t reopen the Strait.

The bottom line for investors and consumers is that the Strait will remain closed indefinitely, with all that implies for global supply chains and inflation. Markets are not priced for this. They are priced for a quick end to the war and the reopening of the Strait.

When reality sinks in, be prepared for major declines in stock prices, higher interest rates and an economic recession — or worse.

Jim’s direct approach is rarely sugarcoated. His predictions on this conflict have so far proven the most accurate, and I share his concerns.

The stock market is currently valuing a near-term reopening of the Strait of Hormuz, which appears highly unlikely.

Last week, optimism around a deal pushed WTI crude prices down to $87 a barrel. Now, as the situation hardens, prices have jumped to $96.

If the Strait remains closed, oil could hit $150 per barrel by summer’s end. Renewed fighting and damage to key infrastructure, like Saudi pipelines that currently circumvent the conflict zones, could push prices even higher.

Regions such as California face severe challenges very soon. Diesel prices have already surpassed $7 per gallon and are likely to climb further. In contrast, states like Texas with oil fracking may avoid shortages but will still feel the impact of rising costs.

The global economy is poised for a significant inflation surge, as soaring oil prices typically drive up the cost of nearly all goods.

My portfolio still includes oil stocks and precious metals. While I am somewhat cautious about miners in the short term—given the possibility of an oil price spike—the sector remains undervalued and discounted since the conflict began. For now, I’m holding steady.

We will keep monitoring and adjusting our strategies to weather the upcoming turbulence.