Ozempic is Killing Food Stocks

Friday’s trading session was rough.

Almost every stock declined, leaving the market awash in red.

However, on my watchlist, there was a small patch of green—a tiny spark of hope amidst the downturn.

That was Campbell’s (CPB). Yes, the well-known soup, food, and snacks company.

For several weeks, I’ve been analyzing consumer staples stocks that have been hammered, including Campbell’s.

Last week, I conducted thorough research on both General Mills (GIS) and Campbell’s, ultimately finding Campbell’s more appealing.

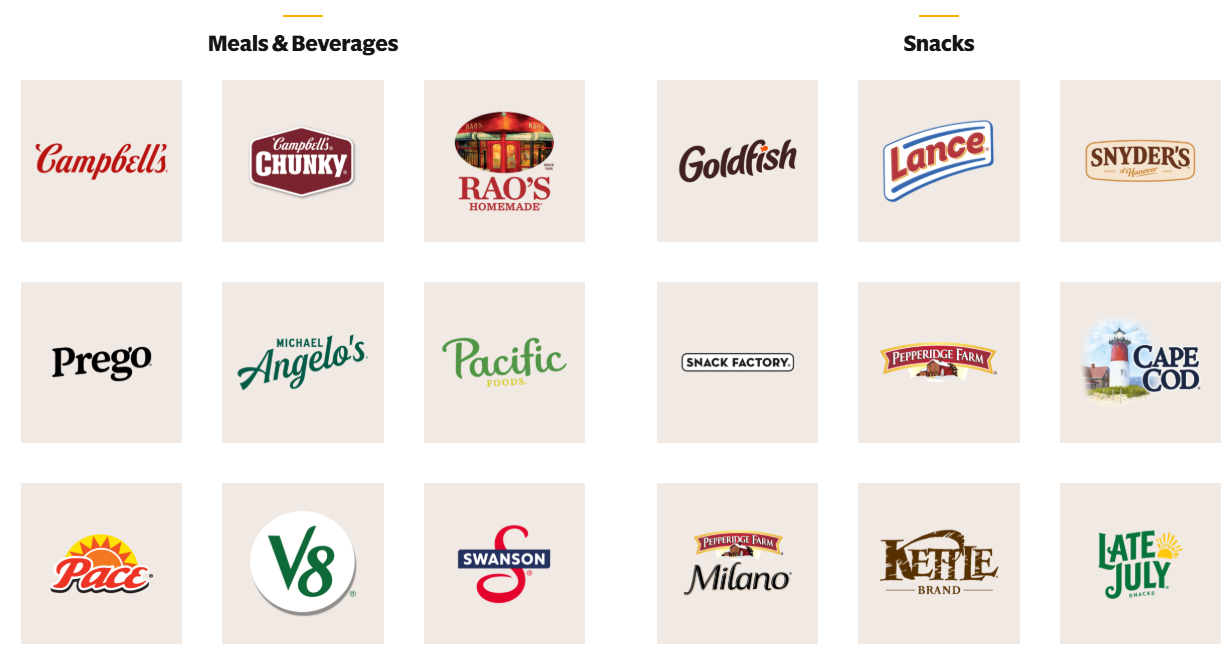

Campbell’s owns a collection of beloved food brands:

Today, let’s explore why Campbell’s presents an intriguing investment opportunity right now.

Real Value, or Value Trap?

At first glance, Campbell’s looks extremely undervalued. It trades near 9 times projected earnings for next year, and offers an attractive 7.2% dividend yield.

The price-to-sales ratio for CPB is just 0.65x, which is remarkably low.

However, recent earnings show a 4% decline in revenue compared to last year, and the company carries a heavy debt load of $6.9 billion.

Despite still generating profit, sales have decelerated, causing investors to shun the stock. Over the last year, shares have dropped 37%, and over five years, 56%.

A major challenge facing companies like Campbell’s is the growing popularity of GLP-1 medications such as Ozempic and Wegovy.

The Ozempic (GLP-1) Threat

This new category of GLP-1 drugs is transforming treatment for diabetes and obesity.

Currently, about 12% of Americans are prescribed one of these medications—a rapid rate of adoption.

While beneficial for many, this shift has significantly harmed U.S. food manufacturers, as overall food consumption and snacking have declined.

This represents one of the most unusual negative forces I’ve observed impacting an entire sector. It’s akin to a tidal wave sweeping through the restaurant and food industries. Whether this effect endures remains uncertain.

For the moment, firms like Campbell’s and General Mills have taken substantial hits.

Private Labels = Trouble

Another considerable challenge for Campbell’s is the surge in “private label” products. Grocery chains now frequently offer their own competitive brands.

Costco’s Kirkland line, in particular, has proven difficult to rival. They identify successful products within Costco and quickly roll out alternatives.

When private labels achieve quality close to that of established brands, it becomes tough for national names like Campbell’s to maintain their footing.

This competition, combined with the rise of GLP-1 drugs, creates a challenging landscape for traditional consumer staples companies.

The Turnaround Plan

Campbell’s is working on a turnaround strategy, which heavily relies on a 2023 acquisition of Sovos Brands, the parent company of the popular Italian brand Rao’s.

Source: The Campbell’s Company

The company paid $2.7 billion for Sovos Brands, a price the market apparently deemed excessive, which has weighed on CPB’s stock price.

Since the acquisition, Campbell’s shares have fallen nearly 50%.

Nonetheless, Rao’s now serves as the chief growth engine for Campbell’s. Their flagship pasta sauce commands a premium price around $8 per jar and enjoys a devoted fan base. Additionally, they have broadened the brand into frozen foods, pasta, pizza, soups, and beyond.

Rao’s strong branding is the main factor attracting me to Campbell’s. While Pepperidge Farm and Goldfish remain assets, these traditional lines are merely fighting to keep market share in today’s environment. Rao’s, however, still has considerable upside.

Elsewhere, Campbell’s is adjusting to evolving consumer preferences. For example, within chips and other snacks, they are shifting away from soybean and cottonseed oils, opting instead for healthier alternatives like avocado oil. Public opinion has turned against “seed oils,” particularly soybean and canola types. Previously marketed as “heart healthy” and widely used in products such as margarine, snacks, and meals, recent research suggests these inexpensive oils function more like industrial-grade lubricants.

Is CPB a Buy?

I have yet to decide if I’ll purchase Campbell’s stock. However, witnessing its decline while the overall market surges stirs my contrarian perspective.

A 7% dividend yield certainly grabs my attention. This payout appears secure in the short term, though it might be reduced if the turnaround strategy falters.

Campbell’s could be a resilient pick during a broad market downturn. It’s already deeply undervalued, pays a solid dividend, and its products tend to perform relatively well in recessions.

Still, genuine risks remain:

- GLP-1 drugs such as Ozempic

- Private label competitors like Costco’s Kirkland

- Changing consumer preferences

The stock might decline further. We’ll continue monitoring it and notify you if promising entry points emerge.