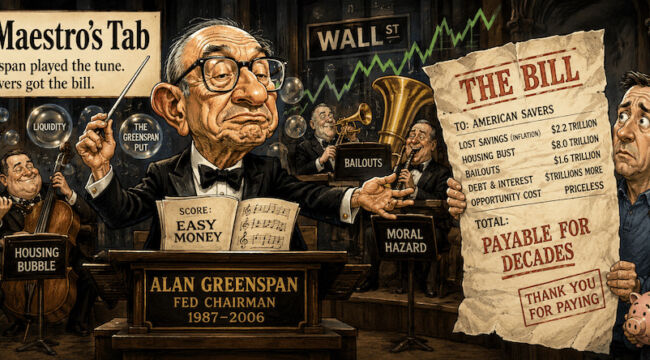

The Maestro’s Tab

Alan Greenspan has passed away.

He was 100 years old and died Monday morning from Parkinson’s disease at home, with his wife, Andrea Mitchell, by his side.

Learning of his death filled me with deep sorrow. Not because his life was cut short—he had clearly lived a long life.

But because he was a man who hovered near true greatness and might have reached it… if only he had followed his better instincts.

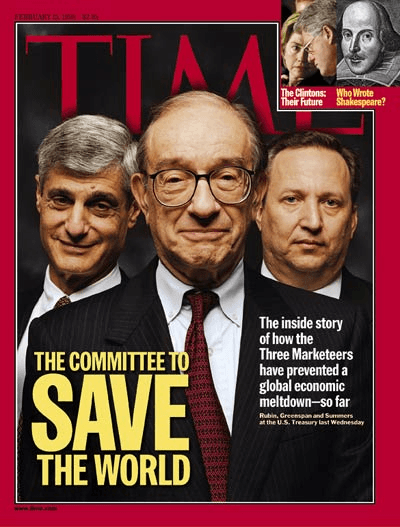

I also reflected on the innocence of my early years in banking when I genuinely admired him. It’s like Zero Hedge enjoys tormenting me, A Clockwork Orange-style, each time it resurfaces this Time magazine cover:

Credit: Time magazine and Michael O’Neill

I don’t regret ever subscribing to Time. Instead, I’m embarrassed I nearly framed this cover.

Predictably, the accolades came flooding in: “A giant.” “A maestro.” “The greatest central banker of the modern era.”

Without question, Greenspan was brilliant.

But ultimately, he was also the man who handed the Federal Reserve a loaded weapon aimed squarely at savers.

The bill racked up during his tenure is still being settled—and will continue for decades. Those paying the price are not those who reaped the rewards.

The Maestro Rises

Greenspan assumed the Fed Chairmanship in August 1987. Two months later came Black Monday, when the Dow plummeted 22% in a single day. Greenspan’s quick and decisive promise of liquidity calmed the markets. A legend was born.

Except for the 1991 Recession, the 1990s were a period of robust growth. Unemployment fell below 4%. Remarkably, the government reported surpluses during the final four years of the Clinton administration. The stock market repeatedly reached record highs. Bob Woodward dubbed him “The Maestro.” Congress revered him as an oracle. Senators, clueless about balance sheets, drank in his Fedspeak as if it were scripture.

I clearly recall former US Senator Phil Gramm humiliating himself by hailing Greenspan as “the greatest central banker in the history of the world” during the Senate confirmation vote for Greenspan’s fourth term. The Maestro listened silently, visibly mortified by the extravagant praise.

Greenspan himself referred to his communication style as “syntax destruction.” He once said to Congress: “I know you think you understand what you thought I said, but I’m not sure you realize that what you heard is not what I meant.”

The media lapped it up. Wall Street adored it. He became untouchable.

The Greenspan Put

However, beneath the surface, decay was taking hold.

Whenever markets faltered, Greenspan cut interest rates. At every sign of trouble—whether the 1994 Bond Debacle, Russia’s 1998 default, the Long-Term Capital Management bailout, or the Y2K scare—the Fed responded with easy money.

Markets quickly learned the lesson: bet big, and if things go wrong, the Fed will rescue you.

Traders termed this the “Greenspan Put”—an unspoken guarantee that losses would be capped, but profits had no limits. This encouraged reckless risk-taking under the Fed’s protection.

Of course, this undermines how free markets should function. Naturally, bad decisions face consequences, discouraging further missteps. Removing those consequences ensures more poor decisions.

Ludwig von Mises dedicated his career to explaining this malinvestment problem. Murray Rothbard elaborated extensively. Sadly, neither influenced Washington policymakers. The tragedy lies in the fact that Greenspan once studied their work. In the 1950s and 60s, he was a follower of Ayn Rand.

During a lecture for Rand’s followers, Greenspan described creating the Federal Reserve as “one of the historic disasters in American history.”

Amen, Alan. Amen.

The then-Randroid understood the gold standard as a critical limit on government’s ability to fuel booms and busts by printing money.

Then power found him, and his understanding shifted.

The Dotcom Bubble

By the late 1990s, the Fed’s cheap money had inflated the biggest speculative bubble in US history to that point. Internet startups lacking revenue, profits, or viable business models raised hundreds of millions.

CNBC became essential viewing during the dotcom craze. People who had never followed markets tuned in. Many middle-class investors painfully discovered the Nasdaq wasn’t a high-yield savings account.

Names like Pets.com, Webvan, and Kozmo.com now sound almost comical. But that was cold comfort to those who lost their life savings.

$5 trillion in market value vanished between 2000 and 2002.

Following the crash, Greenspan’s Fed cut rates to 1% and kept them there.

This foundation set the stage for the crises to come.

The Housing Bubble

With interest rates at 1%, money sought new outlets. Housing became the destination. Mortgage lenders approved loans for almost anyone. “No Income, No Job, or Assets? No problem, NINJA loans are here.” Incentives encouraged reckless lending.

Why the lax oversight? Wall Street bundled these loans and sold them as AAA-rated securities to naïve foreign banks and sovereign wealth funds. If Ivy League grade inflation shocks you, wait till you see what rating agencies handed out during 2005-2008. This is how a US crisis rippled worldwide.

Greenspan dismissed worries about a national housing bubble, conceding only that local markets might be overvalued.

He underestimated by $8 trillion—that’s the household wealth lost in the 2008 crash.

“Those of us who have looked to the self-interest of lending institutions to protect shareholders’ equity, myself especially, are in a state of shocked disbelief,” he told Congress in October 2008. (Editor’s note: Remember this remark.)

The Maestro eventually grasped that free markets require free pricing. Fixing money’s cost below its market value fabricates false prosperity—until reality intervenes.

He admitted that he had been right about 70% of the time.

The 30% left proved nearly catastrophic.

His Legacy

The tributes have been generous, as they typically are.

Paradigm Press’ Enrique Abeyta commented on our app’s Daily Feed:

While there are many critics of the Fed, my view is that they should ultimately be judged on the results. Those results are economic stability, growth, and high employment. Objectively, based on those measures, the US economy has absolutely CRUSHED it in the last 50 years. Far outpacing every other developed economy in the world by a huge amount. RIP Alan Greenspan – you did your job!

Greg Ip shared a heartfelt piece in The Wall Street Journal reflecting on Greenspan and his time covering the Fed.

However, the Journal’s editorial board released an article titled “The Myth of Alan Greenspan,” which surprised me. They criticized his 2008 comment (above) about self-interest.

That comment, which received enormous publicity, let the political class off the hook and fed the belief that the panic was a crisis of capitalism that needed more regulation. Greenspan never admitted the failure of monetary policy or of the regulators at the time who had allowed Citigroup and other banks to create the off-balance-sheet vehicles that failed.

Libertarian historian and writer Tom Woods echoed this viewpoint:

Because of Greenspan’s earlier association with Ayn Rand, and because the general public knows so little about the Fed, when the 2008 crash occurred, people generally went along with blaming “capitalism” — even though the Federal Reserve is a non-market institution created by act of Congress and enjoying a government-granted monopoly, and even though Greenspan’s manipulations overrode what the market was trying to say.

Greenspan’s legacy is 2008, and the undeserved reputational damage that the market economy suffered as a result.

In light of this, it’s no surprise that Mamdani is now Mayor of New York City and successfully swept the recent elections.

@Handre explained:

In 1966, a younger Greenspan wrote an essay called “Gold and Economic Freedom.” He laid out the case with precision. The gold standard protected savers from confiscation by inflation. Welfare statists hated gold because it stood in the way of their deficits. He wrote that the abandonment of gold made deficit spending a “scheme for the hidden confiscation of wealth.” He was right. He knew it. Then he took the job running the printing press.

Finally, Bill Bonner wrote here in the Daily Reckoning:

Rand was in raptures when her smooth disciple was summoned to Washington. Now, she crowed, she had ‘her man’ at the Fed.

She did not have him long. Principles are cheap furniture for a struggling philosopher or a journeyman saxophonist; he may keep them about the parlor all his life and dust them fondly. But the Chairmanship of the Federal Reserve calls for principles of another make. Volcker had wrestled the inflationary beast to the floor, now the politicians could spend and borrow more freely. But they needed THEIR man at the Fed.

There lay Greenspan’s true historic office. The famous “Greenspan put” was nothing grander than this: he stood ready to catch every gambler who flung himself off the ledge — and so, he presided over the largest carnival of phony prosperity the world has ever staged.

Greenspan set the standard for every Fed Chair who followed. He ingrained the belief that the Fed should manage business cycles through rate adjustments. He molded investors to view the Fed as a safety net rather than a brake. He transformed the central bank from a last-resort lender into a permanent enabler of risky behavior.

Ben Bernanke followed this blueprint after 2008, pushing rates to zero and maintaining them for years. Janet Yellen kept rates low, and Jerome Powell reduced them again during COVID.

It’s no surprise hedge fund managers mourn Greenspan’s passing. But at least they have Warsh now… right?

The Patience Tax discussed in the Rude Awakening—the penalty on savers, the reward for borrowers, the destruction of returns that once made caution sensible—bears Greenspan’s mark. So do the False Boom and the Ratchet.

While he did not invent central banking or fiat currency, Greenspan made both appear benign, even advantageous, for long enough to suppress serious challenges.

A Complicated Man

Alan Greenspan was no villain, and certainly not foolish. By most accounts, he was genuinely kind, a devoted enthusiast of classical music and economic data, a hard worker who pondered complex issues deeply.

In his early years, he saw things clearly. As @Handre noted above, his 1966 essay, “Gold and Economic Freedom,” stands as one of the clearest defenses of the gold standard ever penned. He argued central banking was a tool for transferring wealth from producers to politically favored groups. He grasped the Cantillon Effect.

But when power entered the scene, clarity shifted.

Unfortunately, this is typical. Serving under a small circle of powerful figures, your incentives align more with their desires than with truth. Greenspan served four presidents, retaining his position by pleasing them. Pleasing them meant cheap money when times grew tough.

Wrap Up

Alan Greenspan reached 100 years of age. He lived long enough to witness every bubble he helped inflate collapse. He watched the Fed he once led morph into an institution that would have disgusted the idealistic young man who had written against it.

History will remember him as a maestro. That label isn’t entirely fitting.

He was a man with exceptional talents who applied them to uphold a system he once recognized as flawed. The harmony he created was beautiful enough that many failed to see the edifice crumbling around them.

You saw it. That’s why you’re still here.

The tab remains open. It will be for some time to come.

Rest in peace, Mr. Greenspan. We are still cleaning up.