The Elon Premium is Real

The upcoming SpaceX IPO is destined to be insane.

Think of it as an investor’s Superbowl, but taken to an entirely new level. Even bigger.

The anticipated valuation (market cap) for SpaceX at IPO is approximately $1.75 trillion.

I recall when Facebook debuted publicly with a market cap of $104 billion and thought that was staggering. SpaceX will be nearly 17 times larger.

Today, let’s break down the numbers behind SpaceX and assess whether this stock is worth buying.

A Hefty Price

At $1.75 trillion, the figure is so massive it’s difficult to truly comprehend.

To grasp this magnitude, here’s a quick analogy: one million seconds equals 11.5 days, one billion seconds spans 31.7 years, and one trillion seconds stretches out over 31,688 years.

No IPO of this scale has ever occurred before. Nothing else is remotely comparable.

So, what exactly are investors acquiring at this price?

In 2024, SpaceX earned a profit of $791 million. The following year, 2025, it incurred a loss of $4.94 billion. In just the first quarter of 2026, it lost an additional $4.28 billion.

SpaceX’s core space launch operations and Starlink have proven lucrative. So what changed? The company expanded by merging with X (formerly Twitter) and xAI, Elon’s social media and artificial intelligence ventures.

As widely known, AI is an expensive sector. GPUs and data infrastructure require huge investments, and Elon’s firm has swiftly developed some of the largest AI computing clusters globally.

The Colossus data centers house roughly 230,000 top-tier Nvidia GPUs—the best AI hardware available on Earth—at a scale unmatched by nearly anyone else.

Soon, xAI will start turning this computing power into significant revenue. A new agreement with Anthropic, creators of the popular Claude AI models, is expected to generate about $1.25 billion monthly.

This alone should bring them close to breaking even. Plus, there’s a strong possibility that Elon’s proprietary AI model, Grok, will eventually rival ChatGPT and Claude in sophistication.

Nonetheless, AI remains fiercely competitive. Surprisingly, SpaceX is largely an AI enterprise.

Of course, the space launch segment remains robust, and the Starlink satellite network continues to grow at 100% annually. In 2025, Starlink generated $11.6 billion in sales. That’s undeniably a promising business.

Yet the major risk—as well as opportunity—in this stock is tied to the AI side. Massive investments are being funneled into data centers and the development of Grok, their in-house AI platform.

The Elon Premium

Elon Musk is arguably America’s most remarkable entrepreneur of this century. PayPal, Tesla, SpaceX, the Boring Company—an impressive legacy.

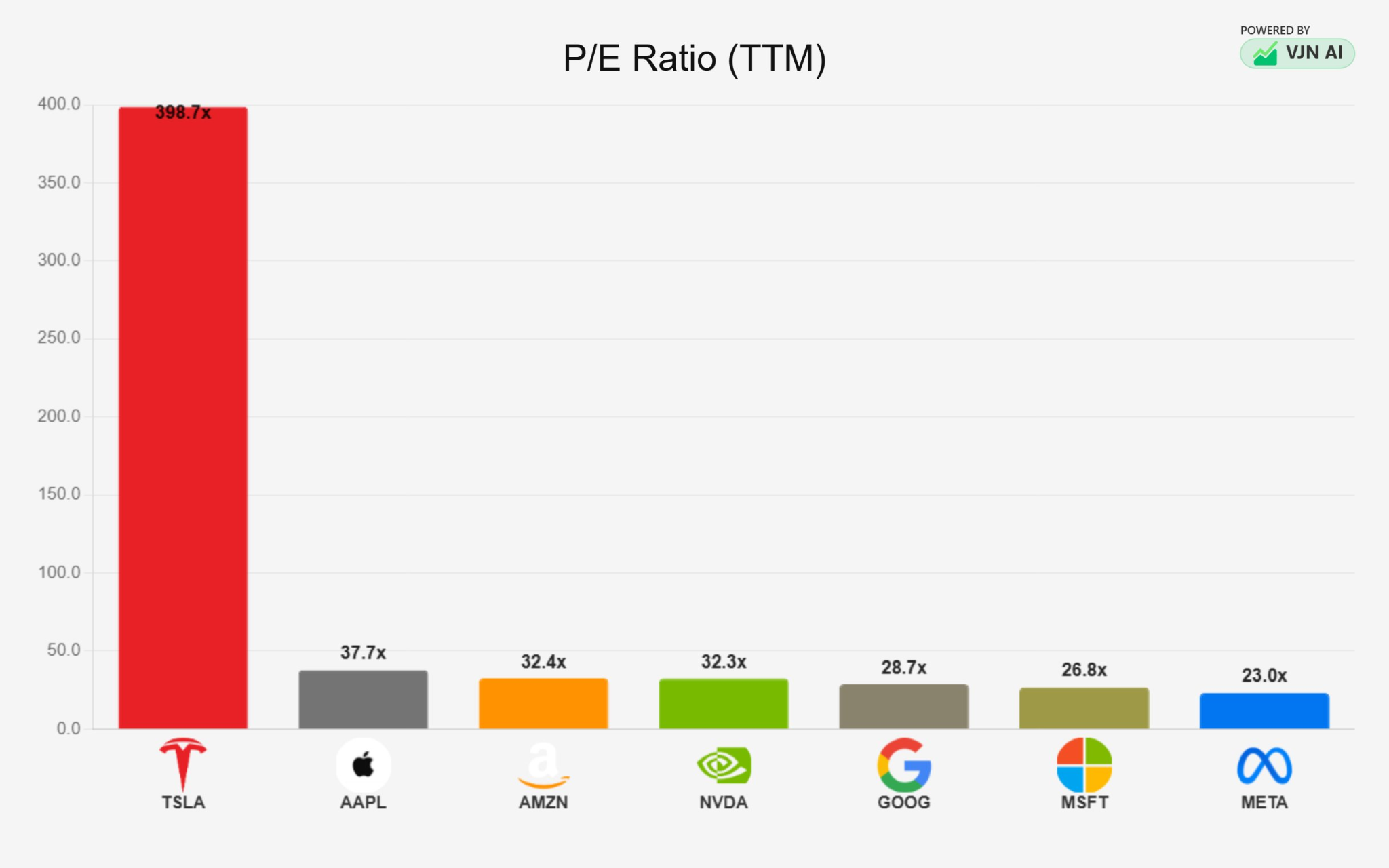

Tesla has created thousands of millionaires, and its shares are far from cheap. The chart below illustrates the price-to-earnings ratios of the “Magnificent 7” tech giants, highlighting how Tesla remains pricier than the rest.

Tesla has been labeled overvalued by many for years, yet it consistently retains a premium valuation. Elon’s dedicated followers believe he will dominate in autonomous vehicles and humanoid robotics, both enormously lucrative markets. This is what constitutes the Elon premium.

It’s entirely plausible that SpaceX will launch at a high valuation and maintain—or even increase—that level over time.

Personally, I’m holding off on purchasing at the IPO. The price feels too steep for me. Given the 2025 revenue estimate of $18.7 billion, the stock would debut at an expensive 94 times sales. That’s… generous to say the least.

That said, I had chances to invest in SpaceX privately when its value hovered around $100 billion but never acted. It always felt overpriced. Clearly, that was an error.

The fundamental space launch business is exceptional. Starlink is remarkable. And AI holds enormous promise.

If Grok achieves competitiveness with ChatGPT and Claude—currently the top two AI models—it could well justify this valuation. OpenAI and Anthropic, the companies behind those models, are each valued near $900 billion without aerospace ventures included.

The Elon premium undeniably exists and might support this immense valuation. However, I worry about the potential impact of a market downturn. Even Elon’s massive fan base may not sustain such lofty prices in a crash.

For now, SpaceX remains too pricey for me, so I’ll stay on the sidelines. Next week will tell if that’s a wise decision or not.