The dispute between member states and the EC risks tearing the entire union apart.

The EU, deeply entrenched in its warlike stance, has at last greenlit the €90 billion loan to Ukraine after Hungary lifted its veto, ending a deadlock that had persisted for five months since at least December 2025. A key insight is that this conflict is essentially driven by the City of London. Although the €90 billion figure is notably lower than the earlier controversial €140 billion proposal—which had sparked outrage when the European Commission threatened to compel member approval—the financial support still amounts to throwing good money after bad. Sooner or later, reality will impose itself.

EU officials have also confirmed the formal adoption of the bloc’s 20th sanctions package on Russia, resolving a standoff that had delayed the measure for several days. The deadlock ended following the resumption of oil shipments via the Druzhba pipeline, which had been disrupted after Ukrainian President Zelensky shut it down in January as leverage to pressure Hungary and Slovakia into approving the loan. This pipeline, running through Ukraine, is critical for landlocked Hungary and Slovakia—both of which withheld sanctions approval while oil flow was halted. Zelensky announced on Tuesday that deliveries would recommence, with Budapest and Bratislava officials confirming oil was moving again by Wednesday.

With the oil supply issue settled, the Cyprus EU Presidency finalized the sanctions via written procedure, confirming completion by Thursday afternoon. It is worth recalling that the push for mutualized debt obligations began back in 2025, presenting a “plan A” and a “plan B”. Merz and von der Leyen failed to execute “plan A”, which involved seizing frozen Russian assets held by Euroclear in Belgium. “Plan B” involved issuing bonds backed collectively by EU member states; this was ultimately adopted, albeit with the reduced €90 billion amount. Currently, talk centers on covering Ukraine’s debt payments through interest accrued on Russia’s frozen funds if Ukraine defaults.

Despite pro-Kyiv mainstream EU media celebrating the €90 billion “loan”, it reveals notable shortcomings of the EU Commission. This amount falls far short of covering Ukraine’s war expenses and basic budgetary requirements through 2027, even compared to earlier estimates from December when the smaller sum was agreed. Moreover, with the recent U.S. conflict against Iran pushing energy prices up, Ukraine’s previous budget projections are now outdated and insufficient.

Additionally, news reports indicate Russia plans to halt Kazakh oil shipments passing through the northern Druzhba pipeline to Germany, which is expected to increase inflationary pressures there.

From Ukraine’s logistical standpoint, this poses challenges in ferrying troops to reinforce front lines engaged in intense combat, along with the movement of equipment across their contact zones. Civilian transit also depends on these routes, highlighting how a separate conflict involving Iran escalates the costs and complications of the Ukraine war. Nonetheless, the EU will lend these funds to Ukraine, despite widespread understanding that repayment is unlikely, effectively making it a disguised gift burdening the 24 member states who foolishly or under pressure consented.

As detailed in Destroying Europe in order to save it: Extortion, theft, and the EU’s two disastrous choices, this complex maneuver toward plan B (now manifested as the €90 billion “gift”) threatens to convert the EU into a de facto single super-state governed centrally, abandoning its origins as a treaty-based economic union of independent member states. The resistance from Slovakia and Hungary led von der Leyen to again threaten to remove member states’ veto privileges in decision-making. The most commonly proposed solution is QMV – Qualified Majority Voting, which under a liberal reading of existing treaties could override unanimity rules in areas prone to vetoes like foreign policy and taxation.

However, implementing such a shift would provoke widespread political backlash throughout the EU, emboldening Eurosceptic movements and potentially causing government collapses in various countries. This could trigger referenda reconsidering the EU’s very foundation. When Brussels touts a €90 billion aid package to Ukraine over two years, it hardly appears as if it is firmly in control. The financial logic behind Plan B depended on strong EU unity to guarantee mutualized debt issuance.

The €90 billion arrangement introduces a subtle yet crucial uncertainty that under usual circumstances would concern investors. According to the December terms, Hungary, Slovakia, and Czechia are exempt from direct liability, but the bonds are still issued under the EU umbrella and investors naturally assume a collective guarantee. If the bonds falter or default risk rises, pressure will fall on the EU and its more financially stable members to bridge any gap, establishing an implicit liability that spares no one, including the City of London’s key financial institutions backing the deal.

The City of London’s War

Are these the same interests behind Boris Johnson’s urging Zelensky to reject the Turkish-brokered ceasefire deal that could have ended the conflict early on? London’s major financial players such as HSBC, Goldman Sachs International, J.P. Morgan, and Barclays appear to be the key architects. Historically, they hold the greatest stake in underwriting and purchasing these bonds, distributing the remainder through their Primary Dealer Network. This reveals the deep ties between Western finance capitalism and support for the Kiev regime. The arrangement ensures that the EU follows a script directed not by its member nations but by the City of London. These financiers have been sponsoring this war from the start and are locked into perpetuating their scheme, driven by the sunk-cost fallacy.

From inception, the €90 billion scheme resembled more a financial operation than a genuine policy move. The European Commission issues the bonds, but it is the underwriters—primarily London-based banks—who control pricing and distribution. Their goal is to profit from heavy sovereign-style debt sales, influence EU policy concerning Russia and Ukraine, and sustain a bellicose environment that keeps demand high. They refuse a real negotiation to end the conflict, contradicting the historical maxim that “the victors determine the conditions of peace”—Russia, in this scenario. Once it becomes undeniable that much of the former Ukraine will not return to Kiev’s control, the EU’s Ukraine-war bubble will burst.

Source: https://ec.europa.eu/commission/presscorner/api/files/document/print/en/ip_25_2735/IP_25_2735_EN.pdf?

With major London-based banks—HSBC, Goldman Sachs International, J.P. Morgan, and Barclays—serving as joint lead managers on EU syndicated bonds tied to the unprecedented NextGenerationEU fund (which also backs war efforts in Ukraine), the €90 billion initiative follows this precedent. These financial institutions have strong incentives to prolong the conflict between Ukraine and Russia, as the ongoing crisis guarantees continued demand for bonds, derivatives, and consulting. Yet it runs deeper: the EU’s political bodies act mostly as facilitators, legitimizing the operation while City of London financiers reap profits and destabilize European markets. This scheme is both a geopolitical gambit and an act of malice by the UK against EU member states and their populations, ironically carried out with the apparent cooperation of the EU Commission and the broader “Eureaucracy.”

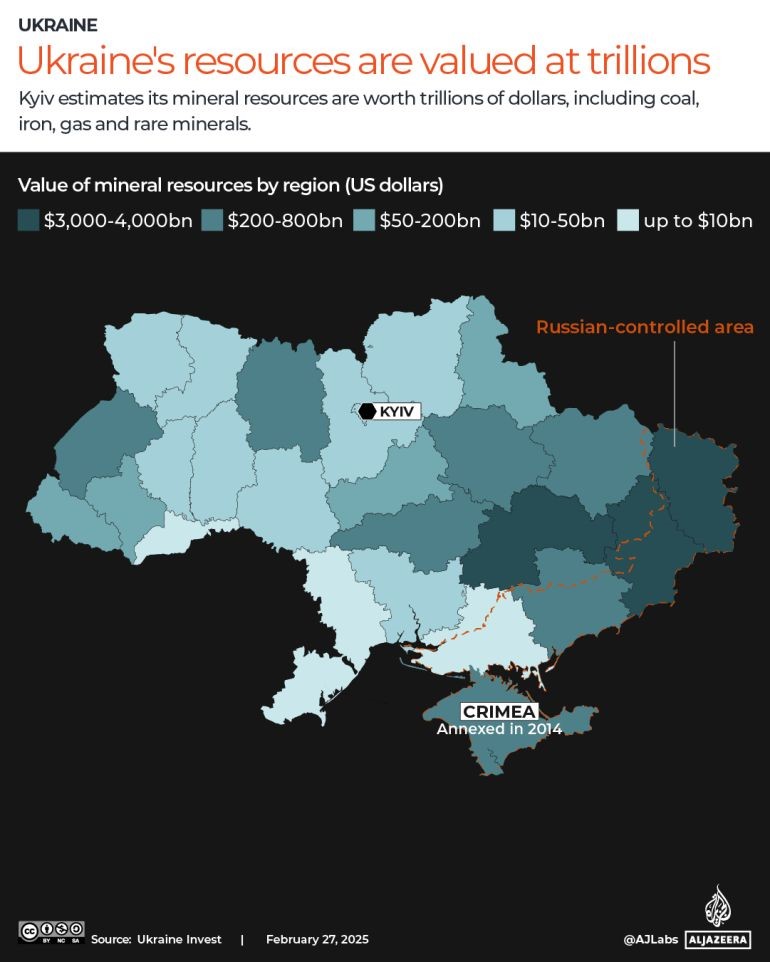

What we are witnessing is a calculated maneuver: the EU must appear united, Ukraine must seem financially supported, and the City of London ensures the war and debt machinery operates without interruption. Meanwhile, this strategy bets on wearing down the EU in a hopeless confrontation with Russia while holding out for a future U.S. administration—Democrat or neocon Republican—beginning in 2029, when American funding will resume to intensify the push against Russia. The British back this war not only to sell EU bonds but also to exploit Ukraine’s vast industrial, agricultural, and especially mineral wealth. Ukraine’s deposits, estimated between €12 and €22 trillion in minerals, are vital. While the EU needs the resources located in regions already integrated with Russia, it cannot risk a political outcome enabling Moscow to become Europe’s gatekeeper to Ukraine’s assets.

Plan B: Ambition Without Execution

The initial Plan B, formulated after the failure of the frozen Russian assets seizure, aimed ambitiously to issue fully mutualized EU debt, making all member states jointly responsible. However, the EU abandoned this model in favor of a setup allowing dissenting states to opt out of direct obligations.

Brussels now recognizes it cannot force mutualization without risking the EU’s collapse. This is a game the Commission has lost. Future efforts for centralized EU debt issuance will be haunted by this setback, and every opposing member state understands the Commission will concede first. Full mutualization could have generated €140–165 billion, but this compromise yields only €90 billion, just about two-thirds of the target. Given soaring energy costs, the €90 billion will cover less and last a shorter time than initially anticipated when the plan was crafted in 2025. Despite Brussels’ triumphant rhetoric, Ukraine remains grossly underfunded—an issue we will now examine.

€90 Billion in the Context of Ukraine’s Budget

The impressive figure of €90 billion obscures the financial reality facing Kiev. Ukraine’s 2025 budget forecasted UAH 3.94 trillion (€77 billion) in expenses against UAH 2.34 trillion (€46 billion) in revenues, resulting in a significant deficit. Early 2026 estimates project spending of 4.8 trillion UAH (€92–94 billion) against revenues of 2.8 trillion UAH (€53–56 billion), creating a shortfall near 18% of GDP.

Spread over two years—the period this bond is intended to cover—the EU contribution represents roughly €45 billion annually, about half of Ukraine’s total financing gap. The remainder must be sourced from the IMF, the U.S., and other international donors. However, there is no guarantee these funds will materialize. The U.S. has clearly signaled reduced involvement, preferring instead to sell limited weapons supplies to Europe—which it can scarcely afford—citing the Iran conflict as a convenient justification for cuts.

Von der Leyen’s Commission heralds this €90 billion deal as a victory, but the reality is the EU did not assert dominance over reluctant member states; instead, it relented to avoid legal and political turmoil. The City of London banks achieved their aim: a massive, lucrative bond issue disguised as wartime aid, perpetuating investments likely lost forever. This sums up the EU: ambition promoted as achievement, compromise disguised as success. While the €90 billion package may seem like a win to those uninformed, the true picture shows the EU relinquishing control to financial interests and external forces, leaving Ukraine underfunded and fully dependent on a fragmented donor base. It is probable that nearly €200 billion will be requested in 2027 as current funds fall short and inflationary pressures mount. The clash between member states and the EC at that juncture may well bring the entire union to collapse.